Trilateralism: The past is prologue

Intercapitalist rivalries ebb and flow and shaped modern history more than many may realize. Recall that Nixon unilaterally severed the dollar's last ties to gold, not because of the Soviet Union. America's capitalist allies in Europe demanded gold for their dollars, accumulating from aid, foreign direct investment, and trade.

A couple years after the collapse of Bretton Woods, the Trilateral Commission was formed to ensure greater dialogue among the three large capitalist camps: North America, Europe, and Japan. David Rockefeller founded the group, and among the founding members were Paul Volcker and Alan Greenspan. Although current officials cannot be members, over the years, numerous prestigious former officials have been members, and in fact, former ECB President Trichet serves as the European Chair.

Many have suggested a US-China Cold War may be the organizing principle when thinking through recent developments and their trajectory. We, too, have found it to be a useful construct framing recent developments. It is fine at a high level, but we suspect a more detailed view may give new meaning to Trilaterlism. Rather than a two-player game, it is complicated by a third participant: Europe. It might not nicely fit into the intercapitalist rivalries even though some academics, like Branko Milanovic, argue that China is a capitalist country essentially because workers are paid wages, and all that implies.

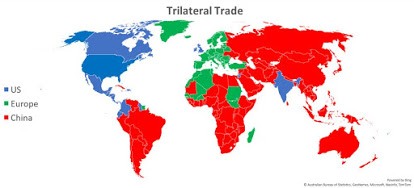

Trade patterns offer a quick but not necessarily the best way to get an idea of what could be our trilateral future. Often, a two-color map is shown to illustrate whether the US or China is the larger trading partner. Nicholas Hatzis, a graduate student in a seminar I led at the Gabelli School of Business at Fordham, created this map that shows where Europe is a bigger trading partner than the US or China.

Admittedly, trade can be a purely commercial transaction and not indicative of political alliances. China is Japan and Australia's largest trading partner, for example. A variety of Australian imports, from iron ore to wine, are being blocked because of Canberra's criticism of Beijing's policies. China's export ban on rare earth shipments to Japan a decade ago was a wake-up call. Alternative sources and processing have been developed, and inventories (e.g., Pentagon) have weakened China's near-monopoly control and takes some of the sting from Beijing's recent threats.

Some countries' reliance on China's demand may, over time, create interests that want to change the foreign policy away from a pro-American stance. It need not be pro-China for it to be to Beijing's advantage. Neutrality is good enough. The US has opposed the Nord Stream 2 pipeline that boosts Russian natural gas exports directly to Germany for nearly a decade. The same logic applies equally to Japanese and Australian reliance on China's demand. One big difference is that while the US would like to provide more natural gas to Europe, it has no need for Australia's coal or iron ore.

Another strategic contradiction posed by China's dominant trade position reflects a dilution of the US presence but not its high-level military commitment. The Biden administration has quickly reaffirmed that the US umbrella covers some islands, atolls, reefs, and the like that China claims. Still, the decline of presence would suggest a decline in interests over time, and in the long-run, interests and commitment must converge.

When the Trilateral Commission was founded, Japan was the dominant Asian economy. That is no longer true, even though Japan is the world's third-largest economy. Since a few years after Trilateral Commission was founded, China has been committed to rapid industrialization and modernization. Many narratives see the first phase as a gradual liberalization, even though it included the Tiananmen Square Massacre (1989).

Since Xi became the head of the Chinese Communist Party in 2012, especially since his term limits were abolished (2018), a less liberal modernization effort has been undeniable. If anything, the state-sector has become more powerful and dominating. While China's economy is a centripetal force in Asia, with the Middle Kingdom at the center, its actions domestically and on the international stage are a centrifugal force, alienating potential allies. Indeed, Beijing is perceived as a bully, which gives cause to others to embrace the US, even if reluctantly, as a counterweight in the region.

The US presence and its ability to project its military might complicate China's sphere, but it is not clear that Beijing has become the regional hegemon. North Korea, India, Pakistan are nuclear powers. Iran may still become one. Aside from China, there are four other top 10 militaries in the world nearby; Japan, India, Pakistan, and South Korea (Global Firepower Index 2021). Many military strategists wonder if China's People's Liberation Army could take Taiwan that former Australian Prime Minister Kenneth Rudd characterized, as an island of the Netherlands' size and Norway's terrain.

Yet, China's sheer size gives it a gravitational pull that Japan lacked. It, and not the US, leads the largest free-trade agreement (Regional Comprehensive Economic Partnership) that includes Japan and South Korea for the first time and Australia and New Zealand. It might not be as bold or have as high of standards that the US would have insisted on, but tariffs on more than 90% of the goods will be eliminated, and there are basic rules on investment and intellectual property.

Moves toward economic and monetary union are the culmination of the evolution of the European bloc from the currency "snake" in the 1970s and the European Exchange Rate Mechanism. Three big crises have fueled the evolution. The unification of German unleashed destabilizing forces, ending the ERM and gave rise to the Maastricht Treaty and a common currency. The Great Financial Crisis and the sovereign debt crisis in Europe expanded the ECB and the European Union's institutional capacity. The pandemic has seen the EU launch common bonds to fund regional unemployment insurance and a recovery effort. Although some quarters hailed this as a "Hamiltonian moment," the fight over whether it will be a permanent institutional addition or simply a crisis response is still to be had.

Nevertheless, Europe seems galvanized. It has struck a free-trade agreement with Japan (which is still proving elusive for the US, who nevertheless wants to be granted the same terms as the EU). At the very end of last year, it secured a trade agreement with the UK, which has left the EU, and a pact with China.

Europe's economic performance lags behind the US and China. It does not appear to have much of a foothold on the commanding heights of the new economy. However, it seeks to have a substantial voice on the rules governing data privacy, the environment, and the internet giants' behavior. Yet, its ability to enforce its will looks terribly compromised after years of underfunding defense. Germany may send a frigate to make port calls in Japan, South Korea, and Australia. It is expected to enter disputed waters in the South China Sea, but if it is attacked, there seems to be little doubt about who would defend it.

The Nord Stream 2 pipeline does not make Europe more secure but instead leaves it vulnerable to Russia's goodwill. The EU sanctions Russia for its behavior but not in a way that rises above inconvenience and annoyance. Similarly, the EU sanctions China for actions in Hong Kong and its treatment of the Uighurs. However, Europe appears more willing to sustain a type of political cognitive dissonance: dislike of Russia and China's behavior but does not want to pass up commercial opportunities. Moreover, as the chart above illustrates, China has taken stakes in numerous ports in Europe. Eastern and Central Europe disputes with Brussels are not only over the independence of the judiciary and a free press, but countries that lived under the Soviet boot want a more robust confrontation.

Even before the Trilateral Commission was launched, Germany pursued "OstPolitik," an early form of detente with the Soviet Union. A treaty was struck in which the Soviet Union renounced the use of force, and Poland accepted the Oder-Neisse line and the territorial settlement of WWII. Europe shows a preference for striking such modus vivendi, like China's investment agreement, that shifts the focus to adjudication of conflicts.

The European Commission issued a document seeking to boost the international role of the euro. The US sanctions on companies involved Nord Stream 2 pipeline and violations of Iran sanctions frustrate Europe and demonstrate its limited sovereignty. The common EU bond is nowhere large enough to compete with the US Treasury market for large pools of capital, including central banks and sovereign wealth funds. The euro's share of global reserves is broadly stable, a little more than 20% of the allocated reserves. The US can deny access to the dollar funding market, and Brussels has not devised a robust workaround.

Europe, Japan, and many others seem to simultaneously worry about too weak and too strong America. They chafe as the US imposes its will through its unique power levers. At the same time, they worry about too weak of America who may return to Fortress America and withdraw from the multilateral world it was instrumental in creating.

Biden's election may represent the restoration of the US political elite's more multilateral wing, but there is no going back to 2016. Many international observers recognize the same thing as many domestic political analysts do, namely that Trump may have lost the presidency, but he remains the single most powerful Republican. The party that occupies the White House typically loses seats in the midterm election (2022). Given the near parity presentation in both the House and Senate, it is not inconceivable that the Republicans gain control of one or both houses. Nor has it been lost on foreign observers that the US Senate has been singularly unable to approve a multilateral treaty for 15 years. The US President has been forced to rely on the legally weak executive orders that, as we have seen in 2017 and 2021, can be unwound quickly by the next one.

There seems to have always been an eddy in the stream of ideas that see America in decline. It has probably supported more than a cottage industry since the first speculation against the Continental army's loans and bonds in 1776 as it waged war against one of the most powerful empires of the day. With China's rise and its sheer scale, the US has a rival of the likes it has not seen before. Making conservative assumptions, even with the monetary and fiscally induced growth spurt this year, the US economy is likely to be overtaken by China at market exchange rates before the end of the decade.

To be sure, it is not merely China. It is two decades of ineffectual foreign policy, perhaps beginning with Iraq's invasion in 2003 that destabilized the Middle East. There is the forever war in Afghanistan, confusing policy in Syria, and the disaster in Libya. The 2018 tariffs that Trump shrouded with national security claims levied on steel, and aluminum imports from Canada, Europe, and Japan have not been lifted yet by the Biden administration. Even during the pandemic the US has not risen to the occasion. It accounts for about 4% of the world's population and an estimated 25% of the document cases, and almost 20% of the deaths.

The arms-control-like agreement that limited government interference in the foreign exchange market to secure trade advantage is in disrepair. The weaponization of access to the dollar erodes trust in international service/utility that the US provided. Of course, the response to 9/11 bolstered efforts to cut off terrorist financing, and in so doing, officials discovered a high-precision weapon with broad application.

The collateral damage may not be so apparent, but it undermines the goodwill toward the dollar brand and encourages the search for an alternative. Hence, Mark Carney, former Governor of the Bank of Canada and the Bank of England, went to America's heartland at the Fed's Jackson Hole gathering in late 2019 and declared that the dollar was a source of instability in the world and ought to be replaced with a multinational digital reserve asset. It seems akin to Keynes' bancor proposal at Bretton Woods. Some argue that a token one gets for solving a difficult computer problem, and consumes as much electricity as a small country, could replace it.

While Merkel and Macron warn against dividing the world into blocs, a crystallization of a new alliance may be emergent even if not equivalent to NATO. The scaffolding has been there for several years, but Beijing's continued harassment of Taiwan and its other aggressive acts in the area may provide a catalyst for the next evolutionary step. The marriage of the 5-Eyes intelligence sharing (US, UK, Australia, New Zealand, and Canada) and the Quadrilateral Security Dialogue (US, Australia, Japan, and India), also known as the Quad. It is not difficult to imagine the group expanding to include South Korea, which is also the 10th largest economy, and the firepower of its military surpasses Germany.

The three spheres, the US, Europe, and China, are simultaneously pursuing import-substitution strategies. The US and Europe found themselves heavily reliant on China for medical supplies, like PPE and medicines. This will change, but the import-substitution efforts will be broader and fall under the elastic rubric of national security. It will include rare earths and semiconductor chips, to cite a couple of examples in the news. Chips are ubiquitous but consider that the dollar value of China's semiconductor imports exceeds the cost of its oil imports, and it is the world's largest importer of oil. According to the Congressional Research Service, an F-35 fighter jet has more than 900 pounds of rare earths. A submarine may need four tons.

It makes little sense for China to be beholden to the US duopoly of mobile operating systems. Yet the fragmentation of the internet and the strategic threat that former US Trade Representative Barshefsky referred to in last August's op-ed piece in the Financial Times was not China but Europe. Europe's effort to secure "digital sovereignty" was an affront to US interests and she called on Europe to abandon its techno-nationalism. On the contrary, it is poised to grow.

The initial Trilateralist vision was to deepen the communications of the three capitalist areas that were seemingly diverging. A little less than half a century later, three blocs appear as a useful way to frame the developments. The two most significant changes have been the greater integration of Europe and China's rise to eclipse Japan as the dominant economy in Asia. The center of the world economy has shifted. It is no longer the Northern Atlantic. Trans-Pacific trade has outstripped trans-Atlantic trade for around 40 years, though we would quickly add that China surpassed the US as Europe's biggest trading partner in 2020. With broad strokes, we have tried to sketch out the emerging trilateral world, attentive to tensions and contradictory developments. It is not the first or last word.

Author

Marc Chandler

Marc to Market

Experience Marc Chandler's first job out of school was with a newswire and he covered currency futures and Eurodollar and Tbill futures.