Rumor has it that the hike in July is the end of the Fed’s hiking cycle

Outlook: Rumor has it that the hike in July is the end of the Fed’s hiking cycle. Even Ben Bernanke, former Fed chairman, says so.

Instead of giving that a 90% chance, we give it less than 50%. Or rather, we give the Powell speech next week less than 50% chance of saying anything remotely like “this is the last hike.” He is more likely to suggest that it will take several more core PCE readings showing real progress before hiking can be declared dead and buried.

It’s wishful thinking to imagine July is the end. Not to be a broken record, but as we keep pointing out, the most recent core PCE inflation rate was 4.62% but it was 4.88% the year before. This is not much downward progress by any stretch of the imagination.

A Reuters summary is interesting: “Pessimists think the Fed is not done tightening yet and any further rate hikes after next week will just hasten a downturn in 2024. That has sobered up the Treasury market a touch after a couple of weeks of disinflation relief.

“Futures are fully priced for a quarter-point rate rise next week, but indicated less than a 50-50 chance of another hike by November and 75 basis points of cuts from the peak by this time next year. Two-year Treasury yields nudged 12 bps higher to 4.88% on Thursday, but have settled back to 4.85% since.”

Two things of interest here: first, the Treasury market is operating on assumptions and expectations about the Fed—not economic data, including inflation data. Second, the Treasury market is flighty—up a bit, down a bit. We are not calling it “volatile,” just fickle and irresolute. That bleeds over to FX.

July not being the last hike assumes two things and both could be wrong. First, core PCE is the only measure the Fed cares about, or needs to care about in public to appear consistent. If that’s all there is, it’s correct to say July is not the last. It’s well nigh impossible for core PCE inflation to go from nearly 5% to 2% in a few months.

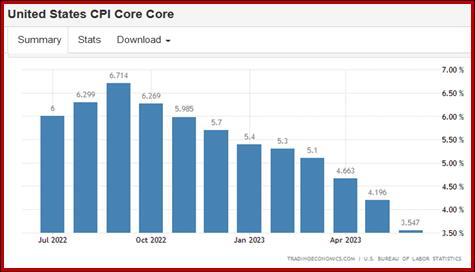

But remember that WSJ article last week about the harmonized version used in Europe. If we had that measure, core inflation would be under 3%. Then there is something named core CPI looks a whole lot better, only 3.55% in June from 4.2% the month before. Core excludes food, shelter, energy, and used cars and trucks. Since everybody eats, sleeps, and uses electricity, even if they don’t buy used vehicles, it seems a little silly to use it to forecast the Fed, but having said that, see the chart. And several other measures of inflation—and Trading Economics has dozens—show a similar sharp downturn. In fact, the PCE core is one of the few that doesn’t. So now we have to ask whether Mr. Powell’s preference for inflation ex-shelter and perhaps in a shorter timeframe (like q/q) can get him to the promised land.

And here’s a troubling side-note—if the drop in inflation has been due chiefly to supply chains getting fixed, we may well have squeezed all there is out of goods inflation. Services inflation remains. Many economists are noting that we have little evidence that Fe rate hikes have hit the real economy in any meaningful way. Case in point: doubts about peak Fed emerged yesterday on the still-tight labor market, initial claims down a measly 9,000 to 228,000 for the week ended July 15, the lowest level since mid-May. The Reuters forecast had been 242,000. You do not get a recession when the labor market is stubbornly tight.

Higher rates are not without some effects. Some banks that failed to hedge correctly, sure. The housing market and its upstream cousin, contractors. Some folks, including commercial real estate, with adjustable mortgages. We have yet to see the full scope of the demise of the urban office center, or even shopping malls (and Bloomberg notes bottom-fishers are already out and about). But that’s mostly fallout from Covid and the stubborn preference for working at home, plus the delights of shopping online, among other factors.

The Fed surely knows it is not having much effect on inflation in the usual ways—economic slowdown, unemployment, recession. Instead we have the Atlanta Fed estimating Q2 GFP at 2.4%. And the labor market data is hardly what you’d call dire or even a little scary. Hardly anyone is still calling for recession, or if we get a recession, it will be way off in the future and not all that bad. This is not to say the Fed wants a recession. It is to say that standard monetary policy is hardly working out the way the old models say it should—and we can lay blame at Covid’s door for a lot of the mismatch—and it must trouble the Fed. At a guess, this means the discussion at the FOMC next week will be lively and the while the vote this time may be unanimous, the board is about to fragment.

Bottom line: everything depends on what Mr. Powell says about the economy and the Fed’s thinking going forward. He will be coy and refuse to help, which is his job. Still, the Fed-watchers will parse every work for clues about peak rate or more hikes to come, even if “more hikes” comes with a maybe.

Forecast: If we deduce sentiment solely from charts, the dollar is on the way to a bigger upside correction, but it’s still just a correction, not a reversal. And the big danger is that the market’s broad assumption of one-and-done at the FOMC next week means the dollar “should” fall and pretty soon—Monday or Tuesday, of not today. This would be a good time to get out of Dodge and get square—traders may flee the scene today in preparation for a rout next week, incomplete correction notwithstanding. This is the worst-case pessimist’s scenario but the right one for the risk-averse.

Tidbit: Reminder—don’t forget that core PCE inflation is still sticky. Last week it came in at 4.62%, lower than the month before, but it was 4.88% the year before. For perspective, see the one-year core PCE vs. the 5-year. Still think the Fed will relent? We are going to keep these charts up for the sake of context. Remember them the next time someone says “higher for longer” is a dead duck.

Tidbit: We follow the stock market forecasts out of the corner of our eye but imagine many self-proclaimed experts are eating crow. What happened to the “sell in May” crowd and all the others predicting a crash that kept getting pushed out in time? Bloomberg picks one party surrendering: “Piper Sandler’s Michael Kantrowitz, the most bearish in a Bloomberg poll in January, has lifted his initial target of 3,225 to a range of between 3,600 and 3,800. ‘As we think about where the S&P 500 will end in 2023, the year-to-date move makes it difficult for us to continue justifying our year-end target that we published back in January as large-cap market indices have appreciated a lot year-to-date,’ Kantrowitz wrote in a note to clients.” We await the bigger names. Told you so.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat