Key points

-

USD’s August blues: The US dollar faced its worst month of the year in August, sparking concerns about a potential long-term decline. This came on the back of expectations of Fed rate cuts.

-

Dollar smile theory: The USD is currently at the middle part of the dollar smile curve, vulnerable to selling pressure as soft landing hopes rise.

-

Speculator shift: Speculator positioning turned net short on the dollar for the first time since January, raising red flags about further weakness.

-

Rate cut expectations are skewed dovish: The market is pricing in 100bps of Fed rate cuts this year. Only sever economic concerns could transpire that, but that could be USD-supportive amid safe-haven flows. If US economic momentum remains resilient, market expectations may need to shift hawkishly, again pushing the USD higher.

-

Risks to watch: Potential USD crisis triggers in the short-term include pronounced US disinflation, carry trade unwinding or speculative short positioning getting extended. Threats from rising US debt and de-dollarization trends are more long-term concerns.

-

Nuanced outlook: Despite short-term pressures, the USD could rebound if risk aversion increases or if other currencies, like the EUR, face heightened political or economic risks.

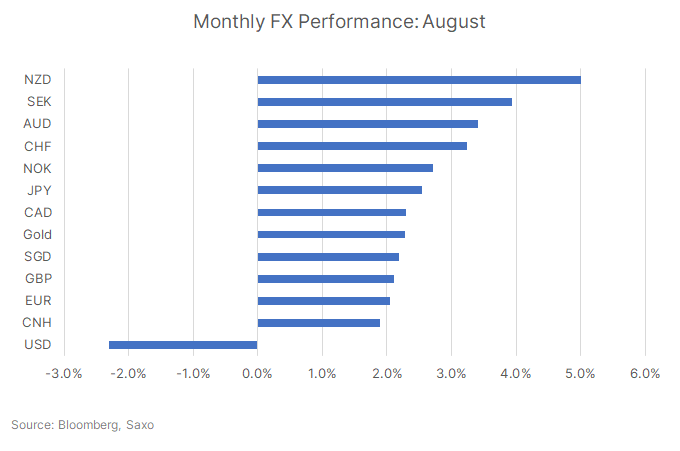

The US dollar has recently faced mounting pressures, raising concerns about whether this signals the beginning of a more sustained period of weakness. August was the dollar's worst month of the year as the July US jobs report and Fed Chair Powell’s comments at Jackson Hole signaled there could be a larger rate cut of 50 basis points coming at the Fed’s September meeting.

The US Dollar spot index (DXY) was down 2.3% in August, registering its second-worst month since the start of 2023 and slipping to over one-year lows.

This came along with US economic data remaining mostly resilient, and soft landing hopes continuing to gain traction. This lands the US dollar in the middle of the ‘dollar smile’ theory, which makes the USD prone to drawdowns as investors go on a hunt for higher yields elsewhere.

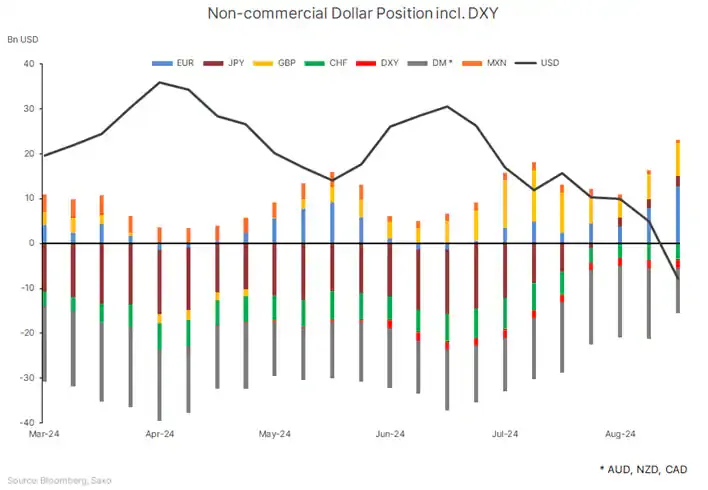

The speculator positioning in the US dollar, as a result, has shifted to a net short in the week of August 27 for the first time since January. These developments have led to increased scrutiny of the factors driving the dollar's current trajectory and the risks that could further undermine its position.

Some are looking at the start of Fed rate cuts to put further pressure on the USD, but there could be reasons to expect the trend to reverse, as noted below.

Why the USD weakness may have limited legs

Market expectations for the Fed are tilting dovish

The market has already priced in 100 basis points of rate cuts by the Federal Reserve for this year, reflecting expectations of a slowing US economy. However, this assumption could be overly pessimistic. If economic data remains even modestly resilient, the market may need to reassess its expectations and shift towards a more hawkish outlook for the Fed. Such a shift would be USD-positive, as higher interest rates would make US assets more attractive to investors, bolstering demand for the dollar.

Recession risks and safe haven demand

If growth concerns materialize and recession risks escalate to justify market’s expectations for aggressive easing from the Fed, then focus will likely shift back to the dollar's role as a safe haven. In times of economic uncertainty, global investors typically flock to the US dollar, driving up its value. This potential flight to safety could counterbalance any initial pressure from rate cuts, limiting the downside for the dollar.

US exceptionalism is intact even if growth slows

Despite a slowing US economy, its resilience relative to other major economies remains intact. US exceptionalism, characterized by strong corporate earnings, a robust labor market, and the dominance of the US dollar in global trade, continues to make the dollar an attractive asset. This could counterbalance recent weakness.

Political and economic risks in the Eurozone are becoming more prominent, compounded by a significant economic slowdown in China. The Eurozone's struggles with stagnant growth, inflationary pressures, and high energy costs, along with China's reduced demand for European exports, could add to the euro's weakness. Political instability in key EU nations and potential fragmentation risks further weaken the euro, making the USD more attractive to global investors.

Geopolitical risks remain elevated

Geopolitical uncertainties continue to create a risk-off environment that traditionally supports the USD as a safe haven. Ongoing conflicts, trade tensions, and potential economic slowdowns in key regions could lead to increased demand for the dollar amidst global risk aversion.

US election risks

The US election cycle is heating up, and the race still looks tight between Vice President Harris and former President Trump. This introduces a layer of uncertainty that could lead to increased market volatility. Historically, the USD has seen renewed demand during such periods of political turmoil as investors seek safety.

Risks to the USD outlook

While there are support factors for the US dollar, several risks could exacerbate its current weakness, potentially leading to a more sustained downturn. We highlight key short-term and long-term catalysts that could signal a looming USD crisis.

Short-term catalysts

Pronounced disinflation in the US: If the disinflation trend in the US outpaces that of the Eurozone and other major economies, it could prompt a more aggressive easing by the Federal Reserve, further pressuring the dollar.

Yield compression and carry trade unwind: A significant compression in US yields could trigger a rapid unwinding of carry trades, where investors had borrowed in low-yielding currencies to invest in US assets. This unwinding could lead to a sharp selloff in the US dollar.

Speculative positioning turning net short: The shift in speculator positioning to a net short on the US dollar is a concerning sign. If speculative bets against the dollar continue to grow, it may indicate a broader market belief that the dollar's weakness is not just temporary but part of a more sustained trend. This could increase the risk of a USD crisis, as a self-fulfilling prophecy might unfold, where the dollar declines rapidly as traders pile on short positions.

Long-term catalysts

Surge in US debt levels and fiscal deficit: Unsustainable debt levels and growing fiscal deficits could erode confidence in the dollar's value over time, particularly if investors begin to question the US government's ability to manage its finances.

Loss of confidence in the Federal Reserve: If the Federal Reserve is perceived as mismanaging inflation or failing to maintain economic stability, it could trigger a loss of confidence among investors, leading to a significant weakening of the dollar. Any risks to the Fed’s independence could also trigger outflows from the USD.

Decline in global demand for US treasuries: A reduction in global demand for US Treasuries as Japanese interest rates rise could lead to higher borrowing costs for the US government and put downward pressure on the dollar. This could also reflect broader concerns about the US economy's health and its ability to service its debt.

Shift away from the USD as the global reserve currency: A move by global central banks and major economies to reduce their reliance on the US dollar as the global reserve currency could weaken its global standing. This shift could be driven by geopolitical tensions, economic diversification efforts, or the emergence of viable alternatives.

Emergence of a viable alternative to the USD: The rise of a credible alternative to the USD in global trade and finance could reduce the dollar's dominance. Whether through digital currencies, regional trade blocs adopting other currencies, or increased use of the euro or yuan, this shift would diminish the USD's global influence.

Conclusion: A more nuanced approach to the USD outlook

While the US dollar is currently facing challenges, a full-blown crisis remains a low-probability event unless these warning signs start to materialize. Investors should stay vigilant and be prepared to adjust their strategies if the landscape begins to shift dramatically.

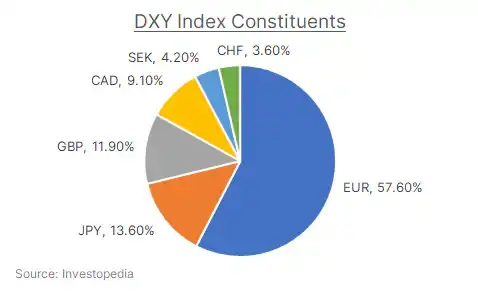

Considering the current environment, it’s important to take a nuanced perspective on the USD’s path. Potential Fed rate cuts or recession risks may strengthen the Japanese yen (JPY) and Swiss franc (CHF), but the Canadian dollar (CAD) and euro (EUR) face higher risks, potentially offering underlying support for the USD. This is especially relevant given the euro's significant weight of over 50% in the DXY index. Investors should carefully monitor these dynamics as they navigate the complexities of the currency market.

Read the original analysis: USD at crossroads: End of strength or start of a crisis?

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Recommended Content

Editors’ Picks

Gold corrects from record high set at $3,500

Gold price pulls away from the record peak it set at $3,500 earlier in the day as buyers take a breather amid overbought conditions on short-term charts. Any meaningful corrective downfall, however, still seems elusive as US Dollar downtrend remains intact.

EUR/USD drops to daily lows near 1.1470, Dollar regains balance

EUR/USD slips back below the 1.1500 mark, trimming part of Monday’s rally as the Greenback picks up some upside momentum following recent multi-year losses. In the meantime, markets remain cautious in light of President Trump’s criticism of Fed Chair Jerome Powell and its potential implications for the US markets.

GBP/USD stays below 1.3400 as USD selloff pauses

GBP/USD fluctuates in a tight range below 1.3400 on Tuesday as the modest recovery seen in the US Dollar caps the pair's upside. Nevertheless, the pair's further downside appears limited as fears of a US economic slowdown and concerns about the Fed's independence remain a headwind for the Greenback.

3% of Bitcoin supply in control of firms with BTC on balance sheets: The good, bad and ugly

Bitcoin disappointed traders with lackluster performance in 2025, hitting the $100,000 milestone and consolidating under the milestone thereafter. Bitcoin rallied past $88,000 early on Monday, the dominant token eyes the $90,000 level.

Five fundamentals for the week: Traders confront the trade war, important surveys, key Fed speech Premium

Will the US strike a trade deal with Japan? That would be positive progress. However, recent developments are not that positive, and there's only one certainty: headlines will dominate markets. Fresh US economic data is also of interest.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.