Poland’s economy falters but continues to outperform EU peers

September data points to a soft patch in Poland’s economic recovery in the third quarter. Industry suffered from weak external demand, construction suffered from the slow absorption of EU funds and high rates, while consumption eased on weaker real wages. We estimate third-quarter GDP growth to be 2.8%YoY and 3% overall in 2024.

Industrial output struggled in the third quarter

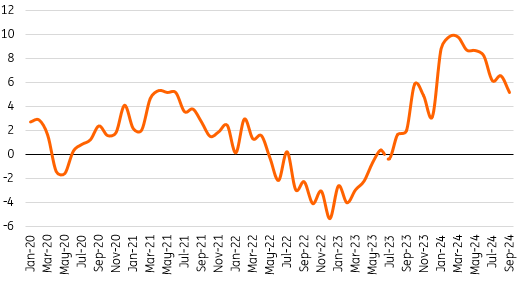

The recovery in Polish industry has stalled, with industrial production in September declining by 0.3%YoY, compared to our forecast of a 0.8%YoY decline and consensus of +0.3%YoY. The previous month also saw a decline of 1.2%YoY. Seasonally adjusted output slightly declined too in the third quarter (around -1.0%QoQ). Domestic consumption alone, even if very robust (we estimate around 4.0%YoY in the third quarter) isn't enough for this sector of the economy to expand.

Unimpressive industrial ouput performance in 3Q24

MoM 3m-month moving average (SA).

Source: GUS, ING.

We believe the production weakness is temporary. The investment impulse, associated with EU funds, is gradually gaining momentum. This year, beneficiaries will receive approximately PLN20bn from the Recovery and Resilience Fund (RRF), and around PLN60bn plus structural funds in 2025. This should also stimulate private investments, which have been subdued in recent years. Additionally, the German automotive industry showed some signs of recovery in August and continued improving in September.

The German economy faces significant structural problems, so we do not expect substantial support from this direction. To avoid industrial stagnation, as experienced by Germany and the Czech Republic, domestic growth factors are crucial. Poland has the opportunity to avoid the stagnation seen in neighbouring countries, as it possesses growth factors that can stimulate domestic demand. Besides strong consumption, we anticipate a revival of public investments and a boost to private investments through multiplier effects. Poland is just beginning to spend EU funds and has its peak ahead, while other countries are somewhat more advanced in the process. Overall, the third quarter was poor for the domestic industry, but we count on improvement ahead.

Construction continues to contract

Construction output fell by 9.0%YoY in September, slightly less than expected (consensus of -9.6%), following a 9.6%YoY decline in August.

Significant drops were observed across all construction categories:

-

Building construction (flats and houses) fell by 10.1% year-on-year (August: -7.9%).

-

Civil engineering works (basic infrastructure) by 8.9% (August: -10.6%), and.

-

Specialised construction activities by 7.9% (August: -9.8%).

The construction sector is experiencing a recession due to the slow uptake of EU cohesion funds at the beginning of the new financial period and the delayed disbursement of funds from the Recovery and Resilience Facility (RRF), which is negatively impacting civil engineering projects. We expect the situation to improve from next year only as beneficiaries will receive roughly twice as much from cohesion funds as this year along with significantly higher RRF abortion.

Residential building construction is also shrinking. The previous government's housing programme (mortgage subsidies) expired at the end of 2023, and a new one has not yet been agreed upon within the government coalition. The demand for housing is also being hampered by the highest mortgage interest rates in Europe.

Labour market metrics also point to slower growth last quarter

The average wage and salary in the enterprise sector amounted to PLN8141 in September, rising by 10.3%YoY (consensus: 11.1%). At the same time, average employment decreased by 0.5%YoY (in line with expectations) to 6.462 million people. According to the StatOffice, the decline in nominal wages vs. August was due to a reduction in the scale of additional payments that occurred in the previous month. Compared to August, the number of jobs in enterprises declined by 8,000.

Real wages growth slowed amid weaker nominal wages and higher inflation

Real wages, %YoY

The growth in wages is no longer as robust as at the beginning of the year when it hovered around 12-13%YoY, but it remains in double digits. Since mid-2024 inflation has rebounded significantly, reaching 4.5%YoY in the third quarter compared to 2.5%YoY in the second quarter. This has resulted in a marked slowdown in real wage growth (from 8.5%YoY to 6.0%YoY). Higher electricity and gas bills may limit resources available for other household expenditures.

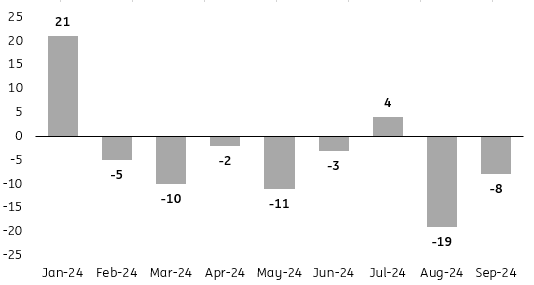

In our view, the slower growth in real wages has somewhat dampened the dynamics of consumption growth, which remains the main driver of the current economic recovery. The negative trend in employment also persists. Since January, the number of jobs in the enterprise sector has been reduced by 54,000.

Employment is shrinking slightly since the beginning of 2024

Change in enterprise sector employment, MoM, thous. of persons.

Still on track to achieve 3% GDP growth in 2024

The labour market remains in good condition but shows that the Polish economy hit a soft patch in the third quarter, after stronger-than-expected growth between April and June.

Data from the real economy confirms this view. Industrial production was stagnant and activity in construction contracted. We expect that the third quarter was also somewhat less favourable for retail trade, especially in goods, however demand for services most likely remained buoyant.

We forecast that household consumption growth eased towards 4%YoY in 3Q24 from 4.7%YoY posted in 2Q24. We estimate third quarter GDP growth of 2.8%YoY (3.2%YoY in 2Q24) and 3% for the whole of 2024.

Read the original analysis: Poland’s economy falters but continues to outperform EU peers

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.