The Fed is right to stick to its tapering acceleration story

Outlook: We get the usual weekly jobless claims today, likely an okay number after the previous week had the Veterans Day holiday. Trading Economics predicts 245,000 vs. the consensus of 240,00 and 199,00 the week before.

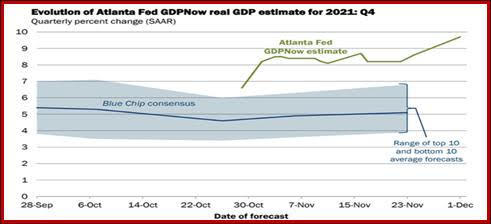

It should go without saying that while we are reeling from panicky risk aversion when that goes away, we will be flying on optimistic moonshine--again. In other words, assuming Omicron is tame and our current vaccines are adequate, we will be back to the Wild West—check out the Atlanta Fed and its 9.7% growth projection—up from 8.6%. Yesterday’s ISM manufacturing index rose to a respectable 61.1 in November (60.8 in Oct) for the 18th month if expansion. The ADP report shows the most new jobs created are at big firms, not mom-and-pop shops.

Many folks think past data has lost its glow because Omicron changes everything and initially we saw it that way ourselves. But it doesn’t, in part because the scientists are on top of it. The California docs worked all night to be able to confirm their one case was indeed Omicron—at 4 am. Scientists warned we would have to wait 2-3 weeks for them to get a grip on lethality and other characteristics, but we already see a pushback against the current exaggerated response to Omicron. The press is full of “buy the dip” advice.

The markets’ freakout was based to some extent on the Delta experience but we have no reason to suppose Omicron will be as bad or worse, and besides, we have some shreds of evidence it won’t be and will be easily managed. (That doesn’t mean the next variant won’t be far, far worse, but let’s not go there yet.) JP Morgan was only one of the advisors saying a less-lethal variant is consistent with how viruses mutate (apparently) and once that it recognized, it’s positive for risk appetite.

This perspective gives us (and Mr. Powell) every reason to suppose that in the US and probably several other countries, a new lockdown is not necessary, even if such a thing could be imagined. Growth is wild and woolly. That means inflation, and it means the Fed is right to stick to its tapering acceleration story. The next FOMC is Dec 14-15. The FT has clever wording—Powell “looks past Omicron threat.”

As for the Atlanta Fed GDPNow model, it gets a jaw-dropping real growth (note that word real) of 9.7% (from 8.6% last week). This is based on the ISM report and construction spending as we’ll as the already top factors of real personal consumption spending growth from 7.9% to 9.6% and real gross private domestic investment growth increased from 12.5% to 13.1%. And that’s with a headwind of a dip in government spending. Granted, the Atlanta Fed has a long history of overshooting but we like it anyway (in part because they are such earnest Boy Scouts).

Finally, the deliberately incompetent Congress can’t figure out how to run the business of the government and funding is ending, perhaps as early as tomorrow. (TreasSec Yellen ad said Dec 12). Unless a continuing resolution gets passed PDQ, the risk of a government shutdown is all too real. One source says the Republicans are staging the shutdown to last only the weekend as punishment for Biden’s vaccine mandates.

Manufactured crises seem not to generate much concern in the bond market but we wonder if these recurring events do not add to the growing pile of no-confidence reasons in the US. Those include gun-toting teenagers, tinfoil-hat conspiracy theory members of Congress, seemingly bad courtroom decisions, and the Supreme Court itself (again). We have spent an inordinate amount of time in recent months watching trials on TV, and that follows watching two Trump impeachments. Just as the UK has lost global respect in its handling of Brexit, especially by breaking deals, the US has lost respect for allowing the lunatic fringe to dominate instead of majority rule, and that includes the Trump presidency.

All the same, let’s assume the Fed is what counts and specifically its response to non-transient inflation. The odds of the first hike being accelerated to May are already higher. It’s a little amusing that the supply chain problem could be well on its way to being resolved by then, so if the tapering and intention to hike are effective in dialing back excessive pre-emptive buying, inflation could fall fast and a lot. But we can’t count on it, not least because some commodity and food-producing nations are still facing rising old-school Covid and that shortfall in vaccinations. We still expect risk-off to fade away or perhaps collapse all at once in a heap. The dollar should regain favor.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat