Monetary policy’s long and variable lags: The case of the US

The Federal Reserve’s Senior Loan Officer Opinion Survey sheds light on how changes in monetary policy influence banks’ credit standards and expected loan demand. Based on the historical relationships, the latest survey points towards a high likelihood of average negative growth of the volume of company and household investments over the next several quarters. Moreover, recent research shows that since 2009, the maximum impact of monetary policy on inflation may be reached more quickly. Based on the relationship between credit standards, expected credit demand and investments by companies and households, as well as on the possibility that transmission lags have shortened, decisions by the Federal Reserve will more than ever be data-dependent.

Changes in official interest rates influence economic growth and inflation through a variety of channels whereby the effects tend to manifest themselves with long and variable lags. In a recent Ecoweek, using data from the ECB’s quarterly bank lending survey, the relationship has been analysed between, on the one hand, credit standards applied by banks and expected loan demand, and on the other hand, growth in the subsequent quarters in the volume of company investments, household investments and household consumption. Tighter credit standards tend to be followed by slower growth of company investments and households’ housing investments but the relationship with household consumption is very weak. When banks expect credit demand to be weak (strong), subsequent growth of company investments and households’ housing investments tends to be weak (strong). The relationship with household consumption is again very weak.

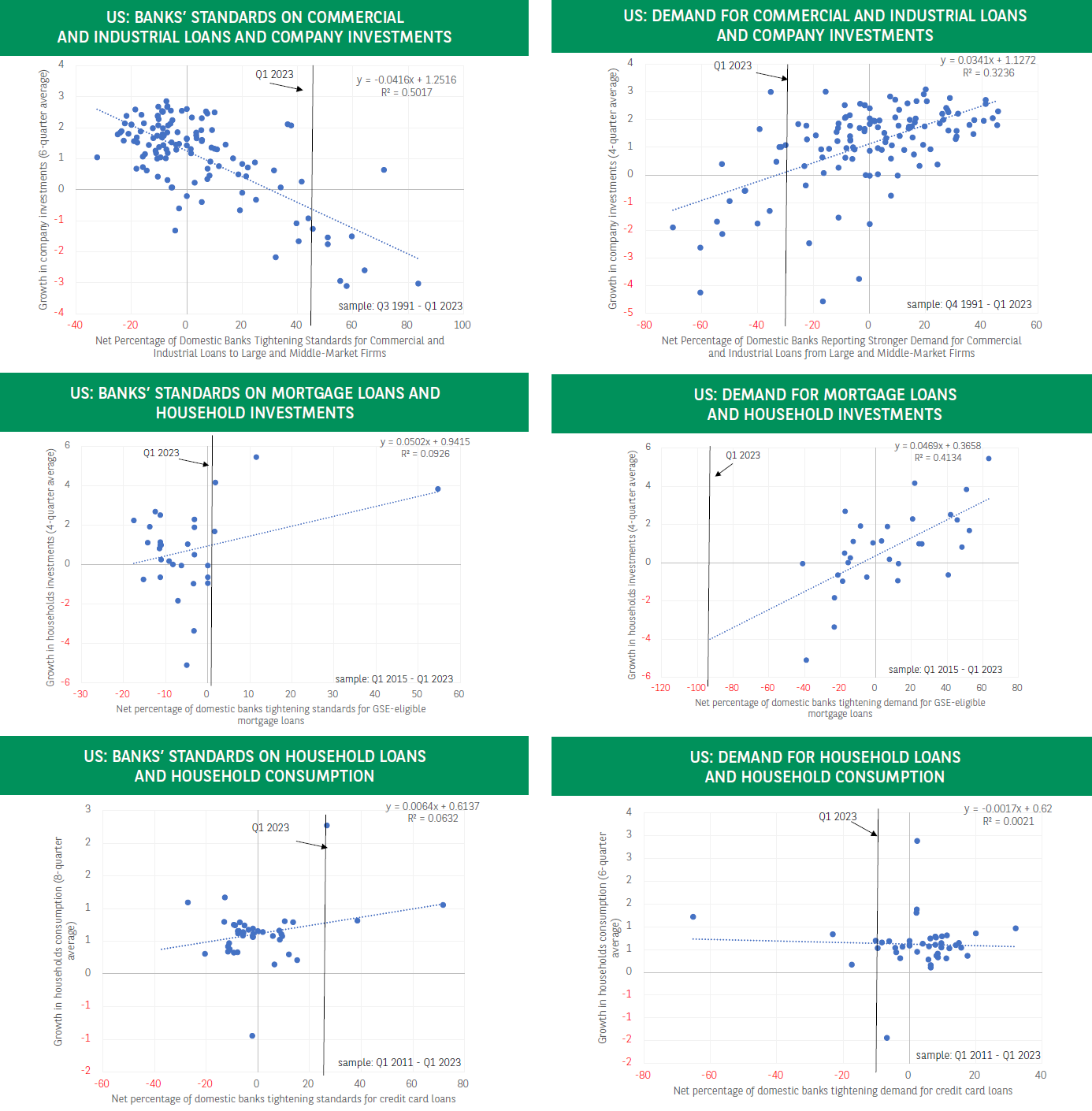

We have conducted a similar analysis for the United States, based on the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) and the results are shown in charts 1-6 as well as in table 1, which reports the regression coefficient and R² for various time windows. There is a clear negative relationship between the net number of banks reporting tighter credit standards for commercial and industrial loans and the average real growth of company investments over the next 6 quarters (chart 1). When banks expect weak (strong) credit demand from companies, the subsequent growth of company investments tends to be weak (strong) too (chart 2). The vertical lines show that in the latest survey (January 2023), compared to history, credit standards were already tight and expected loan demand weak.

Turning to household investments, which mainly consist of the purchase and renovation of dwellings, a negative relationship is also found between banks’ credit standards and the average real growth of housing investments over the next 4 quarters (chart 3). Weak expected credit demand is associated with a contraction in household investments in the following quarters as well (chart 4). In the latest SLOOS, credit standards were, compared to the historical range, already rather tight, whereas expected loan demand was very weak and close to the historical lows. Finally, with respect to household spending, like in the Eurozone, the relationships with credit standards and expected demand are very weak although they have the expected sign.

These results point towards a high likelihood of average negative growth of the volume of company and household investments over the next several quarters unless other factors would play a counterbalancing role. One such factor could be an early end of the tightening cycle by the Federal Reserve, which could boost confidence by reducing fears of a further hit to growth from higher rates. However, based on recent data -labour market, inflation- as well as comments by Federal Reserve officials, additional rate hikes still are to be expected. The further cumulative tightening will be data-dependent but it will also be influenced by the expected transmission speed of monetary policy. The latter point was addressed in a recent speech by Lael Brainard in which she mentions research of 2004 and 2015 showing that “it takes about 9 and 12 months … for monetary policy actions to begin to affect inflation and additional time for that effect to peak”. However, more recent research finds that “inflation effects from monetary policy occur much sooner and peak within the first 10 months.” Recent research by the Federal Reserve of Kansas City also points towards an acceleration of the effect of monetary tightening on inflation -with a maximum effect coming after 12 months- due to the use since 2009 of the central bank’s balance sheet (quantitative easing, quantitative tightening) as well as forward-guidance. According to the authors, the use of a broader range of instruments implies the risk of underestimating the effect of monetary tightening if one would only focus on the federal funds rate. Such underestimation would imply an overestimation of the lag between changes in monetary policy and its effect on inflation. To conclude, based on the relationship between credit standards, expected credit demand and investments by companies and households, as well as on the possibility that transmission lags may have shortened, decisions by the central bank will more than ever be data-dependent.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.