Today the top data release is JOLTS

Outlook

One of the top stories today is, sadly, that Fed Gov Waller said he is leaning toward a cut at the Dec meeting. He said "As of today, I am leaning toward continuing the work we have started in returning monetary policy to a more neutral setting. Cutting again will only mean that we aren't pressing on the brake pedal quite as hard."

This is being taken at face value but we think it seems Waller is throwing down his last dovish vote but before now, was not convinced a cut was right. Mr. Powell speaks tomorrow.

The next Fed meeting and the last of the year is a mere 15 days away. The CME FedWatch tool flip-flops but this time, Waller flipped the probability of a cut from 61.6% the day before to about 76% late yesterday and 72.5% so far this morning. Seems a bit flighty. Those expecting the Fed to stand pat fell to 27.5% from 40.6% a week ago.

Today the top data release is JOLTS, once the favorite of now TreasSec Yellen when she ran the San Francisco Fed. Friday brings nonfarm payrolls, usually the big market-mover. But former Fed economist Sahm has a different view, especially given the galloping GDP just released by the Atlanta Fed. It’s productivity.

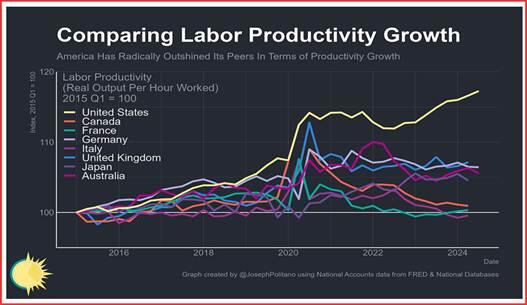

“The gains are impressive. The growth in labor productivity, which has averaged 2.3% in the past two years, is about half a percentage point faster than in the four years before the pandemic. While it may not sound like much, that difference would shave almost 10 years off the time it takes to double the level of real GDP. “ This is better than anyone else—see the chart.

What’s behind it? New business formation, labor quits that ended up with workers in jobs that better suited their skills. Unfortunately the quits rate is stalling.

Fortunately the employment component of the manufacturing PMI hit a 5-month high and all this building suggests it’s not ending soon. The prospect of unemployment is very low, no matter what JOLTS says today, and the labor shortage continues to threaten wage-ush inflation. As we noted at the time, Mr. Powell’s supposed concern about jobs--that took the place of inflation at the top of Fed concerns--was a ruse all along.

Central bank meetings

RBA December 9-10.

BoC December 11.

ECB December 12.

Fed December 18.

BoE December 19.

Bank of Japan Dec 19.

Forecast

The dollar “should” continue to make gains on excellent economic performance and signs of more to come. And the yield differential is still wide and healthy. Politically, the US has a terrible drag in the form of Trump, but of more immediate concern, both of the biggest two European countries are about to lose their government leaders.

Logic and historical precedence say the dollar should solidify gains and keep going up. But logic doesn’t always rule in markets and we need to worry that the Big Players will see the euro as overly oversold and take it higher.

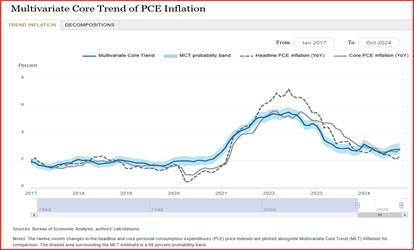

Inflation Blather: We like heavy-duty economic analysis as much as the next guy, but the most recent NY Fed report is hard to swallow. In the Oct update., the core inflation trend is flat at 2.8% (from 2.7%). Housing and services are sticky. See the chart.

The Fed does not project inflation out into any future timeframe. That’s not its goal. But we think it’s the Fed’s job to do exactly that whilst we are inundated with panicky talk about how Trump tariffs are going to raise inflation back to 9% (or something). The Fed has some of the top economists. We want them to work on this one thing.

Context: Before looking at recent specific Trump-driven currency moves, we need to keep in mind what Bloomberg names “digesting Trump’s tariff threats.” Bringing together a panel of experts, it deduces that “If there’s an important lesson worth revisiting from his first trade wars, it’s that Trump’s warnings regularly run into procedural, political and even economic constraints. The result is often a largely symbolic version of the headline threat, or one that ignores it altogether. Disruption and drama rather than destruction is the way Trump’s trade wars have operated.”

A good example is NAFTA, which ended up being rebranded something else but not dead. This time crude efforts to curtail Biden’s investment in infrastructure and industries will meet with opposition from his own party from red states, the chief beneficiaries.

The Bloomberg panel doesn’t dismiss the risks to the US of Trump’s intemperate rants. “This time around the economic consequences are arguably greater. A 25% tariff on imports from Canada and Mexico would kill the USMCA, Trump’s rebranded NAFTA. It would hurt the trade-dependent economies of border states like Texas and be a massive blow to the auto industry and others with regional supply chains. It also would raise the very consumer prices Trump vows to bring down.

“A 100% tariff on imports from BRICS countries would do more harm to the dollar’s global standing than any efforts to build an alternative currency. Never mind the loss of its safe-haven identity. The dollar’s reserve status depends on demand driven by its use in trade and financial transactions. Less trade with Brazil, China and India would just mean less demand for dollars.

“The tariff threats will continue. But for the next four years it’s worth taking a beat when they emerge. Not everything turns out quite as ordered in a late-night post.”

We are not so sure. Tariff is the favorite word these days but it won’t be long before Trump picks up another to hammer us with—lower interest rates. This is especially so if the Fed defies the market and declines to cut at the December meeting.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat