Think ahead: US jobs data and the ECB’s inflation test

In a holiday-shortened week in the US, Thursday’s June jobs report should be a cause for cheer, while falling gasoline prices are also helping ease inflation pressure. In Europe, eurozone inflation data will test ECB rate hike expectations.

Think ahead in developed markets

United States

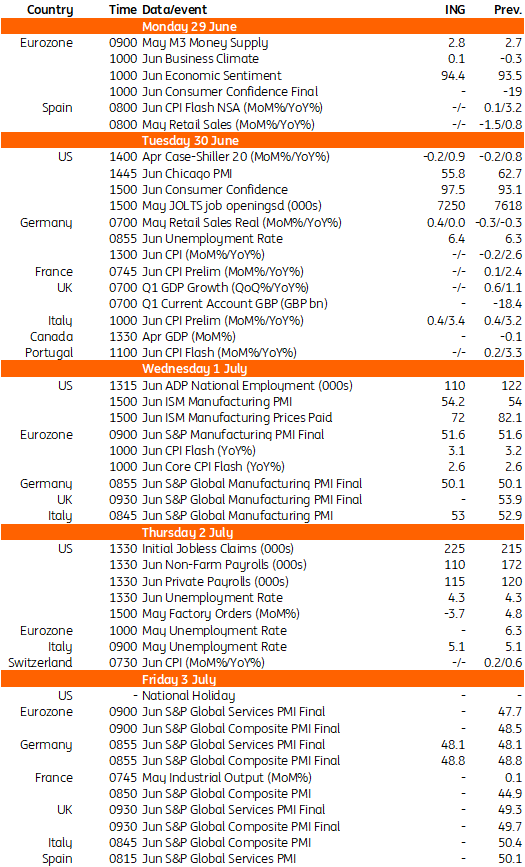

Jobs report (Thu): America will be celebrating the 250th anniversary of the signing of the Declaration of Independence next Saturday, resulting in a holiday-shortened week. Thursday’s June jobs report should also be a cause for cheer, with the fourth consecutive 100k+ reading for non-farm payrolls having averaged merely 8,500 per month between January 2025 and February 2026. While a print of around 110k will not be especially stellar, it will be enough to keep the market pricing Federal Reserve interest rate hikes. The ongoing fall in energy prices is another cause for celebration, with gasoline prices set to break below $3.50 per gallon imminently. This will leave more money in consumers’ pockets while also prompting sharply lower inflation readings over the next few months. Manufacturing surveys also suggest a decent ISM report, which, all in all, means we expect a week that should be supportive for risk appetite.

Eurozone

June economic sentiment indicator (Mon): After a sluggish PMI, the question is whether the second big survey on the eurozone economy shows more improvement. The Middle East deal will not have been fully incorporated yet, but with oil prices already moderating before the deal was struck, sentiment should see some improvement. Consumer confidence, part of the indicator, has already been released and indeed ticked up. Not only sentiment about output, but also inflation sentiment is very relevant. If fewer companies intend to price through higher costs, this will be a clear dovish sign for the ECB.

Inflation (Wed): The key indicator for next week will be inflation for June from a eurozone perspective. Some positive notes on inflation recently, as businesses seem more wary about increasing prices and, most importantly, prices at the pump have come down in recent weeks, which brings the annual increase down compared to May. Markets have been adjusting ECB rate hike expectations down and the June number will be a clear mark for how concerning the inflation situation is now that the deal will bring additional relief.

Think ahead in Central and Eastern Europe

Poland

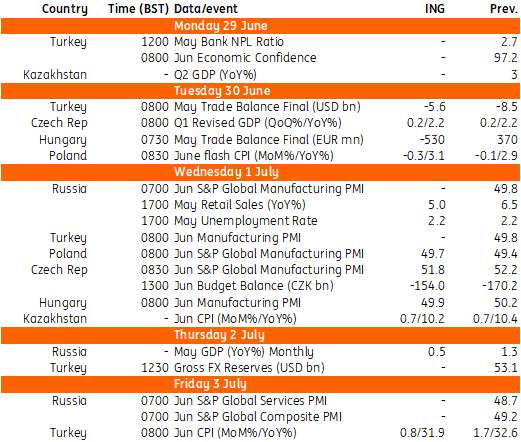

June Flash CPI (Tue): We project a further decline in headline inflation amid a visible decline in fuel prices vs. the previous month, even though the excise duty on gasoline and diesel was restored to its regular levels from the beginning of the year. Food price inflation remains benign, and core inflation was likely broadly unchanged compared to May. All in all, the National Bank of Poland is unlikely to signal any deviation from its wait-and-see policy stance in early July, and the new inflation projection should show that inflation might be heading towards the target, potentially as early as 2Q27, meaning there is no need to hike rates. At the same time, the return to cuts is unlikely any time soon, given the uncertainty regarding the impact of the recent Middle East conflict on prospects for the global economy.

Czech Republic

June Manufacturing PMI (Wed): The Statistical Office will likely confirm the 1Q GDP take, though we see some scope for upward revision of the soft quarterly growth. Industrial PMI is expected to have marginally deteriorated in June, while it remained safely in expansionary territory, proving a welcome resilience of Czech manufacturing to the Middle Eastern disturbance.

Turkey

Inflation (Fri): We expect monthly inflation to moderate further in June to 0.8%, resuming a downtrend in the annual figure to 31.9% from 32.6% a month ago. This would be driven by unprocessed food prices thanks to a recovery in agricultural production and favourable rainfall so far this year, while the rapid decline in oil prices is also supportive for energy inflation.

Key events in developed markets next week

Key events in Central and Eastern Europe next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.