Week ahead: Preliminary November PMIs to catch the market’s attention

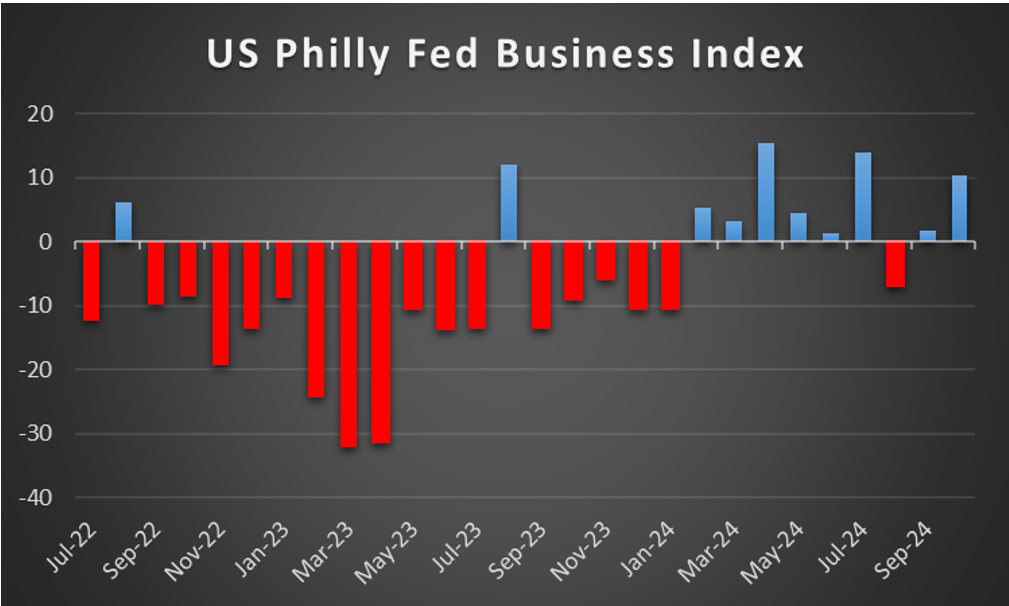

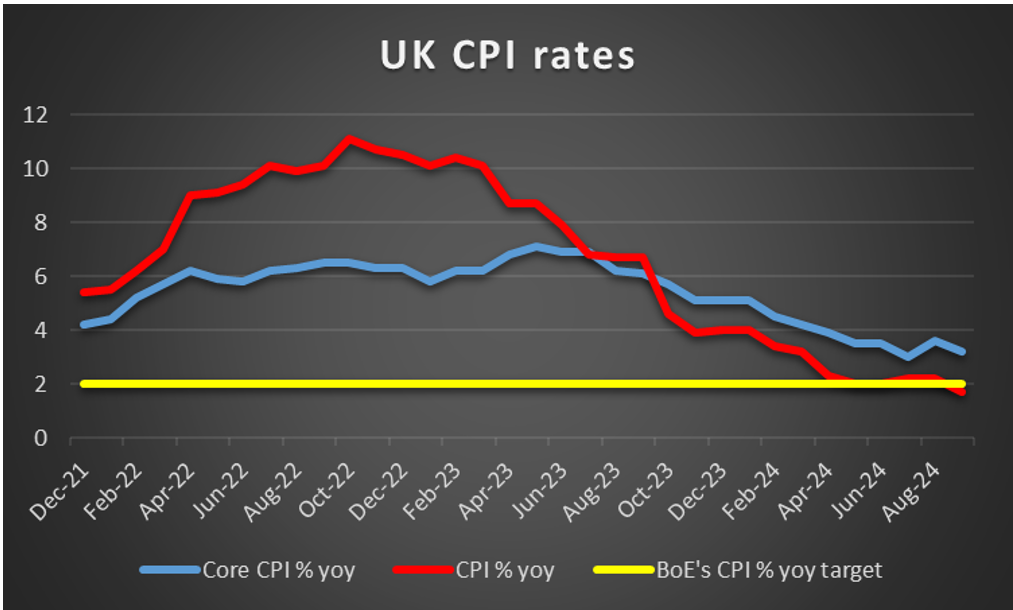

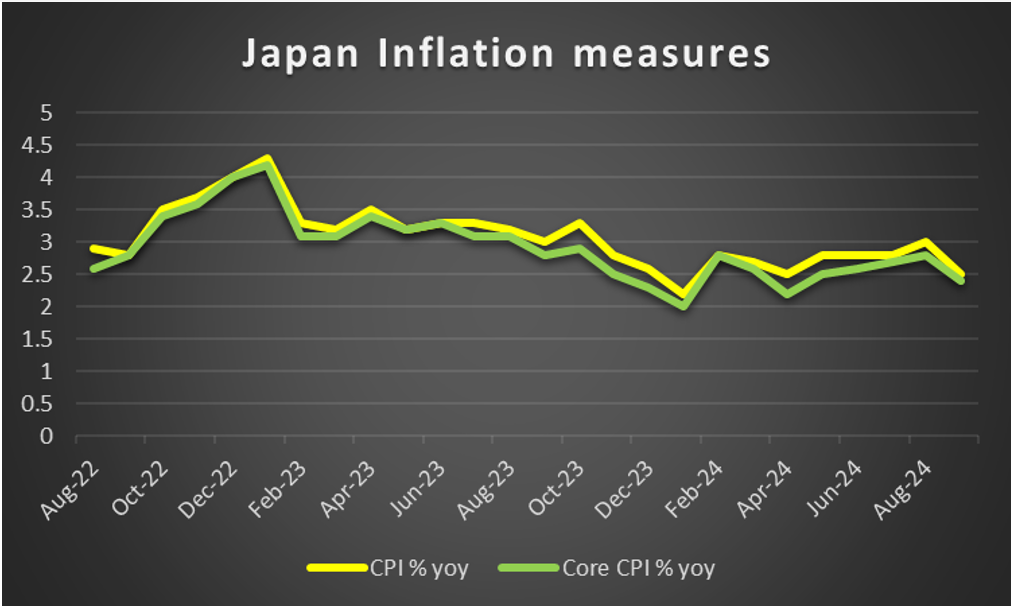

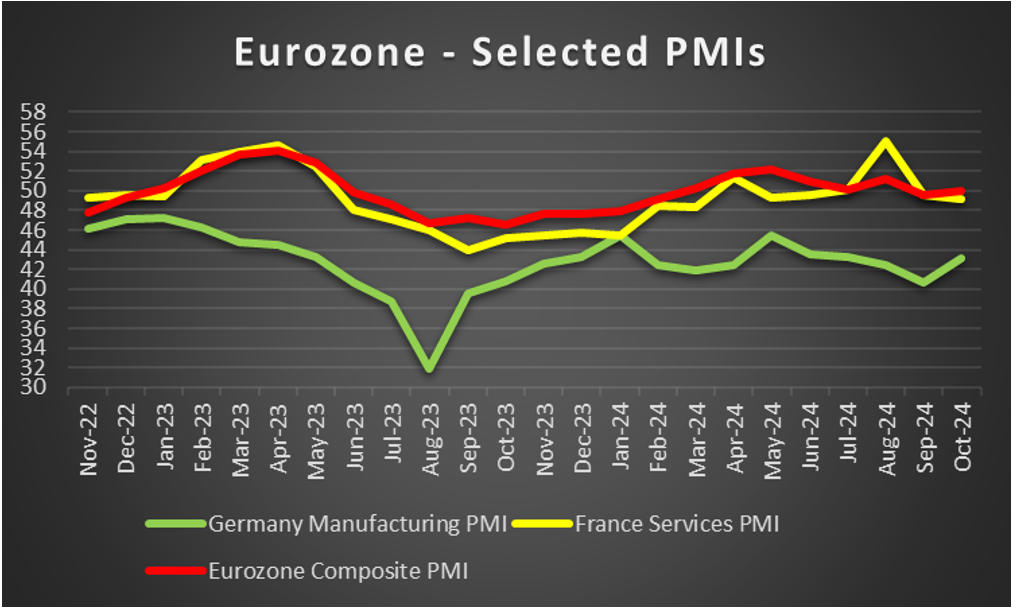

With the dust from the US elections slowly settling down, the week is about to reach its end and we have a look at what next week’s calendar has in store for the markets. On the monetary front, a number of policymakers from various central banks are scheduled to speak, while RBA is to release the minutes of the November meeting on Tuesday, from China PBoC is to release its interest rate decision on Wednesday and from Turkey CBT will be releasing its interest rate decision on Thursday. As for financial releases we start on Monday with Japan’s machinery orders for September and Chain store sales for October and continue with Canada’s House starts for October. On Tuesday we get Eurozone’s and Canada’s CPI rates for October and on Wednesday we note the release of Japan’s trade data and UK’s CPI rates, both being for October. On Thursday we get Norway’s GDP rate for Q3, the UK’s CBI trends for industrial orders for November, the US weekly initial jobless claims figure and November’s Philly Fed Business index as well as Eurozone’s preliminary consumer sentiment for the same month. On Friday we get the preliminary PMI figures of November for Australia, Japan, France, Germany, the Eurozone as a whole, the UK and the US, while we also note the release of Japan’s CPI rates for October, UK’s retail sales also for October, Canada’s retail sales for September and November’s US University of Michigan Consumer Sentiment.

USD – Fundamentals to lead the greenback

Fundamentally for the USD, Trump Trades are still in action supporting the USD, albeit we see the case for some denting of the market sentiment. President elect Donald Trump made headlines as the Republican party secured a majority in the House of Representatives locking in control practically over the US Congress. Yet also his picks for the ministries of the US Government may have taken the markets by surprise, especially the newly formed Department of Government Efficiency (DOGE) which is to be headed by Elon Musk. Marketwise the possibility of Trump starting to slap tariffs on US imports from various countries kept the USD supported in the FX market. Should US economic isolationist tendencies be more outspoken in the coming week we may see them supporting the USD further. On a monetary level, we note that a number of Fed Chairman Powell and other Fed policymakers made the case for an easing of the Fed’s rate cutting path and the market’s expectations for a 25 basis points rate in the December meeting eased over the week. The Fed’s cautiousness towards cutting rates is understandable given that October inflation data showed a persistence of inflationary pressures in the US economy, while on a fiscal level, the Trump economic policies and intentions of imposing trade tariffs, tightening immigration and deepening the deficit hence also raising national debt possibly, may rejuvenate inflationary pressures in the US economy. Should more Fed policymakers highlight the need to slow down the reduction of the interest rates, we may see the USD being supported on a monetary level. On a macro level in the coming week we note the low number of high impact financial releases in the calendar, and expect fundamentals to lead the way for the greenback.

GBP – UK’s October CPI rates eyed

On a macro level we highlight the easing of the tightness of the UK employment market and the release of UK’s GDP rates for Q3, showing a wider-than-expected slowdown in growth for the UK economy over the past quarter. Even worse for the month of September, the UK economy shrunk, while negative signals were sent from the Services, industrial and construction sectors of the economy. We see the case for a darkening of UK’s economic outlook which could weigh on the pound. In the coming week we expect data to be key regarding the pound’s direction and we highlight the release of UK’s October CPI rates for October on Wednesday. Should the rates show further easing of inflationary pressures in the UK economy, we may see the pound slipping as such indications could enhance BoE’s intentions to cut rates at a faster pace. At a macroeconomic level for the pound we would also like to note the release of UK’s retail sales for September and the preliminary PMI figures for November, both due out on Friday and could move the pound. On a monetary level, we note the speech of BoE Governor Bailey on Thursday yet also highlight the market’s expectations for the bank to remain on hold in the December meeting and restart rate cuts in the new year, which in turn may keep the pound supported on a monetary level in the short term. On a political level, we note Chancellor Reeves determination to cut through the red tape in regulation for the UK’s crucial finance industry, which may prove supportive for the pound while intentions to use pensions “mega funds” for investment, “reforming the pension markets decades” could also provide some support for the pound, yet at the same time we tend to remain skeptical for the implementation of such intentions.

JPY – October’s CPI rates in sight

JPY’s weakening against the USD was maintained until today, intensifying our worries for a possible Japanese market intervention operation. The headwinds faced by BoJ in its efforts to normalise its monetary policy seem to have renewed market expectations that the possible rate hikes may be delayed. Even in the summary of opinions of the bank’s latest meeting the divide among BoJ policymakers about the timing of the next rate hike was obvious. Overall we see the case for any further indications of a possible delay of the next rate hike to weigh on JPY in the next week. On a macro level we note the acceleration of Japan’s Corporate goods prices growth rate for October, which may be signalling a possible revival of inflationary pressures in the Japanese economy at a later stage, as producers may have to roll over the increase of prices of raw materials to the consumers. The weakening of the JPY may have played a part in this as it may have made imports more expensive for Japanese businesses. Hence we highlight the release of Japan’s trade data for October with special focus being on the imports figure. Yet on a macroeconomic level the highlight is expected to be the release of Japan’s CPI rates for October on Friday. Should rates show further easing of inflationary pressures in the Japanese economy, we may see the JPY weakening as BoJ’s narrative justifying its intentions for further rate hikes could weaken.

EUR – Preliminary November PMIs to rock the EUR

The USD is passing over the EUR like a juggernaut and some analysts are highlighting the possibility of the pair reaching parity levels. It’s really hard to make the case for EUR bulls practically on all levels of fundamental analysis. On a political level, Eurozone products are a prime target for US President elect imposing tariffs on, Trump is expected to ask for European countries to increase their contribution to NATO and a possible win of Russia in the war in Ukraine tends to worry EU politicians substantially all weighing on the common currency. Furthermore the recent instability of Governance in Germany with the elections being prematurely set for February next year tend to add even more uncertainty for the political outlook of the Eurozone. On a monetary level, the ECB is expected to keep on cutting rates at each meeting and at some point a double rate cut also being possible, also weighing on the single currency. On a macroeconomic level, Eurozone’s HICP acceleration for October is expected to be confirmed next week and despite it being supportive for the EUR, the fact that the ECB had warned for a possible temporary acceleration of the HICP rate as we near the end of the year, practically cuts the support for the common currency. In the coming week, we highlight the release of the November preliminary PMI figures, with special interest being set on Frances’ services sector yet primarily of Germany’s crucial manufacturing sector. Should we see a renewed or even wider contraction of economic activity for the sector being reported, we may see the EUR weakening as the macroeconomic outlook for Germany in particular and the Eurozone as a whole could darken further.

AUD – RBA’s meeting minutes could generate interest for Aussie traders

The calendar of economic releases in the coming week is rather empty for Aussie traders, hence we expect fundamentals to lead AUD. We highlight on Tuesday the release of RBA’s November meeting minutes and should the document show a determination of RBA policymakers in keeping rates high for a prolonged period we may see AUD getting some support on a monetary level. On a deeper fundamental level, Trump’s re-election as President of the US tended to weigh on the Aussie. The prospect of the US imposing additional tariffs on Chinese products could also imply the export of less raw material from Australia towards China. It should be noted that worries for the recovery of the Chinese economy are allready at relatively high levels and the stimulus provided both on a fiscal and monetary levels from the Chinese government and PBoC did not show any substantial positive results yet to lift them. It should be noted that PBoC is to release its interest rate decision next Wednesday, yet the chances for the bank to cut rates again are rather slim. PBoC’s policymakers may opt to wait and see before proceeding with their next move. Overall, should the market sentiment turn sour in the coming week, we may see Aussie suffering as it is perceived as a riskier asset given its commodity related nature.

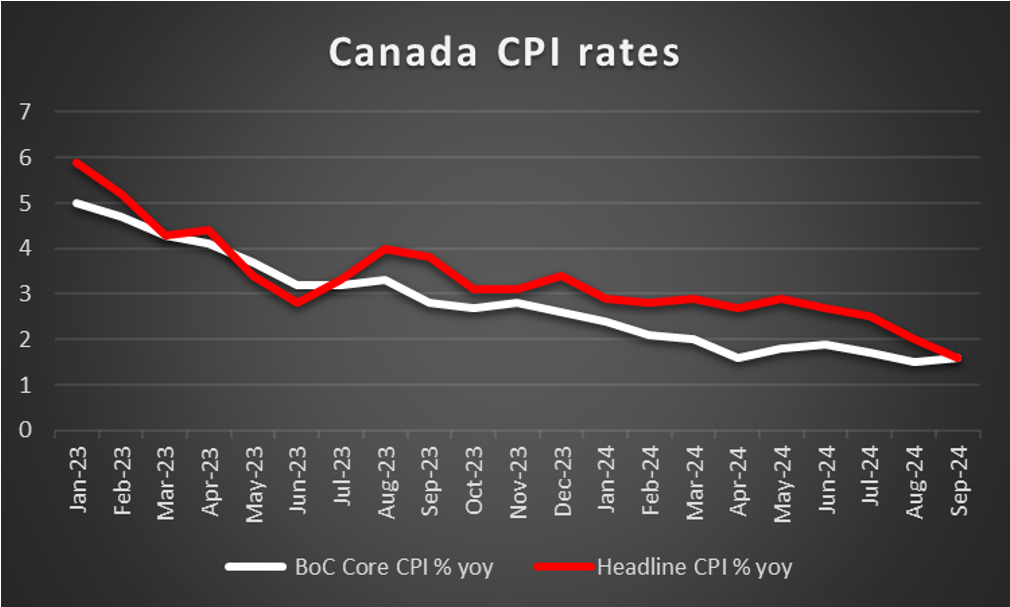

CAD – October’s CPI rates to rock the Loonie

On a macroeconomic level Canada’s employment data tended to send out some mixed signals last

Friday, with the employment change figure dropping more than expected, yet the unemployment rate remained unchanged at 6.5%, despite being expected to tick down. Overall the market reaction to the release tended to be on the bearish side for the CAD and the wider than expected acceleration of the building permits growth rate for September did not provide any comfort for the Loonie. In the coming week, we highlight the release of Canada’s CPI rates for October next Tuesday, and a possible acceleration of the rates could imply some resilience of inflationary pressures in the Canadian economy. In turn such a release could provide some support for the CAD, as the dovishness of BoC may ease. For the time being the market is expecting the bank to proceed with a 25 basis points rate cut in its December meeting, with the alternative being a 50 basis points rate cut, so understandably BoC’s intentions tend to weigh on the CAD on a monetary level. On a more fundamental level, we note the path of oil prices, given Canada’s status as a major oil producing economy and thus should we see oil prices retreating we may see also the CAD slipping further.

General comment

As an epilogue, normally we should expect the influence of the USD over the FX market to ease further given that the number and gravity of high impact financial releases from the US is easing if compared to the current week. Yet Trump as President elect is expected to keep interest about what’s ongoing in the US on a fundamental basis, alive and kicking. As for US stockmarkets the post Trump election rally seems to have been dented and the earnings season is slowly coming to an end, yet in the coming week we still would like to name a few more earnings releases which could make headlines. We make a start with Walmart, Nio and Bidu on Tuesday, Wednesday and Thursday respectively, yet we see the case for Nvidia’s earnings release to be probably the highlight, given the company’s size and the market’s focus on AI technology. As for gold we notice that the negative correlation of the USD with gold’s price sems to have been restored and should we see the USD gaining further we may see gold’s price slipping lower and lower.

Author

Peter Iosif, ACA, MBA

IronFX

Mr. Iosif joined IronFX in 2017 as part of the sales force. His high level of competence and expertise enabled him to climb up the company ladder quickly and move to the IronFX Strategy team as a Research Analyst. Mr.