Yields and the Dollar are in the middle of a whirlwind of conflicting ideas

Yields and the dollar are in the middle of a whirlwind of conflicting ideas. One idea is that CPI inflation is stalled at too high over the target, but the Fed needs to take advantage of the Dec policy meeting to cut rates before Trump policies drive inflation back up again.

This is not how the Fed tends to conduct itself but Fed funds betting seems to follow that script. On Tuesday evening, the CME FedWatch tool had 41.3% betting the Fed keeps rates the same. Last evening that had fallen to 17.2%. The probability of the Dec rate cut rose from 58.7% on Tuesday to 82.8% yesterday. Granted, this is a choppy series, which is itself a warning sign that sentiment is uncertain and fickle.

It's confusing that we are getting a new 52-week dollar index high at the same time. As Reuters phrases it, “Ordinarily, if the chances of a rate cut rise above 80% from nearer 60% just 24 hours earlier, the dollar would fall sharply. But investors are latching on more to the longer-term view that ultimately, King Dollar will rule supreme under Trump.”

In other words, a Dec rate cut is good for the dollar and yields because we all know it’s not going to last. One analyst writes that when Mr. Powell speaks today, he may clear up “how rate cuts and a lack of rate cuts are, at the same time, positive for the dollar and the stock market.”

This is having cake and eating it, too, and not sustainable.

Another factor may be today’s jobless claims, expected a bit higher than the last release (223,000) but still under the 16-month high in mid-Oct at 258,000.

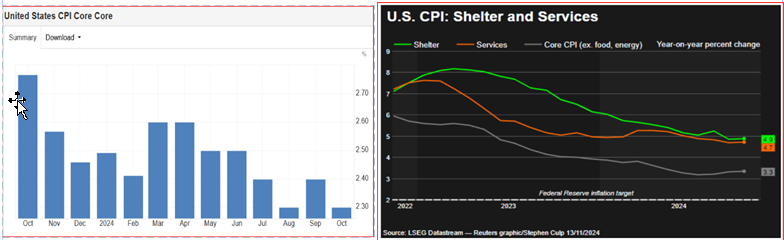

The facts on inflation and other data like claims =is taking a back seat to the Trump outlook. That doesn’t mean we still don’t owe ourselves a proper understanding of the data. CPI yesterday came in exactly as expected but the reporting was biassed. True, headline ticked up from 2.4% to 2.6%, but core remained the same. Some press reports had a rise in inflation while others said inflation did not go up, as though staying the same in a 3-month stall doesn’t alter perception.

Sticky price problems remain, specifically in core services, up 4.8% y/y, the same as the month before. On the 3-month basis, core services actually rose to 4.5% from 4.4% but on the 6-month over-six month basis, decelerated to 3.6% annualized.

The biggie, of course, is still shelter, specifically owners equivalent rent or OER.It rose faster in October to 4.9% and has been hovering around 5% all year. On the 3-month basis, OER CPI rose to 5% for the third month of acceleration. Then there’s rent, outpacing home valuations, and all those automotive things—car insurance up 51% from 2022.

The BLS doesn’t publish supercore (services less food, energy, and shelter) but a few others do, including Trading Economics, which names it “core core.” See the chart. CPI core core fell to 2.3% in Oct from 2.4%. This is probably why the Fed funds betting returned to expecting a Fed rate cut in Dec. But taking energy out is a big part of it. See the St. Louis Fed version. Levelling off, but still high.

Bottom line, you can fiddle with different measurements, different timeframes, and base effects, but the fact remains that inflation is not whipped in some very important categories for the average Joe. The Fed can make the argument that enough progress is not being made to justify a Dec rate cut. Again, this is not how the market sees it.

We shall see if PCE says the same thing as CPI. We don’t get the Fed’s preferred measure until the day before Thanksgiving (Nov 27), which tends to turn into a 4-day weekend and thin out all US trading. Note that we get the revised Atlanta Fed GDPNow tomorrow. It was 2.5% last time.

Most economists have no doubt the Trump initiatives are inflationary. The WSJ of economist had 68% agreeing that prices will rise under Trump (and higher than under Harris). Yesterday former TreasSec Summers told CNN “If he carries through on what he said during his campaign, there will be an inflation shock significantly greater than the one the country suffered in 2021.” This got a response from the Trump team, calling it absurd. Summers can be a real jerk and was wrong about stagflation, but nobody reputatble and qualified is arguing with him now.

Forecast

The FX market is confused. It is accepting two opposing sets of ideas at the same time, and also clinging to the risk-off idea that even if the source of rising risk is the US, the dollar should be the beneficiary. You’d think such contradictions would not be sustainable but we have seen it before (Grexit).

Until we get right on top of the Fed’s Dec rate decision, we can’t see what will jump out and change the landscape. If the Fed declines to cut in Dec, it will be a Shock (and at least somewhat political), but even such a development is probably not enough to knock the dollar off its pedestal (as the embedded inflation forecast in such a move would imply).

Political Tidbit: One of the most repulsive members of Congress was just named as the choice for attorney general—Matt Gaetz. He practiced law for about ten minutes before going into politics. Check out the Wikipedia entry, which includes this: ” In June 2021, Gaetz was one of 21 House Republicans to vote against a resolution to give the Congressional Gold Medal to police officers who defended the U.S. Capitol on January 6.” It seems improbable he can pass approval by the Senate while still under investigation in the House for soliciting minors.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat