The CPI data showed inflation is quite broad-based

Outlook

Inflation is due not just to the price of gasoline. The CPI data showed inflation is quite broad-based, encompassing shelter and food. On top of that, as Mish has been pointing out, real average earnings have been falling since Trump took office.

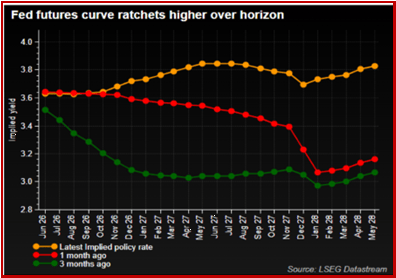

Boston Fed chief Collins said the Fed can’t continue looking through supply shocks; inflation is above target for five years now and is rising again. The consensus is building that a rate hike is inevitable. See the chart from Reuters. Even incoming chief Warsh’s favored trimmed mean version is on the rise.

Reuters points out that “A Fed futures market that confidently bet on two more rate cuts right up until the attacks on Iran inlate February currently seesno further easing and puts an 80% chance of a 25-basis-point rise in the 3.625% policy rate over the next 12 months.”

And yet many still do not accept the outlook. “… the wider investment world still treats further easing as its base case - presumably assuming an end to the Gulf conflict and a retreat in oil prices will reopen the Fed door.

“Just threeweeks ago, only one of 62 economists and strategists polled by Reuters expected a rate rise by the middle of next year. The median view was for two more cuts over that time.

“This week, even as lousy inflation data forced many banks and forecasters to push back their easing timelines, rate cuts remain in the mix.” UBS sees cuts starting in Sept. Morgan Stanley sees cuts next year.

We worry that the timeline is wrong. We could have hikes this year AND cuts next year, depending on the outcome of the war. Not to be silly, but the stock market shrugging off inflation data is favorable. We are not seeing an exodus to a safe haven, therefore a safe haven is not needed. Besides, equity gains are far bigger than stodgy old fixed income gains, even at 5%.

Today we get import/export prices, yawn, the usual weekly jobless claims and April retail sales. That’s the one to watch. Bloomberg expects a 0.5% rise in sales, or 0.3% ex autos and gasoline. Core retail sales, which also excludes food service and construction materials, should rise by 0.4% from 0.7% in March. We say the endlessly materialistic American consumer will keep spending on goods, inflation or not. The lower quartile of income-earners is using credit cards (although distress in the form of defaults is not yet scary).

Forecast

The dollar rallyette may be stalled for the moment, but there are several reasons for it to resume. First, conditions in some places are pretty bad. In the UK, PM Starmer may be facing a realistic challenge. Markets don’t like political turmoil, especially those that involve fiscal matters, which is at the heart of voter discontent.

Then in Japan, the dollar/yen is moving in baby steps to the line in the sand at 158, with some betting the MoF will accept the inevitable and decline to waste money intervening.

A worry is that the AUD is going its own way and posting new highs. It’s supposed to be our canary in the coalmine, but behaving the opposite of the big picture outlook. Instead it was the CAD that surrendered to the USD first.

The EM’s are not delivering much evidence. The dollar/yuan and peso are still fading. A sad tidbit: we don’t follow the Indian rupee but note that overnight it fell to a new record low. The government then announced it will consider lowering taxes on foreign investors in the bond market. This is smart but a few days late.

Finally, the euro is stumbling along lower but not yet at a convincing downside breakout. It is perhaps being supported by the idea of a June rate hike, although that remains in question.

Some smarty-pants pointed out that the biggest obstacle to the dollar recovery would be re-opening the Strait of Hormuz. This is true but not useful, as Mrs. Saunders used to say when the class struggled to justify a geometry problem. The Strait is nowhere close to being re-opened. US allies and friends, even including Japan and China, refuse to join in a re-opening effort. China could probably do it in one fell swoop by saying it will stop buying Iranian oil unless the Strait is opened for everyone. This is not a bad idea but we have no reason to think Pres Xi would bail Trump out at this point, now that he has the US president on his knees.

Tidbit: Trump’s vanity knows no bounds. It’s not just adding his name to the Kennedy Center and airports, he is also putting his picture on US passports and is issuing a “commemorative” gold coin with his face, like a Roman emperor. Now TreasSec Bessent admits Trump will be signing new banknotes alongside his own signature. As Bloomberg points out, there is also a $100 bill with his face on it, although that could be joke on his part. We doubt it.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat