Breaking: FOMC Minutes lean toward higher-for-longer narrative

The June FOMC Minutes reinforced the Fed’s cautious approach as policymakers unanimously agreed to maintain interest rates unchanged while keeping a close eye on inflation risks.

Although officials agreed that downside risks to the labour market had eased somewhat, they generally continued to view upside risks to inflation as elevated. Several participants warned that persistent price pressures could stem from stronger AI-related investment, higher tariffs or renewed tensions in the Middle East, with staff projections revised to show higher inflation in both 2026 and 2027 than previously expected.

Importantly, a few policymakers judged that another rate hike could eventually become appropriate, although they still supported leaving policy unchanged at the June meeting. Almost all of those participants indicated that additional tightening would likely be warranted should inflation evolve along less favourable paths.

The Minutes also revealed a subtle but meaningful shift in the Committee's communication. Most participants favored removing language that suggested an easing bias and a majority favored shortening the post-meeting statement, arguing that it should instead emphasize the Fed’s commitment to achieving its dual mandate and restoring price stability.

While staff modestly downgraded the GDP outlook relative to April, the discussion suggests policymakers remain considerably more concerned about inflation persistence than slowing growth, reinforcing the view that the bar for rate cuts remains high.

Bottom line

The Minutes delivered a hawkish hold. Policymakers continue to see inflation as the dominant risk, several officials still believe further tightening could become necessary, and the Committee appears keen to distance itself from any perception that rate cuts are imminent. From a market perspective, the release supports the higher-for-longer narrative and should remain supportive of the US Dollar and Treasury yields while weighing on rate-sensitive assets.

Market reaction

The Greenback remains under pressure on Wednesday, pushing the US Dollar Index (DXY) to challenge the 101.00 region. In the meantime, investors continue to assess the FOMC Minutes while closely following developments from the geopolitical landscape.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Japanese Yen.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.09% | -0.30% | 0.26% | -0.20% | -0.05% | -0.43% | -0.00% | |

| EUR | 0.09% | -0.21% | 0.37% | -0.11% | 0.05% | -0.34% | 0.09% | |

| GBP | 0.30% | 0.21% | 0.57% | 0.10% | 0.25% | -0.13% | 0.28% | |

| JPY | -0.26% | -0.37% | -0.57% | -0.47% | -0.30% | -0.70% | -0.28% | |

| CAD | 0.20% | 0.11% | -0.10% | 0.47% | 0.15% | -0.24% | 0.18% | |

| AUD | 0.05% | -0.05% | -0.25% | 0.30% | -0.15% | -0.39% | 0.01% | |

| NZD | 0.43% | 0.34% | 0.13% | 0.70% | 0.24% | 0.39% | 0.41% | |

| CHF | 0.00% | -0.09% | -0.28% | 0.28% | -0.18% | -0.01% | -0.41% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

This section below was published as a preview of the FOMC Minutes of the June 16-17 meeting at 17:15 GMT.

- The FOMC Minutes are expected to show further insight about the first Federal Reserve meeting with Kevin Warsh as chairman.

- The Fed is likely to provide a reduced version of the minutes amid Warsh’s reluctance to provide forward guidance.

- Investors will be attentive to growth and inflation expectations to assess the bank’s policy plans.

The United States (US) Federal Reserve (Fed) will release the Minutes of the June 16-17 Federal Open Market Committee (FOMC) meeting on Wednesday at 18:00 GMT. The Minutes should shed more light on the Fed’s hawkish hold delivered at Kevin Warsh’s first meeting as Fed Chair. Even so, doubts remain about how much the minutes will reveal, given Warsh's refusal to provide forward guidance.

The US central bank left the Fed Funds rate unchanged in the 3.50%-3.75% range, as widely expected, although the statement’s language showed a hawkish tilt that surprised markets and provided some support to the US Dollar (USD).

The committee approved the decision unanimously, putting an end to market speculation about the divergences within the governing council. Beyond that, the statement highlighted resilient activity and above-target inflation, adding to the case for interest rate hikes in the near term.

Kevin Warsh and his unexpected hawkish edge

The Fed met expectations in June and left its benchmark interest rate on hold for the sixth consecutive time, with the new chairman’s hand evident in the reduced monetary policy statement. The main takeaway of June’s meeting, however, was Kevin Warsh’s willingness to remove forward guidance, in clear contrast to his predecessor, Jerome Powell’s style, to allow the central bank further flexibility in setting monetary policy.

Warsh, however, was swift to tackle investors’ concerns about the central bank’s independence, showing an “unambiguous” commitment to deliver price stability, which the market took as a hawkish signal.

