Trump wins: Tax cuts come with a cost

Donald Trump’s victory will ensure a lower tax environment that should boost sentiment and spending in the near term. However, promised tariffs, immigration controls and higher borrowing costs will increasingly become headwinds through his presidential term.

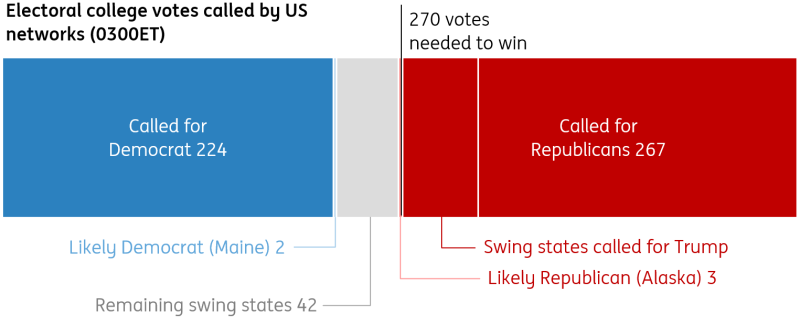

US Presidential election results

(as of 0300 ET)

Source: New York Times

Tax cuts, immigration controls and protectionism

The people have spoken and Donald Trump will be the 47th President of the United States. He will also become only the second president, after Grover Cleveland, to serve non-consecutive terms.

While opinion polls had suggested a close-run race, financial markets appeared increasingly confident of such an outcome with equity markets, the dollar and Treasury yields all rising in recent weeks. Whether these trends remain in place depends on how quickly Trump can marshal his party and pass his legislative agenda through Congress.

The first issue to deal with is addressing the Federal debt limit, which will be reinstated on 2 January. Current Treasury Secretary Janet Yellen will immediately deploy "extraordinary measures" and use cash on hand to continue paying the government’s fiscal obligations. Trump will then be inaugurated on 20 January and his team will have to quickly spring into action to agree a deal on the budget and get the ceiling lifted or suspended further.

At the moment it appears the Republicans are on course for a clean sweep with the presidency, Senate and House, which would mean this should be straightforward. However, if the Democrats manage to win the House this could be a contentious period that will eat up time and cause market angst. Under this second scenario, it would give an early signal of whether his ability to pass tax cuts is going to be constrained.

As for policy, his three main policy aims are to:

-

Extend and modify the Tax Cuts & Jobs Act which is currently scheduled to expire at the end of 2025, accompanied by lower corporate taxes and exempting tips from taxation.

-

Restrict immigration, particularly from the Southern Border and,

-

Implement tariffs that he believes will raise revenue, promote re-shoring of production and boost economic growth and jobs.

Domestic America first

In terms of timing, he is likely to repeat his playbook of 2017 and focus on the domestic issues first. We strongly suspect the initial emphasis will be on immigration policy. The proposals involve a crackdown on illegal immigration, mass deportations of illegal migrants already in the US, and some restrictions on legal migration into the US.

He is also likely to set in motion his plans for reshaping government early on. He believes there is significant waste, abuse and fraud that needs to be tackled and he will be seeking to reduce regulation tied to energy and environmental policy.

The second phase will be on taxation. If it is indeed a Republican clean-sweep, this should be relatively straightforward to achieve and should be completed with plenty of time to spare before his 2017 tax cuts expire on 31 December 2025. However, if Congress is split, this will take longer. Moreover, there is the potential for some dilution as House Democrats push back and the aspiration of extending tax cuts as intended may be curtailed, particularly for the corporate sector, as a compromise to get a deal done before the deadline.

Once he has made progress on the domestic agenda he is likely to switch toward trade policy and the prospect of 60% tariffs on Chinese imports and 10-20% tariffs on products from elsewhere in the world. We suspect that the earliest time for this to occur will be the third quarter of 2025, with a more likely time frame of the fourth quarter of 2025/first quarter of 2026. We also believe there will be a phased introduction given the potential for significant economic disruption. China would likely be impacted first, with a gradual series of tariffs introduced on different products from other countries coming in later.

Regarding geopolitics and international relations, Trump’s foreign policy priorities, aside from containing China, remain relatively unclear due to his election focus on domestic issues. His approach to international diplomacy is expected to be largely transactional and occasionally isolationist, showing less deference to existing partnerships. This may strain relations at times, with trade and diplomatic tensions framing his foreign policy plans. Additionally, criticism of NATO members’ inadequate defence spending is likely to be a recurring theme in discussions on broader security issues.

Initially, Trump is expected to concentrate on issues he highlighted during the election trail and rallies, such as resolving conflicts in Ukraine and the Middle East. Having brokered the Abraham Accords in 2020, he is likely to renew efforts to normalise relations between Israel and neighbouring Arab states, potentially making this a cornerstone of his Middle East agenda. However, his approach to Ukraine is expected to be more decisive, possibly withdrawing military aid to force a negotiated settlement that may allow Russia to retain its current territorial gains. It remains unclear if the lifting of sanctions against Russia would also feature.

The economic consequences

In the near term, the prospect of lower taxes and a pro-business environment should keep sentiment relatively firm and risk appetite buoyant. We have long argued that high-income households have been the key driver of consumer spending growth given inflation has been less of a constraint relative to low-income households, rising asset prices have boosted wealth and high interest rates have benefited them as they have been receiving 5%+ interest on money market funds while paying perhaps 3.5% or less for their mortgage. If these households keep more of their income, that should help support spending.

At the same time, a clean result with a smooth political transition to the new president will provide clarity and help support sentiment, and in a lower interest rate environment, it could improve economic prospects. For example, companies that delayed investment spending on election/regulatory uncertainty may now be prepared to start putting money to work.

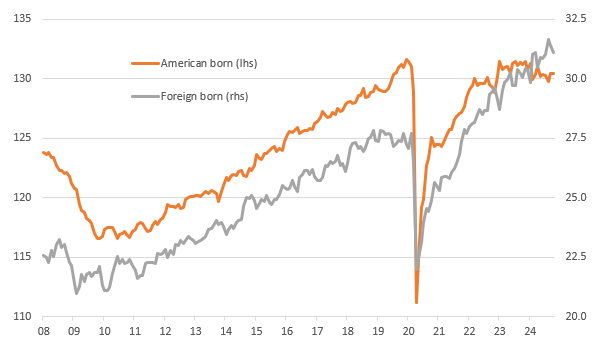

However, the medium and longer-term growth prospects under his presidency are more uncertain. Reduced immigration and forced repatriation could become a major constraint on the US economy, particularly in industries such as agriculture. American-born worker numbers are falling and are a million lower than in 2019. The downtrend in US birthrates suggests little prospect of a demographic-driven turnaround. Employment growth is coming from foreign-born workers, who now make up 19.5% of all US employees. If the foreign-born workforce also shrinks, it could create significant supply-side challenges, driving up wages and inflation. To counteract this, productivity would need to increase substantially. Additionally, fewer active people in the country would mean reduced economic demand.

American-born workers are falling in numbers, foreign-born are rising (millions)

Source: Macrobond, ING

Tariffs are another supply-side constraint on the economy. These are taxes that will be paid by US importers (typically wholesalers and retailers) when the products enter the US. They then decide whether to absorb the extra costs or pass them on either partially or in whole to the customer.

In 2018, the Trump administration introduced a 20% tariff on all imported large residential washing machines. According to the Consumer Price Inflation report, there was no impact for the first four months as retailers ran down their existing inventory that hadn’t been subject to the tariff, before raising consumer prices by 12% over subsequent months. Since the US manufactures washing machines that are not subject to the tariffs, it appears that consumers bore more than 60% of the tariff cost on foreign-made appliances, with the remainder absorbed by retailers’ profit margins or through price reductions by foreign producers. Prices gradually edged lower again, as some buyer substitution for domestically-made washing machines kicked in and presumably as foreign manufacturers agreed to further price cuts.

Under a more sweeping plan of aggressive tariffs, it may be more difficult to immediately substitute domestically-made products, due to capacity constraints. Consequently, the hit to retailers’ profit margins and the erosion of household spending power from higher inflation could be significant in an economy where consumer spending accounts for 70% of all activity. US manufacturers should become more price competitive and benefit, but many also use imported components so face higher costs too and it will take time to build up a US manufacturing plant.

Moreover, retaliation from foreign countries has to be expected, which will create challenges for US exporters and manufacturers. If we see weaker global demand from escalating tit-for-tat trade tariffs, it could mean less investment and fewer jobs, not more as Trump expects.

The biggest headwind to medium-term growth is likely to come from higher US government borrowing costs, which lift consumer and corporate borrowing costs more broadly. The bipartisan Committee for a Responsible Federal Budget estimates that Trump's policy mix of tax cuts, tariff hikes and spending changes will add $7.75tr to the US national debt over the subsequent 10 years relative to the Congressional Budget Office’s current baseline projections.

The US is already running a fiscal deficit of close to 7% of GDP this year with debt-to-GDP running at 100%. Fiscal sustainability concerns, we believe, will lead to investors demanding a higher term premium for lending to the US government over the longer term, pushing up borrowing costs broadly in the economy – note the hefty rises in Treasury yields as markets increasingly priced for a Trump victory. We suspect that the economic implications from reduced population growth, global trade protectionism and the prospect of higher borrowing costs will make it difficult for the US economy to grow rapidly enough to generate tax revenues to fully cover Trump's fiscal plan.

At the same time, the Federal Reserve may take the view that if fiscal policy is going to be loosened relative to their previous baseline forecast then it needs to run monetary policy tighter, implying a higher neutral interest rate to keep inflation at its 2% target. An environment of higher inflation from tariffs could amplify the risk of a higher, steeper yield curve over the next four years relative to what the US economy has experienced over the previous decade.

That said, we have to remember that Jerome Powell’s term as Fed Chair ends in February 2026 and with the Republicans controlling the Senate President Trump has an easy pathway to nominating and installing a candidate that is more willing to accommodate his views on interest rate policy. One example could be a more compliant Fed that is willing to adopt some form of “yield curve control” should higher Treasury yields threaten to undermine the growth story. Nonetheless, such action risks damaging the central bank's credibility, potentially prompting an adverse market reaction.

Of course, what Trump proposes during an election campaign and what he eventually delivers as president may be very different. Our view is that while the growth trajectory in the near term looks fine, the more aggressive he goes on fiscal and immigration policies the more challenges this may present for the US economy over time.

Europe’s worst economic nightmare comes true

A looming new trade war could push the eurozone economy from sluggish growth into a full-blown recession. The already struggling German economy, which heavily relies on trade with the US, would be particularly hard hit by tariffs on European automotives. Additionally, uncertainty about Trump’s stance on Ukraine and NATO could undermine the recently stabilised economic confidence indicators across the eurozone. Even though tariffs might not impact Europe until late 2025, the renewed uncertainty and trade war fears could drive the eurozone economy into recession at the turn of the year.

Despite European politicians’ claims of being prepared for a second Trump presidency, it remains unclear whether Trump could indeed prompt deeper integration, given the domestic challenges many European governments face. Europe will likely wait to see what policies Trump actually implements. Meanwhile, the ECB will need to do the heavy lifting, pushing interest rates into easing territory. With these election results, a 50bp rate cut at the ECB’s December meeting has become more probable, with expectations of the deposit rate dropping to at least 1.75% by early summer, possibly followed by further easing towards the end of 2025.

Fixed income faces upward pressure on yields

When Trump won the presidential election in 2016, it was unexpected. In consequence, there was a dramatic reaction. The 10yr Treasury yield was up some 45bp over the following 10 days and by a further 35bp through the subsequent month. The reaction in Europe was more muted, with the 10yr German yield, for example, up by about 15bp as a one-week reaction, but then it faded lower thereafter.

The difference this time is a Trump victory was generally anticipated. In that sense, the reaction need not be as dramatic, and more likely to be driven by actual policy prescriptions over subsequent months. That said, we’d still expect a material reaction higher in the 10yr Treasury yield. Still, given the size of the up-move already seen pre-election for the 10yr US yield, the post-election move is likely to be 20-40bp to the upside in total. Expect the 10yr German yield to do about half of this, implying a further rise in the Treasury-Bund spread. This size of move is probable as Trump's win was far from 100% anticipated. The clean sweep had a lower probability attached to it. If confirmed, the oomph trade will present the path of least resistance, at least as an impact-to-multiweek reaction. An additional kicker here is the implementation of a meaningful tariff policy, with inflation implications to boot.

When Trump won in 2016, credit experienced the same dramatic reaction. BBB Credit spreads in USD tightened by an average of 22bp in the remaining weeks of that year with 12bp of that coming in the first 109 days or so. Conversely, EUR BBB credit widened by 12bp in the first 10 days and ended the year 4bp wider than before the election result came in.

However, 2024 is different to 2016 where USD BBB credit has already tightened some 30bp over the past three months and BBB EUR credit has widened by about 12bp on average. Thus, this time round the reaction should be more muted as USD credit is deemed expensive at current levels and one could argue it has priced in at least part if not most of the Trump victory. We expect the USD tightening momentum to prevail in the short term but likely only in single-digit territory of say 8bp. For European credit, valuations are currently less stretched leaving more room for some tightening. However, similar to 2016, EUR credit is expected to be less influenced by international policies, making a 4bp tightening the most positive outcome. Medium to longer term, the inflationary aspects add to the growing list of concerns about credit spread performance for 2025.

Another bout of Dollar strength

FX markets went into this election pricing a high probability of a Republican clean sweep, with the dollar stronger across the board in October. That reversed a little after weekend polls suggested momentum was swinging toward Harris, but today's show of strength from Trump has sent the dollar 1-2% higher across the board. Protectionism is a given and a negative for the currencies of the Rest of the World. But whether it is a clean sweep or a Democratic House will have an impact on risk assets and the relative performance in the currency universe.

This is a negative outcome for EUR/USD, where rate spreads are widening against the euro and a new risk premium will need to be added in for protectionism and potentially geopolitical risk too. 1.05 looks the immediate target over the coming weeks, but a move to parity may need to wait until later in 2025 when the full force of the protectionist blast becomes clear. And failure for the Republicans to win the House would demand an even more negative EUR/USD scenario, where world growth would not be able to enjoy as much support given the potential scaling back of prospective Trump tax cuts.

The prospect of relatively higher US interest rates and weaker world trade growth under a Trump administration is a bearish one for emerging market currencies. This is already curtailing some EM easing cycles, e.g. in Hungary, and has indeed reversed the one in Brazil. With US protectionism potentially going global and EUR/USD under pressure, CEE currencies look vulnerable. Much focus will of course be on the Chinese renminbi, but we suspect local authorities may try to limit USD/CNY gains to the 7.30 region as they seek to cement the renminbi's growing clout in global financial architecture.

Read the original analysis: Trump wins: Tax cuts come with a cost

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.