EUR/USD floating on air, unsupported by Yields

Outlook:

We get US PPI today, but it's tomorrow's CPI and retail sales that count. Actually, it's the forward guidance and new economic forecast from the Fed that count. The rate hike itself is a given (or nearly so at a 95.8% probability in the CME FedWatch) but September is still losing ground at 23.6%. It was 28.6% early yesterday.

While the 10-year is rising only moderately off the scary low last week, the two-year is doing a lot better. The 2-year yield closed at 1.359% (from 1.338% on Friday), the best since March 15, according to the WSJ. Yesterday the Treasury muddied the water with $100 billion in four offerings (and we get $12 billion in 30-tears plus a 4-week bill auction today). Market expectations of a slowly moving Fed boosted demand for 3-year notes yesterday ($24 billion), with demand at the highest since Dec 2015, according to the WSJ. "The highlight was 65.6% indirect bidding, a proxy for foreign demand, which was the highest since a record of 68.6% in November 2009." A lousy day in the stock market may have helped fixed income demand a bit, too.

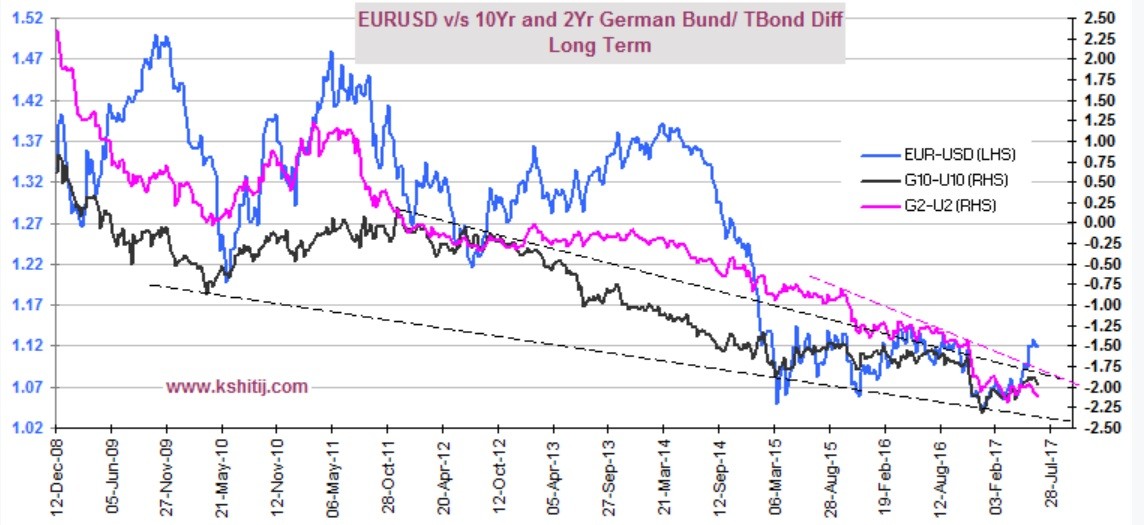

Here's the problem: the 2-year is considered more sensitive to the Fed than the 10-year, even though we tend to get a better correlation of currency moves with the 10-year than the 2-year. Below is the 2-year differential chart against the EUR/USD. The divergence is obvious—and worrying. It looks like the euro is floating on air, unsupported by yield.

The 10-year also shows divergence, if less than the 2-year. Why is the euro outperforming the differential? Reason One is expectation of the ECB relenting on normalization at some point later this year, perhaps as early as September. Reason Two is politics—perhaps. The euro gains strength from a fairly stable political situation, at least in comparison to conditions earlier this year, while the US can be said to have an albatross around its next. Whether you think the albatross is weak inflation or Trump doesn't matter.

Or maybe not. The euro seems to have an inherent advantage over both the 2-year and 10-year differential. It was especially striking in 2009, 2011 and 2014. See the combined chart. The blue EUR line soars above the differential lines.

We continue to wonder why we have to go to India to get these charts when they should be the mainstay of every financial press discussion about currencies. At a guess, it's because editors see FX as secondary and so do not assign that beat to the best reporters. Market News is the key exception, but alas, doesn't publish charts, just prose.

What is the bottom line? You short the euro at your peril. It has demonstrated a tendency to outper-form its yield disadvantage. This is why we keep saying that the US needs a clear and obvious yield advantage, a big fat premium, to overcome the pro-euro bias (or the dollar's perennial disadvantage). We guess this is about 250-350 bp. Whatever it its, it's more than the 200 bp we are getting today. And since there is nothing on the US inflation horizon that will carry the yield advantage higher, we are re-luctant to consider the Fed decision this week as heralding a new pro-dollar day.

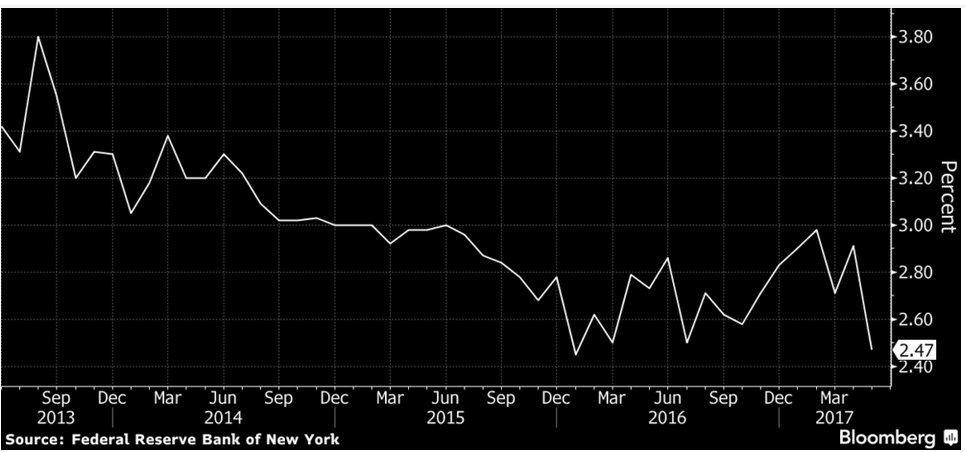

This is because inflation is not keeping up its end of the bargain. Bloomberg reports a survey by the NY Fed showing inflation expectations are falling. In May, expectations fell to the lowest in the 4-year history of the survey, 2.47% over the next three years, down even from April's 2.91%. See the chart. Granted, the Yellen Fed has its own ideas beyond a single survey by the NY Fed, and a newish one at that, but the University of Michigan also finds inflation expectations falling.

The September rate hike is in real jeopardy. Even if the Fed persists and postpones to December in or-der to fulfill its projection of three hikes this year, markets will not necessarily give it credit. Thus we face another Fed confidence issue as well as an advance of moxie in fixed income.

In the UK, PM May has delivered all her mea culpas and wants to move on. Bloomberg, for one, se-lects the trade deal as probably the best first place to get started. The Norway model has long been tout-ed as the most practical—membership in the 28-country EEA customs union. But Brexit Secretary Da-vis has taken a hard line and would prefer to leave the single market altogether rather than accept one of its provisions—that labor be free to move among members. One giant disadvantage of the Norway model is that Nigel Farage likes it. But former Chancellor Osborne likes it, too, as a "holding position."

The real reason May can't start with trade is that the EU rejects singling it out for solution ahead of oth-er issues, especially the already committed fees and protection of EU citizens already resident in the UK. These number almost three million persons. The UK needs a path of legal residency or citizenship. Sound familiar?

Back on the US political front, Attorney General Sessions will testify this afternoon to the same Senate Intelligence Committee that served as host for former FBI director last week. Sessions has already been charged with lying under oath about meetings with Russians, so he is very much in the hot seat today. We continue to imagine there was no advantage for the Trump campaign to collude with the Russians. And even the dimmest of Trumpies had to know it was treason. They likely didn't do it. But what they are doing is obstructing the investigation. After recusing himself from all things pertaining to the FBI investigation into the Russia thing, Sessions was involved in firing Comey for investigation the Russia thing.

There was panic talk late yesterday about Trump considering firing special counsel Mueller. This is too much like Watergate to have escaped even the self-obsessed Trump. Impeachment is in the cards unless he cleans up his act, although far down the road. The UK newspaper Telegraph reports that the "latest odds from Ladbrokes showing that he is more likely than not to fail to make it to the end of his first term in office.

"Their latest odds are as follows:

-

Impeachment or resignation before 2020: 4/7 (64 per cent chance)

-

To serve full first term: 5/4 (44.4 per cent chance)"

Impeachment is far, far off if it happens at all. But accepting money from foreign governments, as Trump does by continuing to own the Washington, DC hotel, may violate the emoluments clause. The State of Delaware and the District of Columbia are charging Trump with that violation. Legal scholars have already found arguments that could help Trump escape—this time.

It must be admitted that unless Trump does or says something to cause a Crisis, these political developments are not much affecting the international markets. As the WSJ reported, demand for US Treasuries in all maturities was very high yesterday.

But as we have noted before, experts know little about "contamination" and continue to study it fever-ishly. Contamination manifests itself mostly in emerging markets, as we saw in the Thai-Brazil-Russia crisis back in the 1990's that took down Long-Term Capital, but also in the market for mortgage-based securities in 2008-09, the market for specific European sovereign paper during the Grexit crisis in 2011-2012, and many other lesser events.

The real risk from contamination is liquidity flying out the door. So far in the Trump saga, that seems not to be a worry.

Note to Readers: RTS has launched a Trade Copier service. We place our trades from the Afternoon Traders' Advisory in the retail spot market and your MT4 account mirrors the trades taken in the RTS account. You don't have to lift a finger. You get to pick how much leverage and exactly which curren-cies you want to include. If you are interested, please contact Paul Harris at [email protected] or visit http://www.rtsforex.com/trade-copier/.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 110.09 | SHORT USD | 05/18/17 | WEAK | 110.36 | 0.24% |

| GBP/USD | 1.2707 | SHORT GBP | 06/12/17 | STRONG | 1.2701 | -0.05% |

| EUR/USD | 1.1207 | SHORT EURO | 06/12/17 | WEAK | 1.1218 | 0.10% |

| EUR/JPY | 123.38 | SHORT EURO | 07/08/17 | WEAK | 123.65 | 0.22% |

| EUR/GBP | 0.8819 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 3.88% |

| USD/CHF | 0.9677 | LONG USD | 06/12/17 | WEAK | 0.9675 | 0.02% |

| USD/CAD | 1.3270 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 2.58% |

| NZD/USD | 0.7223 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 2.28% |

| AUD/USD | 0.7543 | LONG AUD | 06/08/17 | WEAK | 0.7548 | -0.07% |

| AUD/JPY | 83.06 | SHORT AUD | 06/01/17 | WEAK | 82.19 | -1.06% |

| USD/MXN | 18.1257 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 3.12% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat