US interest rates and the dollar: Still the closest of companions

After all the pandemic dramas of the past 18 months, Federal Reserve interest rate policy remains the most important indicative for the US dollar. Are the Fed's June projection of two possible hikes in 2023 a tightening bias? If US inflation is a temporary phenomenon, why the abrupt change in policy? Whither the labor market? Join FXStreet senior analysts Yohay Elam and Joseph Trevisani for a examination of the US economy as the markets prepare for the all-important Nonfarm Payrolls on Friday.

Joseph Trevisani: The dollar was fueled by rising US Treasury rates in the first quarter. The 10-year yield jumped about 80 points to 1.746% by March 31. Currently the 10-year is at 1.461%. However, since the June 16 FOMC the 2-year has jumped.

Yohay Elam: Indeed, the greenback is at the highest since April against both the euro and the pound. Other currencies have also succumbed to King Dollar.

Joseph Trevisani: From 0.15% to 0.25%, so you could say it is still US rates that are powering the dollar.

Yohay Elam: The Federal Reserve's hawkish shift seems to be the main driver of this dollar strength. I am just surprised that it is "the gift that keeps on giving"

Joseph Trevisani: I agree, though the actual rate performance, in historical terms, is minor. Perhaps it is that old saying... "It's not that it is done well, but that it is done at all," Samuel Johnson, a paraphrase. Behind the Fed is the economic comparison. The US leads, and is imagined to lead in recovery.

Yohay Elam: The US economic recovery is undoubtedly robust, that is what led the Fed to change tack, albeit perhaps a bit too soon.

Joseph Trevisani: Yes but with odd patches in the labor market.

Yohay Elam: Indeed, the return to normal is like clicking Ctrl+Z

Joseph Trevisani: Yes but so far it is all talk from the Fed.

Yohay Elam: What surprised me most is Fed Chair Jerome Powell's comments on future job growth. Abandoning the outcome-based approach in favor of an outlook-based one. Too soon.

Joseph Trevisani: I think the Fed is worried about inflation far more than they let on.

Yohay Elam: The Fed upgraded its inflation forecasts substantially and signaled two hikes in 2023, a big shift.

Joseph Trevisani: Fed prognostication on inflation is poor, always has been.

Yohay Elam: That hike hint is the single strongest dollar driver in my opinion. And I think they were too quick to cast doubts about the theory of transitory inflation.

Joseph Trevisani: Remember, for a decade after the financial crisis, the FOMC, Bernanke and Yellen were forever predicting inflation...

Yohay Elam: Which never materialized.

Joseph Trevisani: I agree on the rate change, it speaks of inflation.

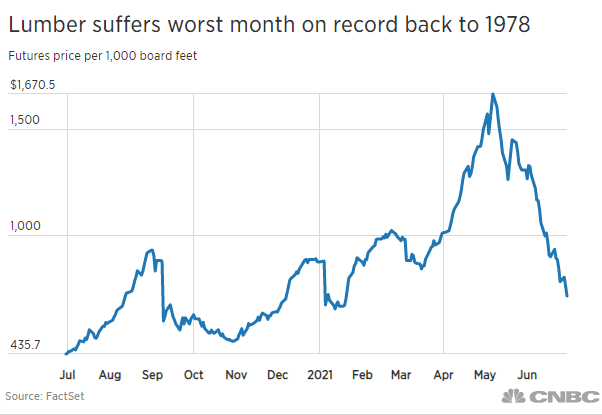

Yohay Elam: I think they were too quick to show wariness about inflation in June. Their previous transitory theory seems more credible as time passes. Look at lumber:

Joseph Trevisani: Another clue was yesterday's odd reaction to the ADP report. I just happen to have written about it.

Yohay Elam: 40% down in June, the worst month since 1978. So far, no 1970s inflation, but more of a downfall like in the 70s, at least for this commodity.

Joseph Trevisani: ADP was stronger than expected..and Treasury yields fell.

Yohay Elam: Yields are also extremely calm. ADP used to be arguably somewhat reliable before the pandemic. Not anymore.

Joseph Trevisani: Yes, but lumber was up over 100% I believe, so the overall is still higher. Yes I agree, its not the NFP prediction that interested me, but the initial credit reaction. The labor shortage is forcing employers to offer bonuses and wage increases. Hence wage inflation. Stronger hiring will help to mitigate that.

Yohay Elam: Lumber is at levels seen in January, December 2020 and August 2020, back to the range, far off the highs. The shift in power to workers is amazing. Still too early to say if it is temporary or not.

Joseph Trevisani: Futures prices are indicators, important but not complete. Retail prices rarely fall back to prior levels, no matter what futures do. So I think we probably have a higher base in many commodities, higher inflation expectation perhaps. And the same is probably true of wages.

Yohay Elam: A higher base perhaps. That would mean a one-off bump higher, without persistent rises.

Joseph Trevisani: Unless, expectations have changed, in wages particularly. Nothing else explains the Fed shift.

Yohay Elam: When you hit the accelerator too strong, the wheels spin a bit, but then you get back into lane, that is how I see it so far – quick reopening causing bottlenecks, temporary price rises, skill mismatches, and then things sort themselves out. If wage expectations change, it would be a whole different ballgame. It would mean that 2021 is the year the Great Recession fully ends.

Joseph Trevisani: Yes and that is what I think prompted the Fed.

Yohay Elam: Rising prices, more power to workers. Indeed, despite disappointing Nonfarm Payrolls figures in May and April, monthly wage gains exceeded expectations.

Joseph Trevisani: Exactly. The Fed has been preparing for this price surge since last October with inflation averaging. Suddenly, their rate projections jump? I don't think anyone expected the relatively slow hiring given the number of open positions in the JOLTS survey and the numbers of unemployed workers.

Yohay Elam: I think the Fed´s goal was to prevent a taper tantrum.

Joseph Trevisani: One final point on Fed. As you observed, so far it is all talk from the Fed, and against possibly changing inflation, talk is useful weapon. Successfully I think.

Yohay Elam: They act rapidly in crisis, during the rest of the time, talking is their weapon.

Joseph Trevisani: Normally the anticipation of a policy change front-loads the credit market and rates, the Fed has largely prevented that very usual adjustment. Some of the other traditional indicators of inflation are absent, specifically gold was down 7% in June.

Yohay Elam: Yes, gold lost its correlation with yields.

Joseph Trevisani: Perhaps the crypto market is draining that interest?

Yohay Elam: Crypto has beaten gold in interest, but cryptos have also crashed from the highs.

Joseph Trevisani: Perhaps as an inflation hedge also?

Yohay Elam: I think these are nice theories, but the fall of cryptos and gold, while US inflation is rising somewhat, makes the inflation hedge theory weaker.

Joseph Trevisani: I am not really proposing it an inflation reaction in cryptos. It is difficult if not impossible to trace external effects in cryptos except for comments from Elon Musk and notices of commercial acceptance. Either gold has lost it traditional inflation reaction, or there is no inflation. Since the second is obviously not true, the first must be.

Yohay Elam: There is hardly any commercial acceptance of cryptos, unless you count ransomware of course.

Joseph Trevisani: Indeed.

Yohay Elam: Regarding the dollar, can its relative strength also be attributed to weakness of other currencies?

Joseph Trevisani: Partially yes. It is a reflection of the better economic and pandemic positions of the US. The ECB seems far more reluctant to consider policy changes than the Fed. That is a continuation of the ECBs inability to return to a 'normal' rate policy. It was the same in the decade after the financial crisis. Europe, at least on rate policy, is becoming Japan. Zero rates are normal rate policy.

Yohay Elam: The eurozone's Japanification process is accelerating... What surprised me more is USD strength against commodity currencies, where central banks moved toward tightening before the Fed.

Joseph Trevisani: Except the Canadian dollar.

Yohay Elam: Where tapering is underway.

Joseph Trevisani: Employment PMI for manufacturing fell to 49.9 in June. That is not going to quell labor market concerns.

Yohay Elam: It is lowering expectations ahead of the NFP, setting a lower bar for an upside surprise.

Joseph Trevisani: And initial claims are at a pandemic low.

Yohay Elam: And we do not have the ISM Services PMI. A lot of uncertainty. Do you have an NFP guess?

Joseph Trevisani: 550,000. Manufacturing is having trouble finding skilled workers, services workers in general... both would seem to be promoting wage inflation.

Yohay Elam: However, the question remains open – is it transitory or not? Bottlenecks or a long-term imbalance? I opt for transitory. My NFP guess is 600,000.

Joseph Trevisani: I think we have both temporary and permanent effects. The Fed will get its long term 2% goal and then some.

Yohay Elam: Will such inflation be exported?

Joseph Trevisani: Good question. Any commodity based inflation should be global. The conditions of the US labor market may be unique to the US.

Yohay Elam: I am optimistic about the US economy, I think things will get sorted out and US demand will lift the global economy. Eventually negative for the dollar, but not in the next months, which will be highly uncertain.

Joseph Trevisani: Historically that scenario would propel the dollar higher but markets have been restrained. The difference is probably the Fed.

Yohay Elam: The Fed is always the difference. Powerful Powell.

Joseph Trevisani: Jerome the Judicious.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

FXStreet Team

FXStreet