Macro data doesn’t matter much anymore now that we have the trade war

It’s a pretty thin week for macro data, which likely doesn’t matter much anymore now that we have the trade war. We get US PPI on Friday, which will remind everyone of what happens when we get a supply chain blockage.

The big story going into the new week is JP Morgan raising the probability of recession to 60%, with others agreeing. See the table from Reuters. Also, Fed chief Powell acknowledged that inflation could be “more persistent” now that we have the tariff story.

Mr. Powell was tactful, but Fed funds bets are solidifying at three this year, starting in June, if not a rate cut at every meeting. The CME FedWatch tool shows that by December, a combined 69.3% expect 3.25-3.5% (100 points) or more to 3.0-3.25%.

The Economist magazine cover is headline “Ruination Day” and shows Trump wielding a saw on the map of America. Sunday TV newscaster Smerconish runs a poll every week and delivers the yes/no answers from viewers. Yesterday the question was would Trump tariffs do harm or good “ultimately”? The vote was big, over 70,000 respondents, and the answer all too clear—92% go for harm. Trump is indifferent. Yesterday he said "Sometimes you have to take medicine to fix something."

Asked on Sunday TV whether the administration foresaw the stock market meltdown, trade idiot Navarro declined to answer and kept repeating the equivalent of “short-term loss, long term gain.” Be patient. The Dow is going higher to 5000. Moreover, those factory jobs are coming back. We will take bicycles back from Taiwan. The interviewer failed to ask about the cost of the tariffed metals but did point out manufacturing would have to be by robot, denying Navarro’s “rise in real wages.” The average wage in Taiwan is about $13,420 (if we did that right).

It goes without saying that only the deluded and mesmerized think Trump knows what he is doing. It’s all impulsive, resulting in slipshod and haphazard outcome unrelated to the real world economy. Analyst Zakaria writes “Trump’s tariff crusade ignores U.S. economic strength — and risks squandering it on fantasy and folly.”

Stock markets crashing around the world do not reflect a financial crisis. It’s not a financial crisis, yet. But the crisis of confidence in the US government can easily be projected to turn into a global economic crisis that then does justify a financial crisis. The stock markets are just running ahead of the facts. Earning season starts this week and expectations are for one grim report after another on future earnings.

Trump says the US has been losing to those taking advantage and cheating. But the US has not been losing—as in the Covid recovery the fasted and most complete in the world. “But Trump is using American power in such a capricious, destructive and dumb way that it will almost certainly result in a lose-lose outcome for everyone.”

Zakaria says “In fact, the poorest American state, Mississippi, has a higher per capita GDP than Britain, France or Japan.” Well, technically but I’d rather live in any of those places than in Mississippi.

Further, “… while America is the world’s dominant power, it is not so strong that it can act this irrationally. The world economy has grown to a size and scale that it will find ways around American protectionism, which is now among the world’s most egregious. Contrary to Trump’s stubborn beliefs, the United States was in fact already somewhat protectionist, with tariff and nontariff trade barriers greater than in 68 other countries. With these new tariffs, American protectionism is off the charts, with higher rates than the Smoot-Hawley ones of 1930 that exacerbated the Great Depression. In the short run, everyone will suffer. But in the medium to long run, countries will start trading around the United States.”

As scathing commentary goes, this is among the best-written. One idea already out there: China links up with Europe.

Food for Thought: What comes next? It all depends on whether this is going to end up as an unforced error/self-destruction or the feedback loop is crooked enough to sling outcomes in a different direction than what we foresee now. In other words, it will take folks outside the White House, from inside the US or outside, to shift the narrative. This is different from what Trump thinks he wants, subservient vassals bowing to the king.

-

Congress takes away Trump’s “emergency” power he is using for tariffs. There was no emergency. Congress has the sole power to tax. It can take it back. This is underway, but faces the craven Republicans in the House. Probability: 10%.

-

The Supreme Court rules on various issues, potentially including tariffs. This takes a long time and of course the court is biassed in Trump’s favor in the first place. On the other hand, there is the Constitution, and some of the Artivles are not actually open for debate. Probability: 10%.

-

Several countries band together, like the EU+UK+Switzerland+the rest of non-EU Europe and goes for bribery. We know Trump is for sale. Another is extreme flattery. We know Trump is vain beyond belief.

-

The single party that can wreak the most severe damage is Canada. Electricity, oil, gas, metals, lumber, etc. Tax every Canadian to subsidize a halt to all critical exports. Get Mexico to join. The pain to American businesses consumers would be huge. 5.

-

Businesses and Wall Street gang up on Trump and make a group visit to him, as the Republicans did in convincing Nixon to resign. At the same time, they tell Congressional Republicans they will withhold primary money to ensure they lose the next election.

-

Protests in the US grow and grow and grow. Trump’s approval rating drops to nearly nothing. This is how the Baby Boomers got the Civil Rights Act passed in the 1960’s. Of course, the president then (Johnson) actually read newspapers.

The desired outcome is a steep reduction in the numbers from the likes of 34% to less than 5%. If and when Trump is forced to cut back, he will declare victory over those folks ripping off the US—they have now learned their lesson, yada yada. This could happen in 3, 6, 9, 12 months. We suspect 6 months is more likely than 12, but you never know with this guy.

Forecast

Extreme moves beg for corrections, whether justified or not on the facts. When everything is oversold, buy-the--dip speculators come out of the woodwork. It’s conceivable that this week will see a recovery in equities and the dollar. The Treasuries, maybe not so much.

The recession and persistent inflation stories remain the sentiment drivers. This likely mean we may see another failed attempt to force a dollar rally, something we have seen a number of times since Trump took office. They were all short-lived but mess up chart-reading something fierce.

For anything long-lasting, we need to see some progress on getting tariff rates down or some other sign of pressure relenting. But there is a problem. If money flows to commodities, that favors the dollar. If money is flowing out of European equities, that’s euro-negative. The best trade now, according to one top analyst, is USD/JPY. As for our canary in the coal mine, the AUD, we are puzzled as to why it crashed so much harder than anything else. This leads us to wonder if we are not in for another dollar rally-ette that is unjustified on any grounds.

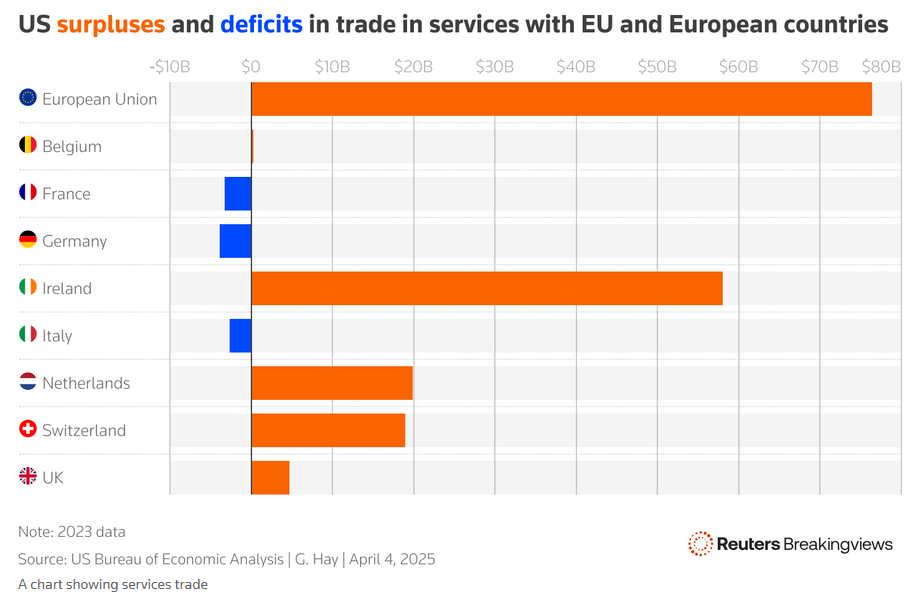

Tidbit: Project Syndicate has a killer article by economist Ricardo Hausmann pointing out that looking at the current account instead of just trade, the US in not far off balance. Trade is a $1.2 trillion deficit but consider the capital surplus of nearly $1 trillion when services, including overseas earnings of US companies.

“If we multiply American companies’ foreign earnings by 26 – the average price-to-earnings ratio of S&P 500 firms – the value of US investments abroad can be estimated at $16.4 trillion. By contrast, foreign companies operating in the US earned just $347 billion in 2024. In effect, America’s surplus in services and foreign equity income nearly offsets its trade deficit in goods. That makes its $16.4 trillion in foreign assets a far more attractive target for retaliation than tariffs on US exports.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat