What Donald Trump’s victory means for China

Chinese assets sold off after the Trump 2.0 outcome, but policymakers should be more prepared this time around. China’s stimulus plans and currency management responses are likely to be the most watched factors in the months ahead.

Trump's return was expected in China

After the last few months of polling foreshadowed a very tight contest, what we ultimately got was the least dramatic election day since Donald Trump first arrived on the political scene, with a “Red Wave” outcome looking likely at the time of writing.

As we found in our October trip to Shanghai and Beijing, the overwhelming majority of Chinese clients have been expecting a Trump victory. Indeed, many of those who expressed a preference either way indicated that a Trump win would be preferable.

It looks like they will be getting their preferred outcome, but as the old saying goes, 'be careful what you wish for, lest it come true'.

What would a second Trump presidency mean for China? From our perspective, this outcome marks a return to uncertainty next year, where scenario-altering developments could come at any moment's notice through a Tweet (or perhaps a Truth Social post). Right now, it remains difficult to gauge the impact as election trail rhetoric does not always translate into actual policy action, so these are just our initial thoughts on the information we have right now.

FX impact: Trump win a net negative for the CNY but no dramatic changes expected

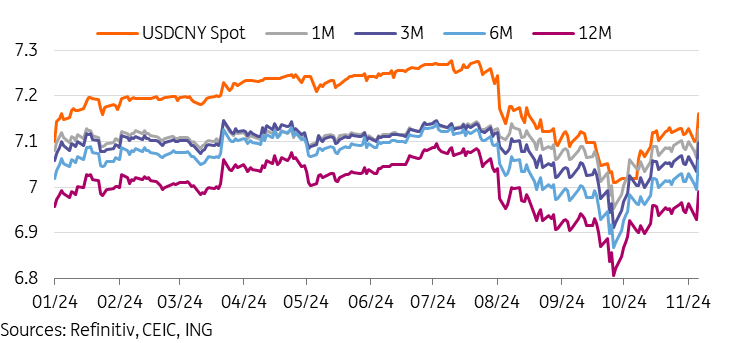

The initial market reaction to a Trump win has been clearly negative for the renminbi, moving up from 7.10 to as high as 7.17. Our view on the topic is in line with the market’s initial movements in that a Trump victory creates an environment for a weaker RMB.

How does a Trump win impact the main factors for the USD/CNY?

-

Interest rate spreads: our house view has been that a Trump win could lead to lead to a less dovish Fed in 2025, which will also limit the amount of narrowing for US-China spreads and thus one of the main catalysts for RMB appreciation.

-

Trade and investment flows: in a vacuum, this front should be negative for the RMB, as exports to the US could take a hit, and high tariffs may encourage Chinese firms with a high proportion of US customers to accelerate expansions abroad to mitigate the impact of tariffs.

-

PBOC stance: Will China purposely devalue the RMB in response to a Trump win and potential tariffs?

-

This was a commonly discussed topic throughout the year, and while it's impossible to say for sure, we do not think this is a likely outcome. China’s priority on currency stabilisation is not tied to short-term trade flows but is likely to limit capital outflow pressures in the near term and facilitate RMB trade settlement and internationalisation in the longer term.

-

As a result, we expect the PBOC to continue to resist large movements in either direction for the RMB, and as outlined above, this policy does not look likely to change dramatically.

-

Will the RMB repeat its Trade War 1.0 performance, where it moved sharply weaker? In a vacuum, the prospect of the start of another trade war certainly should do the RMB no favours. However, there are several key differences this time around:

-

Shock value: The first trade war was a game changer; many companies were caught off guard, and investors were left scrambling. This time around, Trump’s proposed tariffs have been in consideration for some time and should come as no major surprise.

-

Global investor positioning: sentiment on China has been in what we have characterised “excessive pessimism” for some time. Short China and a CNH carry trades have been common themes in markets for much of 2024. There should be less of a dramatic shift for global investors this time around.

-

Trade War 1.0 took place in a modest Fed tightening cycle. Barring a major surprise, a Trade War 2.0 will likely take place during a modest Fed easing cycle.

Overall, we expect the CNY outlook to be a little weaker with a Trump win in the books, and risks to our forecasts are now tilted toward a weaker CNY. We may consider extending the upper bound of our 2025 fluctuation band (currently 6.90-7.20) a little higher if we get signals of stronger action against China, though we expect the PBOC will once again ramp up intervention to prevent excessive depreciation; odds of a move past the 2023 highs of 7.34 are still relatively small unless policymakers abandon the currency stability objective. Furthermore, in our main election wrap-up report, our team expects that "the earliest time for (tariffs) to occur will be the third quarter of 2025, with a more likely time frame of the fourth quarter of 2025/first quarter of 2026", which could mean the impact on the 2025 CNY outlook could end up relatively limited until the tail end of next year. We still expect the CNY to remain a low-volatility currency compared to other Asian currencies.

CNY spot and NDFs moved weaker in the election aftermath

Growth impact: Will likely drag from growth and outward investment be offset by stronger stimulus?

There are many moving pieces and it will be very difficult to gauge until there are concrete policies in place from both sides. We expect that some market participants may end up having a knee-jerk reaction to downgrade forecasts, but we are holding our 2025 forecasts on growth until there is more clarity. Ultimately, our view is that domestic developments should play a larger role in the growth outlook than the potential shock from an escalation of tariffs.

While Trump is widely expected to ramp up tariffs in his second term, when and how this will be done are still up for discussion. We think that the 60% tariff call may be a starting point for negotiations rather than a set-in-stone number – you may recall that the first Trade War saw a truce after an agreement from China to increase imports of US agricultural goods. There are two roads to narrowing the US-China trade deficit: either reducing China's exports to the US or increasing China’s imports of US goods. Given the respective impacts on inflation and job creation, we would assume the latter would also be a welcome outcome for the Trump administration.

-

If we do take the 60% tariff threat at face value, despite various preparations being made for a potential Trump return, there is no denying that a 60% blanket tariff would have a significant impact on Chinese exports to the US.

-

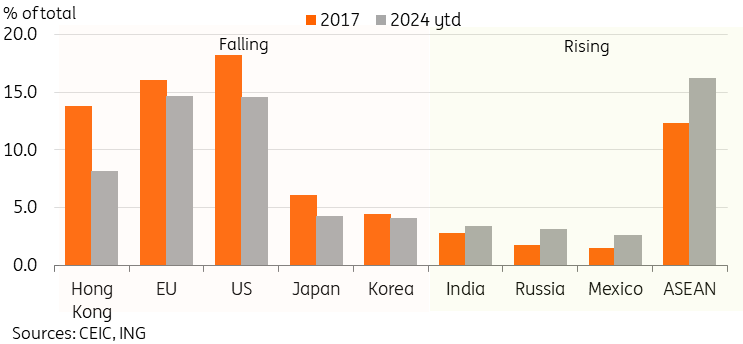

It’s also worth noting that the US has also gradually become a less important export destination for China as well since the first trade war, with exports to the US falling from 18.2% to 14.3% of total exports in 2024 year-to-date.

-

A question to ask is will the US target Chinese companies’ overseas production? Is this feasible and if so it could lead to a game of cat and mouse and searches for loopholes?

-

China will undoubtedly retaliate if we do get aggressive tariffs from the US. Key import categories including agricultural products, minerals and chemicals, and machinery and mechanical appliances. If tariffs are significant, it could be a catalyst for higher inflation in China as well.

Could a Trump win have a stimulus impact? Over the last few months, a common argument has been that a Trump win and the perceived shock from additional tariffs would lead to a more aggressive stimulus response from China to offset the likely loss from exports.

-

This week’s National People’s Congress concludes on Friday, and the delayed timing from the originally expected late October meeting was very likely at least in part considering the new window gave policymakers a chance to address a possible Trump win.

-

In our view, the odds for a larger policy support package will rise somewhat with a Trump victory, though it may not necessarily be announced immediately. According to a recent Reuters report, the expected package size is RMB 10tn over 3-5 years, with RMB 6tn spent on addressing local government debt issues and RMB 4tn on supporting the property market.

-

Top officials have signalled multiple times this week that the PBOC is ready and able to ease policy further if necessary - we expect to see further rate and RRR cuts moving forward as well as expanded open market operations to help support financial stability whenever necessary.

Chinese exporters have become less reliant on the US in recent years

Net negative impact expected on financial and non-financial flows

Financial flows: the initial Chinese equity market reaction to Trump’s victory showed modest capital outflow pressure.

The larger decline seen in the Hang Seng Index versus onshore indices indicates that foreign investors tended to be more concerned than domestic investors on a Trump win’s impact on Chinese companies.

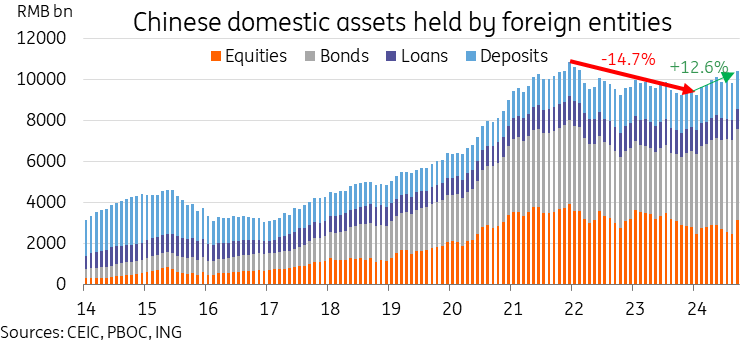

Foreign holdings of Chinese domestic assets fell around 15% from the peak in 2021 to the start of 2024 before rebounding 12.6% since then, in large part thanks to a very strong close to the third quarter. Chinese assets have been underweight by many global investors, and a Trump victory could be a catalyst for some further pullback and a continuation of the “de-risking” trend, especially if we see measures to discourage or ban US investment into Chinese firms. However, we are of the opinion that China’s domestic catalysts, including the upcoming scale and efficacy of stimulus policies, should play a bigger role relative to the US election outcome.

Non-financial flows: Net foreign direct investment into China has cratered to historical lows this year, and new US investment into China has been muted for the last several years already. A Trump win sparking further US-China tension certainly will not help matters on this front. Asymmetric tariffs could accelerate China’s outward direct investment.

Since the first trade war in 2017, the US trade deficits with China have narrowed but widened versus other Asian economies. This increases the odds that China may not be the lone target of Trump’s next possible trade war. However, taking into consideration other geopolitical considerations, tariffs imposed on other Asian economies are expected to be lower than what is ultimately levied on China. If this is the case, we could see an acceleration of outward direct investment from China to at least partially mitigate some of the impact of tariffs.

Trump's win could impact the recent recovery of foreign holdings of Chinese assets

Read the original analysis: What Donald Trump’s victory means for China

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.