The Dollar has some good reasons to be firming

Outlook

Yesterday we got what we wanted, a surge in the dollar due to too much economic power and despite expectations of some small disinflation in Friday’s PCE.

We were surprised the yields went into such a frenzy. Reuters notes that it’s not just the US issuing new debt—it’s a global thing, with the Bund also hitting a six-month high earlier today. “All of which makes an uncomfortable backdrop to what's set to be the heaviest month of the year for net sovereign debt issuance. New government bond supply net of redemptions and central bank purchases is due to rise to $340 billion in June for the United States, euro zone and Britain, according to data from lender BNP Paribas.”

Then there are elections, the S. African rand falling as the voting seems against the ruling party, EC Parliament and India next week, and Mexico and the UK in early July. In the US, the first presidential debate is at end-June.

Then there is tomorrow’s PCE inflation. A small (0.1%) dip is expected in the core and both the US and eurozone may end up with the same year-over-year. One report has it that the drop in eurozone unemployment cut down rate cut expectations in the eurozone, but never mind—the ECB has been telegraphing next week’s cut for a very long time now. The current mood, given the surge in yields, is that the US inflation report will not change the Fed’s tune—we need a sustainable drop in inflation, confidence in that drop and patience until we see it, etc.

That doesn’t mean we can’t get a spikey dollar sell-off on the release. Tomorrow morning is not a good time to trade the news.

At some later point we will get tired of the reasons for the dollar to be strong and go back to how unfair it is, especially for emerging markets paying dollar debt. This gets tiresome. (Also tiresome is anything about Elon Musk, Nvidia and even the Trump trial.)

Fatigue can be a very real contributor to sentiment. Together with profit-taking, we could easily see a dollar retreat next week.

Also in the mix is the dollar/yen retreating from the danger zone where intervention can get real again. Tomorrow we get Tokyo CPI, which fell last time but is forecast to go back up this time, led by (you guessed it) services. On the whole, the Japanese economy is pretty firm, and an additional shove to the upside in the JGB is not silly. It’s still not high enough to lure Japanese investors, who bought ¥2.2 trillion in foreign bonds last week. This includes US Treasuries.

Tidbit: The chief economics reporter at the WSJ, Greg Ip, used to be the top Fed-watcher. Today his article is about tariffs, not the coming inflation data and how the Fed will respond. What does this mean?

Forecast

The dollar has some good reasons to be firming, chiefly the rise in yields and behind that, a lot of debt issuance plus the Fed signaling there is some time way to go before a rate cut.

The latest CME FedWatch tool shows only a 41.7% chance of a single cut by the Dec meeting, although a 29.9% chance of a second one. As long as the US economy keeps rip-roaring along, it’s hard to see a change. But if we start to get rising unemployment or other negatives, the market can turn on a dime and restore the idea of more and/or earlier cuts. Nerves are starting to fray, not so much from the uncertainty as from the outsized responses to the smallest bit of information.

We expect the dollar to continue on the strong side, but the source of any additional upside pushes not known.

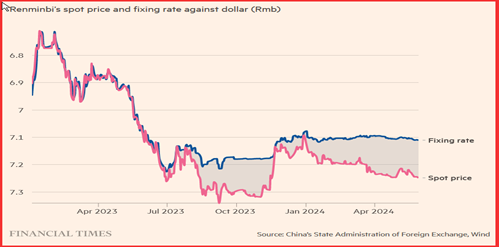

Tidbit: The FT reports that some analysts say it’s time for the Chinese central bank to do a one-time re-calibration of the renminbi, as in 2015. “Markets are pushing for a weaker yuan to reflect the gap in bond yields with the US — 10-year Treasury yields trade at 4.57 per cent, while 10-year Chinese government bonds offer just 2.3 per cent.” The IMF concurs. “First deputy managing director Gita Gopinath urged Beijing on Wednesday to consider allowing more flexibility on its exchange rate, saying this “would reduce deflation risks and help absorb external shocks’.”

The chart shows the spread between the fixing rate And the 2% band around it that China wants the market to hold. This is despite the economy not “needing” devaluation for inflation, trade or other reasons.

Reasons for the Fed to cut rates

Avoid embarrassment from getting inflation wrong twice.

Normalize the yield curve.

Head off any recessionary tendencies.

Help housing via mortgage rates.

Help banks rollover commercial property loans.

Help the stock market.

Synchronize with the ECB (and Riksbank and SNB)

Help the current White House and/or avoid accusations of political bias if delayed to after the Nov election.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat