Real GDP growth weaker than expected in Q1-2023

Summary

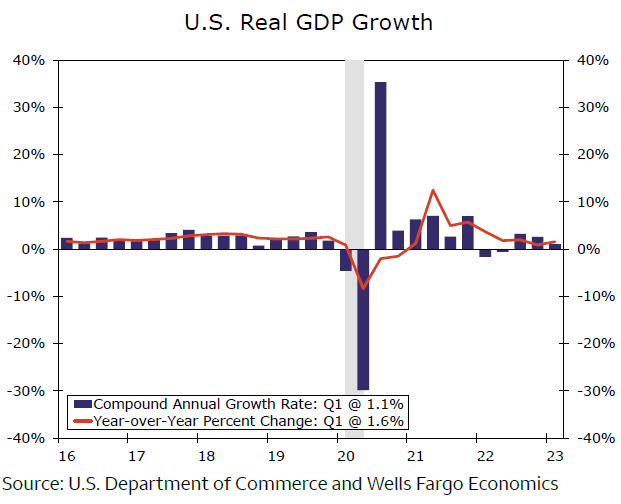

Real GDP grew 1.1% at an annualized rate in Q1-2023 relative to the previous quarter, which was weaker than the consensus forecast.

Real consumer spending rose at a solid rate of 3.7%. But, a significant inventory swing sliced 2.3 percentage points off of the headline real GDP growth rate. The other spending components were mixed.

Monthly data suggest that consumer spending has lost momentum over the past few months. Moreover, consumers are relying increasingly on credit and stockpiled cash to finance their purchases. These factors are not sustainable, in our view.

We continue to forecast that the U.S. economy to slip into recession, which we expect will be of moderate severity, in the second half of the year.

GDP growth print comes in below consensus expectation

Data released this morning showed that U.S. real GDP grew at an annualized rate of 1.1% in the first quarter relative to Q4-2022 (Figure 1). Not only did the outturn represent a slowdown from the 2.6% sequential growth rate that was registered in Q4, but it was also below the consensus forecast of 1.9%. The rise in the year-over-year rate of GDP growth from 0.9% in Q4 to 1.6% in the first quarter reflects low base effects from last year (i.e., real GDP contracted in Q1-2022).

Real GDP growth in the first quarter was driven largely by real personal consumption expenditures (PCE). In a report we published Wednesday, we noted that the Commerce Department had made some downward revisions to monthly data on retail spending data, and we flagged the potential for real PCE growth to be less robust than we initially had anticipated. Nevertheless, real PCE grew at a solid rate of 3.7% in the first quarter. That said, the quarter appears to have ended on a weak note in terms of growth in consumer spending. After surging 1.5% in January relative to the previous month, real PCE edged down 0.1% in February. If there are no revisions to previously published monthly data, then the 3.7% quarterly growth rate implies that real PCE fell 0.5% (not annualized) in March relative to February. (Monthly PCE data for March will be released on Friday, April 28.)

The other spending components were mixed in terms of growth. Real government spending grew 4.7%, and nonresidential construction spending jumped 11.2%. However, residential construction spending fell for the eighth consecutive quarter, down 4.2%, and real business spending on equipment dropped 7.3%, the second consecutive quarterly decline in this component. The 4.8% rise in exports was more or less offset, in terms of topline real GDP growth, by the 2.9% growth rate in imports.

Author

Wells Fargo Research Team

Wells Fargo