Rates spark: US regional banks cast long shadow over FOMC

It's far easier for the Fed to deliver 25bp today than to dare to hold. The latter would be a sign of concern. The former, one of conviction; but still needs explaining. Neither eurozone bank lending nor inflation made the case for a 50bp hike. Markets rightly price more ECB hikes but the end of the Fed’s hiking cycle will bring on aggressive ECB cut expectations.

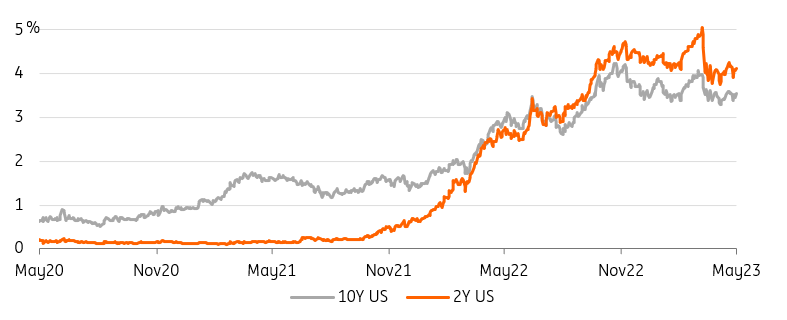

The deeply inverted curve continues to discount trouble ahead

For rates markets, the delivery of (a still) inevitable 25bp hike is not the issue. Signals for what is to follow are more important. And the Federal Reserve will not guide at this juncture for June. That leaves the market interpreting the language used in the press conference as best it can.

That said, the market discount for subsequent cuts is not coming from Fed guidance. Rather it’s a market discount partly built on what's happened in previous cycles, but one that has also been bullied there by banking sector angst. While still mostly idiosyncratic, the market discounts potential systemic implications. The renewed focus on First Republic’s woes keeps this theme at the forefront and is reflected in the 2yr yield trading back below 4% – more than 1% through the funds rate.

One mission for the Fed at this meeting will be to avoid giving the market an excuse to discount even deeper cuts, as that would effectively negate the effect of the 25bp hike delivered. The 10yr at sub-3.5% is even further through the funds rate and remains on a path towards the 3% area in the coming months. The Fed would prefer not to prompt a nudge lower, as it would see that as counterproductive at this juncture.

The Fed should avoid saying anything that would push Treasury yields even lower

Source: Refinitiv, ING

And the Fed will likely be quizzed on banking sector angst

Chair Jerome Powell will likely be quizzed about the banking sector at the press conference. On questioning, he will likely acknowledge the fall in bank deposits seen in the past year, but we would expect him to view this as a natural course of events, where policy has switched from quantitative easing to one of quantitative tightening. It will be interesting to see whether he draws this parallel, and also how he views the stresses being felt by some banks, in particular on the West Coast.

There should also be interest in commentary from Powell on the recent spurt of inflows into money funds, and the parallel inflows to the Fed's reverse repo facility, and any impact on bank reserves. He likely won’t go there, unless the question is asked. Should the Fed surprise with a decision not to deliver a 25bp hike at this meeting, such commentary would be made more difficult, as the Fed would be seen to be on the defensive. At the same time, the Fed would need to justify the hike despite the pressure on some banks.

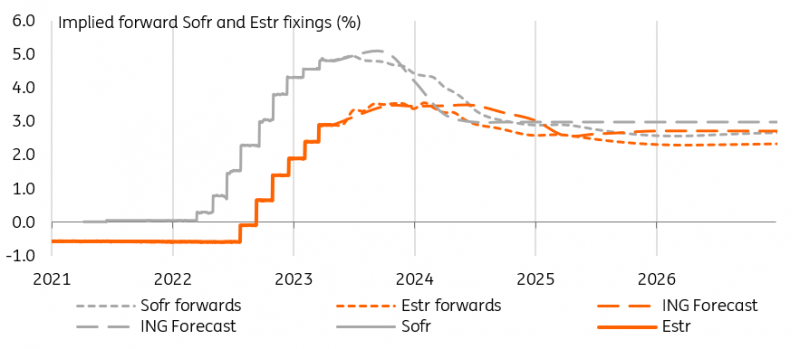

As the end of the Fed's hiking cycle approaches, calls for ECB hikes will grow louder

Source: Refinitiv, ING

Bank lending and eurozone inflation fail to make a case for a 50bp ECB hike

Over in Europe, the European Central Bank’s (ECB) Bank Lending Survey (BLS) confirmed the widely held view of a deterioration of credit demand and lending conditions by banks. This is less than one week after the March ECB meeting’s minutes showed its uncertainty about the speed at which monetary tightening was reaching the real economy. Slower lending, both driven by demand and supply, will be a key plank in the doves’ case that rates need to be raised only 25bp tomorrow, as opposed to 50bp.

Slower lending, will be a key plank in the doves’ case that rates need to be raised only 25bp tomorrow, as opposed to 50bp

As we wrote on Friday, we thought the bar was high anyway for the BLS to help the case for a 50bp hike. The other piece of the jigsaw was the April inflation report, which showed headline and core inflation coming roughly in line with expectations. The ECB will no doubt take solace from the sharp slowdown in core goods and food inflation, but services prices continued to accelerate. Overall, this was not enough of a surprise to bolster the case for another 50bp hike.

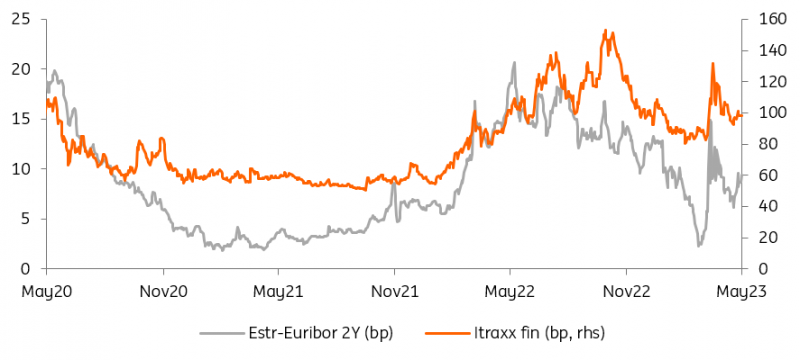

Systemic risk indicators are within recent ranges but the economic spillover is becoming more certain

Source: Refinitiv, ING

Bonds increasingly in favour as banking trouble worsens the economic outlook

If the above helped the bid into core bonds so far this week, the main reason remains worries surrounding the US regional banking sector. It looks like the relief brought by First Republic’s rescue was short-lived and the focus turned back to the sector’s structural challenges, to which markets now add higher FDIC insurance costs. It is beyond the scope of this publication to express a view on US banks but it seems logical in our view that the longer this sector’s troubles linger, the more likely the spillover to the real economy. Even if systemic risk indicators remain relatively muted, the fall in core yields on dimmer economic prospects makes sense to us.

The volatility in 2Y Treasuries yesterday for instance, trading in a 20bp range, is no doubt extreme, but we agree with the direction of travel. Fed funds forwards now price almost 63bp of rate cuts from the peak in May. We think this could accelerate quickly if the Fed modifies its forward guidance tonight as we expect. EUR swaps in comparison still price almost 75bp worth of hikes in this cycle, implying a policy rate peak around July, three months after the Fed. The resulting tightening of USD-EUR rates differentials makes sense to us but a dovish FOMC tonight would also fire the starting gun on more aggressive cut expectations at the ECB.

Read the original analysis: Rates spark: US regional banks cast long shadow over FOMC

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.