Political market moves more interesting than boring old data

Outlook:

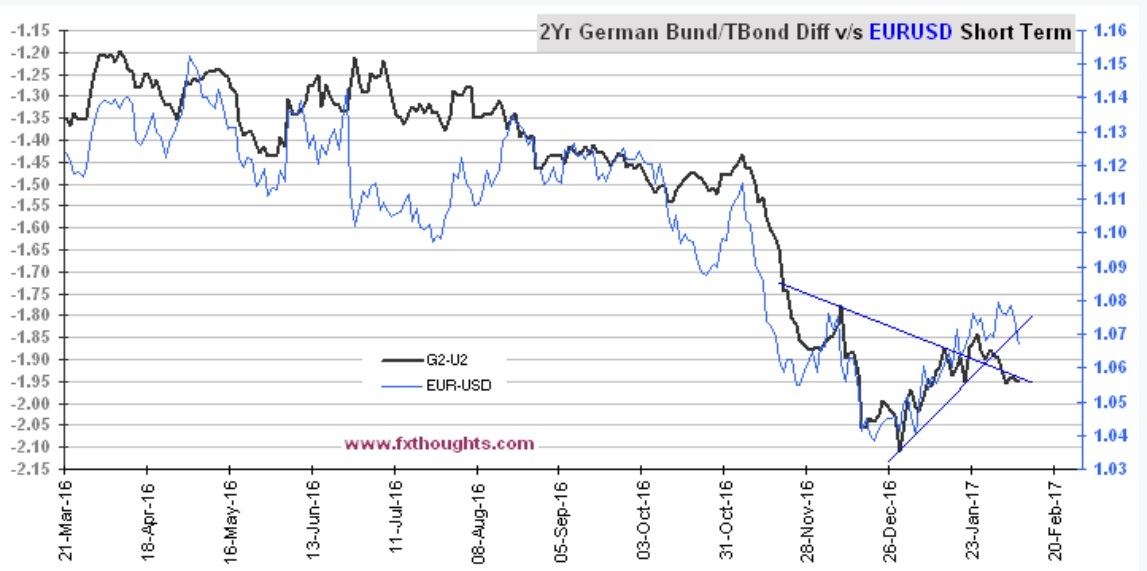

The political aspects of market moves are more interesting than boring old data, but first things first. We named the section on yields "The Main Event" because currencies track the yield differential. This correlation waxes and wanes over time, but has been back mostly in force for several years now and is neglected at our peril.

The chart below shows the 2-year differential against the euro/dollar. The euro had gotten ahead of itself, continuing to rise while the differential was falling. That implies the euro's retreat is corrective in nature.

The other factors behind the dollar's surprise recovery yesterday and overnight are less compelling. First, Philadelphia Fed Pres Harker added his voice to Evans and Williams, saying "I think March is on the table. I would never take a meeting off the table." Harker also said he agrees with three hikes. We are not sure this dog will fight. If two Feds saying "three and maybe March" failed to impress, does a third Fed constitute some critical mass? No. The market continues to price in only two hikes this year and the probability of March is still low, according to the CME's Fed Watch.

A little more impressive is the new perception that the Trump tax and fiscal initiatives will be delayed. For one thing, Congress has the power of the purse, not the president, and it's not clear the Plub leaders are going to fall to their knees—not after having made such a fuss over the past eight years about fiscal rectitude and downsizing the federal government. The Tea Party per se may be quiet, but it's too soon to schedule the funeral. Those who embrace the goals of reducing the deficit and aiming for a balanced budget are not dead—and include a surprising number of libs and Dems.

The third factor is the French far-right LePen making a splash over the weekend and announcing she would take France out of the eurozone. After Grexit and Brexit, this kind of talk is damaging, even if LePen's chances are quite low. She is against globalization, immigration from Muslim countries, and for "France First." It doesn't help that other French politicos (Sarkozy, Fillon) are being charged with ethical lapses that reach criminal proportions. This is actually worse than the FBI muttering about Clinton.

Having said that, Market News reports "An Ifop-Fiducial poll showed Macron defeating the far right National Front leader Le Pen in a runoff vote on May 7 by a margin of 63% to 37%. That compared to 65% to 35% margin in an Opinionway poll earlier on Monday. The Ifop poll showed Le Pen continuing to lead in the first-round ballot on April 23, taking 25.5% of the vote, compared with 20.5% for Macron and 18.5% for the conservative former prime minister Francois Fillon." If no winner emerges on April 23, a run-off will be held May 7.

Normally we would brush off LePen, but then, we brushed off Trump as a repulsive clown and that was a mistake. France's economy is ten times the size of Greece. A LePen victory would push the euro down below parity, according to big bank economists, by more than Grexit.

And our hero Draghi made a terrible, awful mistake yesterday by even talking about LePen's Frexit idea. Bloomberg had a strange article that ends abruptly and is headlined "Draghi Says Euro Is Irreversible as Le Pen Urges French Exit." Speaking to the European Parliament Committee on Economic and Monetary Affairs yesterday, Draghi responded to a question about Frexit. He said in both English and Italian, the euro is irreversible. "L'euro e' irrevocabile, the euro is irrevocable. Questo e' il trattato, this is the treaty."

Unfortunately, this is not true. The Treaty doesn't contain a policy and procedures section for those departing the European Unions, but that doesn't mean a country cannot repudiate any treaty it chooses to repudiate. A treaty is not a life sentence. The Bloomberg story refers to a letter he wrote on Jan 18 to EU parliamentarians from Italy, where the Five Star party also embraces exit. "If a country were to leave the Eurosystem, its national central bank's claims on or liabilities to the ECB would need to be settled in full."

Here's the kicker: "Zanni said that response acknowledged that countries can leave. "I wanted to bring up the issue of exit from the euro and how it can happen. Draghi has now clearly admitted that such an exit is possible and now there is need to have more clarity about the cost. I'm sure that in case of Italy's exit from the euro, benefits exceed costs."

In response to additional questions about those liabilities, Draghi said "I cannot answer a question that is based on hypotheses, on assumptions which are not foreseen" [by the EU treaties]. What I could do is send you a written answer which compares our Target2 system with the Federal Reserve-based system."

Is this a Holy Cow! moment? Time will tell. We are actually not done with Greece yet. The IMF is dithering about whether to re-join the troika. Germany threatened to withdraw from the latest bailout tranche unless the IMF participates, and repeated the threat yesterday. But the IMF continues to believe the debts are unsustainable and will rise to triple GDP by 2060. The FT claims it has seen a new IMF report that doesn't retreat from this judgment.

As for the real reason Draghi was speaking to the EU Parliament, he repeated that "the pickup in headline inflation in December and in January largely reflects sizeable upward base effects and recent increases in energy prices." In policy terms, "we should not react to individual data points and short-lived increases in inflation. If the inflation outlook becomes less favorable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council is prepared to increase the asset purchase program in terms of size and/or duration." Increase, not decrease. There is no other way to label this but "dovish."

Meanwhile, the situation in the US remains the biggest of the political considerations. Trump is in no hurry to launch tax reform and fiscal stimulus. We will get them but not right away, postposing a resumption of rising yields. We saw a mention somewhere that use of the word "uncertainty" has grown by leaps and bounds. Some analysts are worrying about Trump perhaps wanting to revive a "deal" like the Plaza Accord in 1985. This particular idea comes from TD Securities and once said out loud, cannot be unsaid. For those of us who lived and traded through the Plaza Accord, the phrase brings back nightmares. The Plaza Accord said the US dollar is too strong and needs to be managed downward against the Deutschemark and yen. The only party to the G5 agreement who took real action was Japan, as Paul Volcker writes about in his book Changing Fortunes, still the best-ever book on FX.

The TD Securities strategist makes trenchant points. "Continued aggressive statements designed to weaken the USD and pressure to structure deals like the 1985 Plaza Accord, or even suggestions the Fed play a role in pushing the government agenda could well be in the cards going forward. This, along with the risk of global trade and currency wars likely mean that the market appetite for safe haven assets like gold may become increasingly voracious, as we head deeper into the President's four-year mandate."

Popular protests against Trump around the country and around the world are taking a toll. The one thing a narcissist dislikes the most is being embarrassed, as TV comedy shows appreciate. Unfortunately, the expected response is more impulsive lashing out—and an enemies list. Comparisons with Nixon abound. Trump likes to dish out the insults but can't take them himself. The list of those who have offended Trump is growing by leaps and bounds and here's the problem—we don't know at whom he will lash out in retribution. It could be some innocent party... like the Japanese, who visit Washington on Friday.

Bloomberg reports "Trump was barred from U.K. Parliament over ‘racism and sexism.' House of Commons Speaker John Bercow said Trump must not be allowed to address the U.K. Parliament during a state visit to Britain. Barack Obama, Nelson Mandela, Angela Merkel and Pope Benedict XVI have all been invited to speak to members of the House of Commons and the House of Lords." The debate (C-Span, Sunday nights) was hilarious. Boris Johnson kept saying the UK has to work to get the best trade deal--and kept getting shouted down.

Bottom line—Trump is not yet done with trade and currency wars. We thought he would race on to other matters and come back later to tidy up. Market players thought he would deliver the "good" policies right away on taxes and fiscal spending. But if Trump is going to linger on the trade and currency issues, we must expect the same response we had over the first two weeks—a weaker dollar. The current upswing is probably seen as unwelcome in the White House. Get ready for a lashing.

| Current | Signal | Signal | Signal | |||

| Currency | Spot | Position | Strength | Date | Rate | Gain/Loss |

| USD/JPY | 112.28 | SHORT USD | WEAK | 01/05/17 | 115.93 | 3.15% |

| GBP/USD | 1.2369 | LONG GBP | WEAK | 01/24/17 | 1.2451 | -0.66% |

| EUR/USD | 1.0663 | LONG EURO | WEAK | 01/10/17 | 1.0587 | 0.72% |

| EUR/JPY | 119.74 | SHORT EURO | WEAK | 02/03/17 | 121.56 | 1.50% |

| EUR/GBP | 0.8620 | LONG EURO | WEAK | 02/06/17 | 0.8605 | 0.17% |

| USD/CHF | 0.9993 | SHORT USD | WEAK | 01/05/17 | 1.0113 | 1.19% |

| USD/CAD | 1.3195 | SHORT USD | WEAK | 01/05/17 | 1.3253 | 0.44% |

| NZD/USD | 0.7297 | LONG NZD | STRONG | 01/10/17 | 0.7014 | 4.03% |

| AUD/USD | 0.7618 | LONG AUD | WEAK | 01/05/17 | 0.7343 | 3.75% |

| AUD/JPY | 85.53 | LONG AUD | STRONG | 10/06/16 | 78.48 | 8.98% |

| USD/MXN | 20.7116 | SHORT USD | WEAK | 01/31/17 | 20.8108 | 0.48% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat