Seven Fundamentals for the Week: “Liberation Day” tariffs and Nonfarm Payrolls to rock markets

- US President Trump's tariff announcements will keep markets busy all week.

- Key business and labor market indicators compete with Trump's announcements.

- US Nonfarm Payrolls for March end the week with a blast.

New quarter, even more action – United States (US) President Donald Trump is set to announce tariffs in the middle of the week, but reports, rumors and counter-measures will likely dominate the headline. It is also a busy week on the economic data front, with a full buildup to the Nonfarm Payrolls (NFP) data for March.

1) Liberation Day Tariffs may be softer, auto tariffs and countermeasures harder

Even Japan is ready to retaliate – the country that has accepted Trump's tariffs in both of his terms seems angry after the president announced 25% levies on cars. Do these duties, due on April 3, mean that the "reciprocal tariffs" of April 2 will be softer?

It is hard to know with Trump, and his threats to hit his allies harder if they cooperate further raises uncertainty. In general, markets dislike impediments to global trade, which means higher prices and weaker growth. More lenient levies and moderate countermeasures by Europe, Canada, and Mexico would be possitve for Stocks.

However, in his second term, Trump seems less eager to use tariffs as a bargaining chip, but rather as an end in itself. For traders, it could mean a "sell the rally" playbook to any piece of good news – as adverse developments would likely follow.

In any case, high uncertainty, the inability to predict the timing of headlines, and the president's unpredictability mean highly volatile trading.

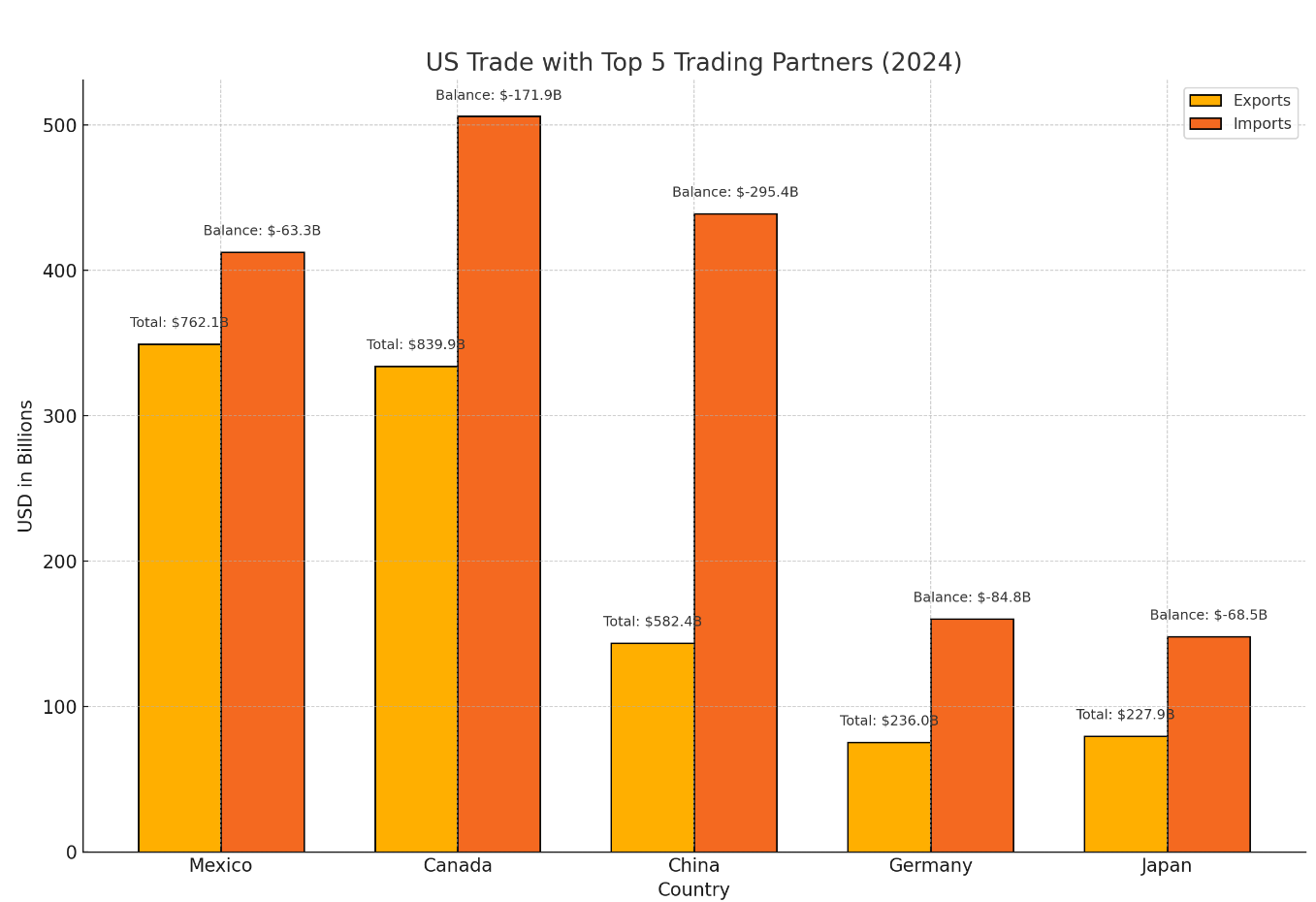

US trade relations with main partners:

2) RBA may surprise with a rate cut

Tuesday, 3:30 GMT. The Reserve Bank of Australia (RBA) has been one of the last central banks to cut interest rates – and a hawkish tone accompanied its decision. Therefore, no change is expected for this meeting.

However, recent Australian data missed estimates: the land down under shed jobs, and inflation rose by only 2.4% YoY in February. In addition, growing uncertainty about global trade may also push RBA Governor Michelle Bullock to surprise with an interest rate cut. Conversely, she may oversee an "unchanged" decision but signal that a reduction to borrowing costs is on the cards.

The decision may have an impact beyond Australia's shores – as central banks are watching each other, especially in these times. A warning about trade may reverberate around the world.

3) ISM Manufacturing PMI provides insights into how the industry feels about tariffs

Tuesday, 14:00 GMT. Institute for Supply Management (ISM) Purchasing Managers Indexes (PMIs) are forward-looking business surveys, and data for March, when trade tensions intensified, are closely watched. The first one is for the manufacturing sector.

After hitting 50.3 in February, just above the 50-point threshold that separates expansion from contraction in bussiness acitivity, there is room for retreat below that line.

Apart from the headline, investors will be watching the Prices Paid component, which represents inflation. It is of higher importance after another increase in the University of Michigan's Consumer Sentiment Index showed rising inflation expectations.

4) JOLTs measures confidence among employers and employees

Tuesday, 14:00 GMT. Published alongside the ISM Manufacturing PMI, JOLTs Job Openings for February seem somewhat lagging. They are less recent than the Nonfarm Payrolls, which are for March, but they are closely watched.

Officials at the Federal Reserve (Fed) eye any changes in hiring and also quitting trends. A higher level of voluntary departures means greater confidence, while the lack of movement reflects concern about job prospects.

The economic calendar points to a figure slightly lower to January's 7.74 million.

5) ADP jobs figures shape NFP expectations

Wednesday, 12:15 GMT. America's largest payroll provider showed a disappointing slowdown in private-sector job creation in February: only 77K jobs. Economists expect a rebound to 120K in March, which would still be low compared to longer-term trends.

It is essential to note that Automatic Data Processing’s (ADP) figures have a loose correlation to official NFP figures. Nevertheless, they have a short-term impact on markets, which can serve as an opportunity to go contrarian.

Moreover, they shape expectations for Friday's release, affecting real estimates that are not always reflected in the economic calendar.

6) ISM Services PMI is a view of the consumer from the viewpoint of businesses

Thursday, 14:00 GMT. Is America's largest sector doing well? The S&P Global Services PMI for March provided an upside surprise, shaking the growing worries narrative. ISM data carries more weight, and this release will test how businesses close to consumers feel about the economy.

The economic calendar points to a small decrease to 53 from 53.5 in February, which would still point to satisfactory growth.

The Employment Component is also important as another leading indicator of Friday's Nonfarm Payrolls. It stood at 53.9 points in February.

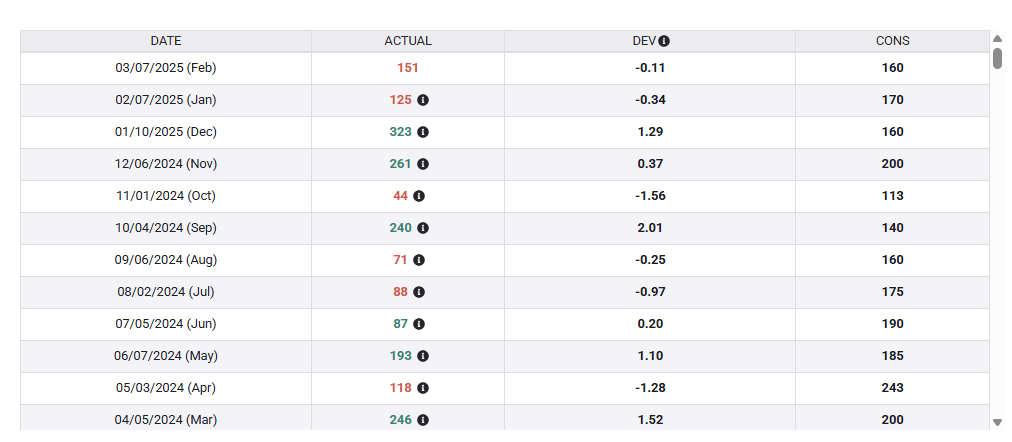

7) Nonfarm Payrolls may provide surprises

Friday, 12:30 GMT. The best is kept for last – the King of economic indicators. America's employment report may provide answers to several burning questions. Are firings initiated by the Department of Government Efficiency (DOGE) affecting the broader labor market? Are employers laying off people or clinging to them?

In February, headline job growth came out at 151K, within estimates. Still, the edging up of the Unemployment Rate from 4% to 4.1% – despite a decline in the participation rate from 62.6% to 62.4% – showed that the broader workforce is under pressure.

Economists project a more minor increase of 128K in March, accompanied by another small increase in the jobless rate to 4.2%.

Merely meeting these estimates would provide a sense of calm to investors wary of a downturn. However, an increase of under 100K cannot be ruled out, causing concern.

Nonfarm Payrolls. Source: FXStreet

Final Thoughts

This is one of the more consequential weeks in trading, coming after another market crash and as the fate of tariffs could possibly be decided. The combination of a busy week of economic releases and some end-of-quarter flows add to the mess.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.