The Fed didn’t make any commitment to rolling back

On the whole, not much here to impress and we are stuck with Monday morning quarter-backing on yesterday’s Fed.

Watching Bloomberg TV yesterday while waiting for the Fed, the top-drawer analysts pushed back against the 50 bp idea and were quite convincing it would be 25 bp. This is not to criticize but to highlight that the current cycle is really, really weird. Because of Covid, it’s also unprecedented, making history and experience less useful. And as noted, logic is not always the top factor in price movements, especially the one-time data-driven events.

And we still have some anomalies. Go back to the dot-plot chart on page 2. The Fed projects another 50 by year-end and then yet another 100 bp in 2025. The terminal rate is 2.75-3.0%. But the futures market still sees 75 bp this year and an additional 50 bp next year over what the Fed has.

This means the market is betting on a return to near-zero or even negative inflation—the days of yore!—and that’s almost certainly a pipedream.

We are going to eschew discussion of the neutral rate, the supposed Fed target, for several reasons, chief among them that nobody knows what it is and it changes all the time, anyway. The biggest objection to the neutral rate, the rate which neither raises nor lowers inflation, is that external forces can shove it off any path. The assumption of the neutral rate is that the US economy is self-contained and the chief contributor to inflation is demand. This is foolish when we just had an external supply chain disruption that has nothing to do with demand. We have been complaining about the natural rate since oil crises…

More important, probably, is that the Fed didn’t make any commitment to rolling back QT. Those scratching for grievances will pick up on that. Reuters notes that in the UK, some announcement on balance sheet reduction is expected at the November policy meeting. “If it repeats prior years' targets of a 100 billion pounds runoff over the next year, that could reduce active BoE bond sales sharply because a heavy schedule of maturing debt over that horizon will see bonds fall off organically over the coming 12 months.” We hope it’s not naïve to say fewer bonds/lower supply, higher yields.

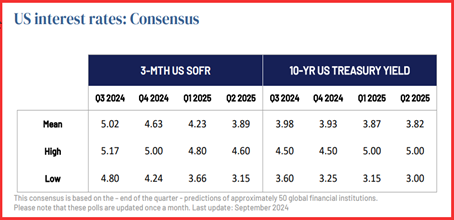

Forecast

The charts mostly point to other currencies resuming their rise, but the only one that carries real confidence is the AUD. We joke that the AUD is our canary in the coalmine because when we get a definite, confirmed move, it tends to be the first. We will wait a day or two for confirmation in the others.

The consensus viewpoint is that the dollar is toast with all these rate cuts, whether the Fed’s expectations or the market’s. The cuts are supposed to bring down yields and thus the yield differential, which will favor the dollar less going forward. But the differential will still favor the dollar, just by less. Confusing? You bet. And remember the long-term forecast yesterday showing that at the high end, the 10-year could be 4.5-5.0% and at the low end, not less than 3%.

The FX markets trades on news now, not 6-9 month projections, but it also tracks the bond market pretty closely. We are not so sure it has that much further to fall. Today’s small rise in the 10-year yield is a knee-jerk reaction to prices overshooting. Is there more to come? We wouldn’t be contrarian and buy the dollar, but we wouldn’t have a big short position, either.

Political Tidbit: The latest Silver Bulletin survey of surveys has Harris at 49.1% and Trump with 46.0%. Polls are not election results, alas.

Trump had warned the Fed not to cut rates before the election and complained when it did, saying “To cut it by that much, assuming they’re not just playing politics, the economy would be very bad, or they’re playing politics.”

And it’s true that consumers will start getting lower rates on all the stuff they borrow to buy and own, which might make some Trumpers less aggrieved and angry even if they try to hold on to negativity.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat