The Fed’s ruse of citing the labor market to cut rates has been exposed

We get the ISM manufacturing PMI later today and it can be a market-mover, but expectations of improvement are low and manufacturing is a small part of GDP, anyway. Besides, we have juicier things to think about.

Top of the list is the lower weekly unemployment claims yesterday to an 8-month low. This set off a new round of betting against Fed rate cuts. The Fed’s ruse of naming the labor market as a reason to cut rates has been exposed as just that, a ruse.

Because construction spending was higher than expected, we can expect the next Atlanta Fed GDPNow to show an increase. We get a new forecast today, after yesterday’s 2.6%, which was a revision from 3.1 percent on December 24. We now expect it to go back to 3% or more, compared to the Fed’s expectation of 2%.

A robust economy and a Fed on hold is a good thing unless you are trying to buy a new house. Mortgage rates have gone back to 7%.

The Fed is going to have a hard time justifying the next rate cut. The next Fed meeting is Jan 29 and the CME FedWatch tools shows a mere 11.2% now expect a rate cut at that meeting. We do not get the PCE release until a few days later (Jan 31).

As noted before, the other key central banks are all expected to cut this year. The number of cuts might be shaved as things develop, including eurozone inflation next week. In Japan, those betting on a BoJ rate hike have retreated but we are not seeing the dollar highs we had Christmas week. They are seemingly quite persistent. See the 2-hour chart.

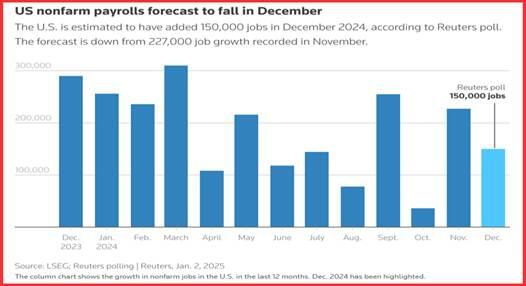

Forecast

The dollar is on a roll with plenty of data backing up the idea that the economy is so strong it’s probably overheating. The Fed can’t cut rates under these circumstances. But wait, we get nonfamr payrolls next Friday and that has the potential to alter the outlook. See the chart from Reuters.

And we have various factors coming at us from left field, including whatever ridiculous things Trump will say as the Jan 20 inauguation comes closer. A rise in risk from US politial conditions does not harm the dollar, at least not in recent history and not yet. We must expect the customery pullback next week, though, so sttay alert.

Keeper Tidbit: The St. Louis Fed has the schedule for 2025 release dates of the PCE data.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat