The ECB is changing faces: Could policy change next?

The European Central Bank is entering an unusual period of transition, with several changes in its top leadership. The reshuffle comes at a time when the ECB is balancing persistent inflation risks, fragile economic growth and rising political tensions across Europe. Will these appointments alter the direction of monetary policy, or instead reinforce continuity?

The beginning of June has brought several changes within the ECB Governing Council: Luis de Guindos’ departure from the vice presidency, with Boris Vujcic taking over as of Monday, coincides with François Villeroy de Galhau’s exit from the Banque de France, where Emmanuel Moulin officially assumed office on Tuesday. Christine Lagarde remains ECB President for now, but speculation about an early departure before the end of her term in October 2027 has already triggered the succession debate.

Boris Vujcic: A continuity candidate with a hawkish bias

Boris Vujcic arrives at the ECB vice presidency with extensive experience in central banking. Governor of the Croatian National Bank since 2012, he oversaw Croatia’s entry into the Eurozone in 2023. His appointment is also symbolic, as he becomes the first Executive Board member from a country that joined the European Union (EU) after 2004.

In policy terms, Vujcic is generally viewed as a moderate hawk. He has consistently emphasized price stability and appears reluctant to ease financial conditions too quickly when inflation remains vulnerable to renewed pressures. This does not mean he will automatically advocate higher interest rates, but rather that he is likely to support a cautious, gradual and strictly data-dependent approach.

As a result, his arrival does not fundamentally change the ECB’s balance in the short term. However, it may reduce the influence of more dovish policymakers if inflation accelerates again due to energy or geopolitical shocks.

Emmanuel Moulin: Technical expertise meets independence concerns

Emmanuel Moulin’s appointment at the Banque de France is more politically sensitive. His career spans senior positions at the French Treasury, the Ministry of Finance, the Prime Minister’s office and the Presidential palace. He brings deep knowledge of financial markets, European affairs and state institutions, making him a strong candidate to represent France within the ECB Governing Council.

Yet that same background has also attracted criticism. His close ties to President Emmanuel Macron have raised questions about the independence of the Banque de France, particularly since François Villeroy de Galhau stepped down before the end of his term. In central banking, independence depends not only on legal safeguards but also on public perception that policy decisions remain insulated from political influence.

Moulin’s monetary policy profile is also less well defined than that of his predecessor. Villeroy de Galhau championed what he described as “agile pragmatism,” adapting policy recommendations to evolving economic conditions. Moulin may ultimately follow a similar path, but the lack of a clearly established public stance on monetary policy makes his early interventions especially important.

Lagarde and the risk of a politicized succession

Christine Lagarde’s situation adds another layer of complexity. According to several reports, she may be considering leaving before the official end of her mandate, potentially allowing French President Emmanuel Macron and German Chancellor Friedrich Merz to influence the selection of her successor ahead of the French presidential election in 2027.

The ECB has repeatedly denied that any decision has been made, and Lagarde herself insists she remains focused on her responsibilities. Nevertheless, the mere existence of such speculation is enough to politicize the succession process. An accelerated appointment could be presented as an effort to shield the institution from a possible Eurosceptic victory in France. It could also be criticized as an attempt by current governments to secure key positions before a major political shift.

The risk for the ECB is not merely institutional. It concerns credibility. After navigating successive crises, including the pandemic, Russia’s invasion of Ukraine, the inflation surge and global trade tensions, and currently the consequences of the war in Iran, the ECB must preserve its image as an independent authority focused on price stability rather than national political considerations.

An ECB likely to become more cautious than dovish

At this stage, the leadership changes do not point toward a more accommodative policy stance. Vujcic leans toward caution on inflation. Moulin’s views remain largely unknown, but his profile as a crisis manager and senior European policymaker suggests institutional continuity rather than a major shift. The real turning point may come with Lagarde’s eventual successor, if that appointment alters the balance between hawks and doves within the ECB.

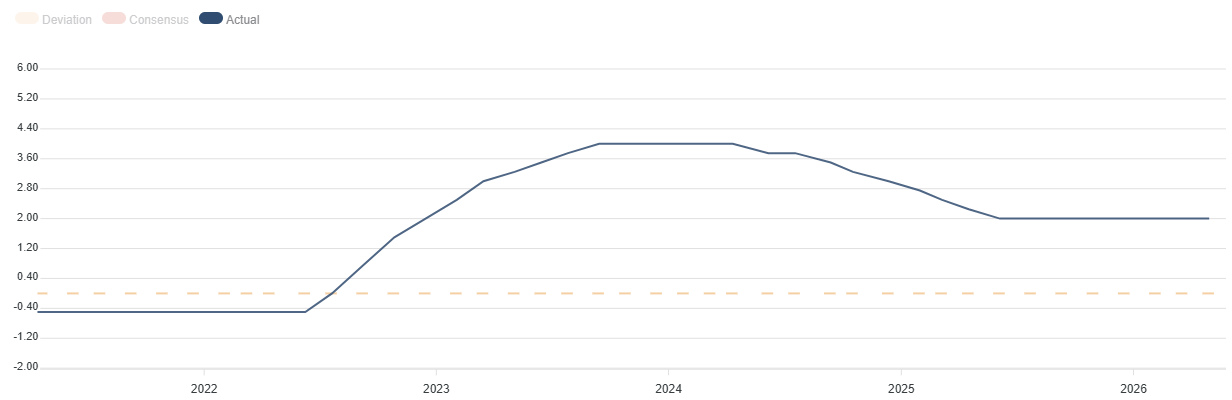

For now, the ECB is likely to maintain a cautious approach, avoiding strong commitments on the future path of interest rates. For next week, most economists expect the central bank to increase interest rates by 25 basis points, the first hike in nearly three years, as inflation rose to 3.2% in May, drifting further away from the 2% target.

The dominant message should remain one of data dependency, with particular attention paid to wages, core inflation, energy prices and signs of weakness in economic activity.

The paradox of this transition is that it aims to preserve stability within the ECB while simultaneously exposing the institution to accusations of politicization. That tension, between monetary continuity and political reshuffling, could become one of the defining European themes over the coming year.

ECB FAQs

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy for the region. The ECB primary mandate is to maintain price stability, which means keeping inflation at around 2%. Its primary tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

In extreme situations, the European Central Bank can enact a policy tool called Quantitative Easing. QE is the process by which the ECB prints Euros and uses them to buy assets – usually government or corporate bonds – from banks and other financial institutions. QE usually results in a weaker Euro. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The ECB used it during the Great Financial Crisis in 2009-11, in 2015 when inflation remained stubbornly low, as well as during the covid pandemic.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the European Central Bank (ECB) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the ECB stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Euro.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.