Polish interest rate hike veiled by uncertainty

The coming days will be action-packed as we will see two central bank meetings and a bunch of real economy data across CEE -" including further inflation prints for November. The Polish central bank will meet on Wednesday and, given the size of November inflation surprise, we expect the central bank to raise the key rate by 75bp to 2.0%. However, a smaller move cannot be ruled out due to the recent announcement of the “Anti-inflation shield” package by the government, slowing economic growth and pandemic worries. The Serbian central bank, on the other hand, has outlined several times it has no intention to raise rates in the near term and we expect it to hold its key rate steady at 1%. Romania will complete the 3Q21 GDP breakdown in CEE. Economic growth should be confirmed at 7.2% y/y (0.3% q/q), whereby in quarter-on-quarter terms a strong positive contribution from agriculture likely just about offset the large negative contribution from industry and construction. November inflation will be released in Hungary and Czechia. We expect an acceleration of consumer price growth in both countries, to 7.3% y/y in Hungary and 6.3% y/y in Czechia. Higher food and fuel prices were likely the key culprits behind the speed-up compared to the preceding month. Whereas this might be the peak in Hungary, Czech inflation could have to wait until January for that. Moreover, industrial production figures for October will be published in Czechia, Slovakia, Hungary and Slovenia. We expect negative year-on-year development in the first three countries, as supply-side issues bite manufacturers; however, Slovenian industry likely marked a robust 5% y/y increase.

FX market developments

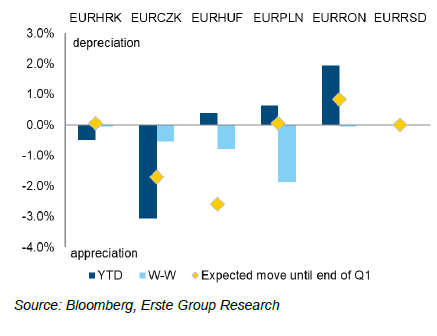

Increased volatility and the emerging market sell-off caused by the omicron variant was short-lived, as CEE currencies pared their losses and appreciated. The Polish zloty moved to 4.60 vs. the EUR, supported by a swing in the central bank’s rhetoric. Following a change in Jerome Powell’s view on inflation, Governor Glapinski also no longer sees it as transitory. He said that the central bank will bring inflation to ‘minimum levels’ without triggering high unemployment. Moreover, after the publication of flash CPI for November, which again surprised markets to the upside, the governor said that there is still room to raise interest rates, but ‘it is not unlimited’. Changes in the monetary policy toolkit and further tightening of monetary conditions supported the Hungarian forint. After shifting the interest rate corridor and significantly increasing its upper limit, the Hungarian central bank delivered a fourth consecutive rate increase in a month, as it raised the one-week depo rate by 20bp to 3.1%. All in all, we expect the MNB to hike the depo rate once again on Thursday and follow with a key rate increase next week (December 14). The improved global sentiment was positive for the Czech koruna, as it strengthened and moved back to 25.4 vs. the EUR. As far as the Romanian leu is concerned, it remains stable at 4.95 vs. the EUR. Nevertheless, if regional central banks continue to tighten monetary conditions in December and January, the pressure on the RON might increase and may force the central bank to intervene more aggressively.

Bond market developments

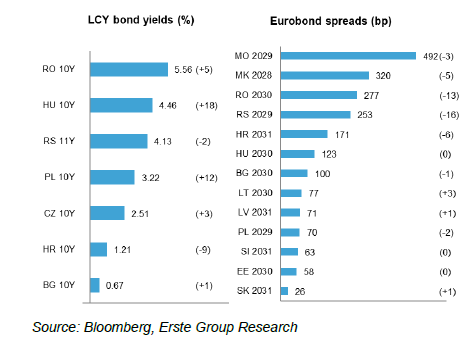

QE programs seem to be coming to an official end in the CEE region. Although the National Bank of Poland has already significantly lowered its bond purchases in recent months, for the first time since the launch of the program, it did not schedule a tender in December. However, the NBP does not rule out future operations, if required by the market situation. The bond purchase program is also in focus in Hungary and Governor Matolcsy said that the MNB will wind down its QE program to boost its monetary tightening efforts. We think that the MNB might continue to buy bonds in 1Q22, but likely at much lower volumes, up to HUF 10bn per week. At the December rate setting meeting, the MNB will review its weekly limit of purchases, which currently stands at HUF 40bn. Long ends of LCY curves went up in the CEE region, with the most pronounced increases observed in Poland and Hungary, where the 10Y yields returned to 3.3% and 4.6%, respectively. This week, two regional central banks will convene meetings. While the National Bank of Poland will most likely deliver another rate hike, the National Bank of Serbia is expected to keep the key rate unchanged at 1.0%. The NBS has been communicating that they are using other available tools to withdraw surplus liquidity from the market.

Author

Erste Bank Research Team

Erste Bank

At Erste Group we greatly value transparency. Our Investor Relations team strives to provide comprehensive information with frequent updates to ensure that the details on these pages are always current.