The bank’s statement also confirmed Warsh’s plans to implement radical changes in key areas of the central bank, including communication, data sources, and the framework of the central bank's inflation studies, which might also alter the bank’s monetary policy stance in the medium term.

As an immediate consequence of the new house style, the bank is expected to deliver a slimmer, less informative version of the Minutes with no clear hints about the bank’s rate path beyond the economic and inflation outlook.

With this in mind, investors will cautiously analyse the Minutes against the framework of last week’s disappointing Nonfarm Payrolls (NFP) report. June’s Payrolls showed a sharp slowdown in net employment creation, at 57K against expectations of a 110K increase, following three months of strong data, which prompted investors to push back hopes of Fed rate hikes.

Beyond that, concerns about inflation have eased since last month’s meeting. The latest US inflation figures remain well above the 2% target, but the easing tensions in the Middle East have brought Crude Oil prices back to pre-war levels. This is likely to cool price pressures over the coming months, and might grant Warsh with valuable leeway to postpone rate hikes.

When will FOMC Minutes be released and how could they affect the US Dollar?

The FOMC will release the Minutes of the June 16-17 policy meeting at 18:00 GMT on Wednesday.

Investors’ bets on Fed rate hikes have receded from the highs witnessed before last week’s NFP report, but money markets are still pricing at least a 25-basis-point rate hike over the next six months, which keeps the US Dollar buoyed.

The CME Group’s FedWatch tool still shows a 58% chance of a rate hike in September and nearly an 80% chance that the bank will tighten its monetary policy before the year-end. In this context, a clear message from the bank to contain inflationary pressures might reassure Fed tightening bets and provide a fresh boost to the US Dollar.

Downside risks from the US Dollar, in this case, would come from comments that play down the risk of second-round effects on inflation and link current higher prices to the energy shock.

USD moves, in any case, are likely to be limited, as recent developments in the Middle East and last week’s labour figures have altered the scenario, and investors are likely to await further US economic releases to better assess the Fed’s rate hike calendar.

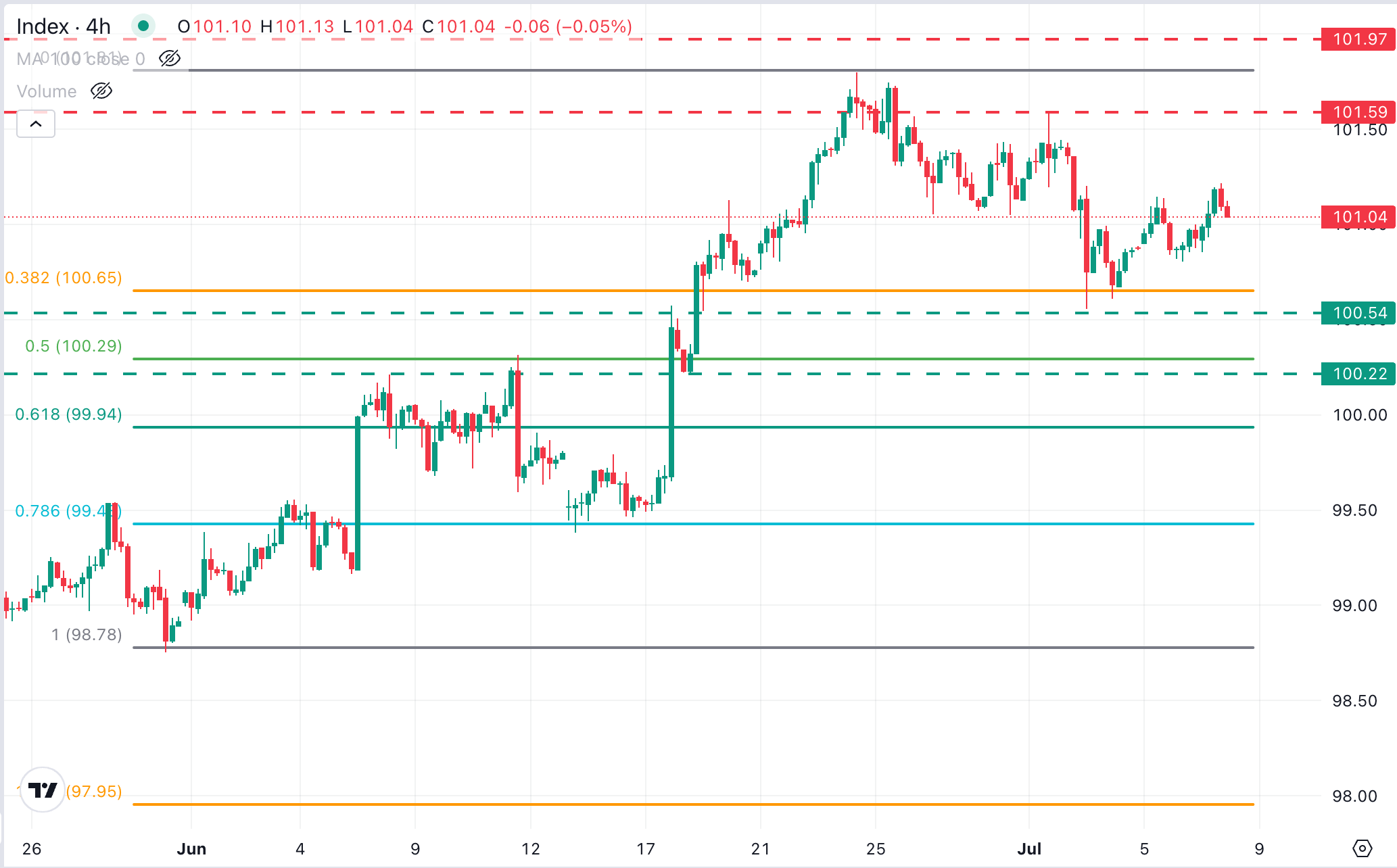

The US Dollar Index (DXY) has been wavering on both sides of the 101.00 level so far this week, trading within a corrective channel from last week’s highs at the 101.80 area. Momentum indicators highlight a mixed bias, with the Relative Strength Index (14) just below 50 and the Moving Average Convergence Divergence (MACD) near zero hinting at a lack of clear bias, although the broader trend remains bullish.

Immediate resistance emerges at the mid-range of the 101.00s, which held bulls in early July, closing their path towards the 2026 peak of 101.80. On the downside, bears would have to breach the area between the 38.2% Fibonacci retracement of June’s rally and the July 2 low, in the 100.50-100-60 area, to confirm a deeper correction, aiming for the June 11 high around 100.30. Further down, the 78.6% Fibonacci retracement meets the June 15 low, just below 99.40.

(The technical analysis of this story was written with the help of an AI tool.)

Interest rates FAQs

Interest rates are charged by financial institutions on loans to borrowers and are paid as interest to savers and depositors. They are influenced by base lending rates, which are set by central banks in response to changes in the economy. Central banks normally have a mandate to ensure price stability, which in most cases means targeting a core inflation rate of around 2%. If inflation falls below target the central bank may cut base lending rates, with a view to stimulating lending and boosting the economy. If inflation rises substantially above 2% it normally results in the central bank raising base lending rates in an attempt to lower inflation.

Higher interest rates generally help strengthen a country’s currency as they make it a more attractive place for global investors to park their money.

Higher interest rates overall weigh on the price of Gold because they increase the opportunity cost of holding Gold instead of investing in an interest-bearing asset or placing cash in the bank. If interest rates are high that usually pushes up the price of the US Dollar (USD), and since Gold is priced in Dollars, this has the effect of lowering the price of Gold.

The Fed funds rate is the overnight rate at which US banks lend to each other. It is the oft-quoted headline rate set by the Federal Reserve at its FOMC meetings. It is set as a range, for example 4.75%-5.00%, though the upper limit (in that case 5.00%) is the quoted figure. Market expectations for future Fed funds rate are tracked by the CME FedWatch tool, which shapes how many financial markets behave in anticipation of future Federal Reserve monetary policy decisions.

Economic Indicator

FOMC Minutes

FOMC stands for The Federal Open Market Committee that organizes 8 meetings in a year and reviews economic and financial conditions, determines the appropriate stance of monetary policy and assesses the risks to its long-run goals of price stability and sustainable economic growth. FOMC Minutes are released by the Board of Governors of the Federal Reserve and are a clear guide to the future US interest rate policy.

Next release: Wed Jul 08, 2026 18:00

Frequency: Irregular

Consensus: -

Previous: -

Source: Federal Reserve

Minutes of the Federal Open Market Committee (FOMC) is usually published three weeks after the day of the policy decision. Investors look for clues regarding the policy outlook in this publication alongside the vote split. A bullish tone is likely to provide a boost to the greenback while a dovish stance is seen as USD-negative. It needs to be noted that the market reaction to FOMC Minutes could be delayed as news outlets don’t have access to the publication before the release, unlike the FOMC’s Policy Statement.

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.