Since a 1977 act, the dual mandate of the Federal Reserve (Fed) has de jure entrusted it with the objectives of maximum employment and price stability (the latter being expected to favour the former in the long term). However, these objectives can come into conflict and, as has been the case since March 2022, the Fed may have to give clear priority to reducing inflation at the risk of damaging employment and output. This refers to the concept of sacrifice ratio[1] or trade-off[2], i.e. the expected cumulative deterioration of the latter to help bring inflation back to its target (2%).

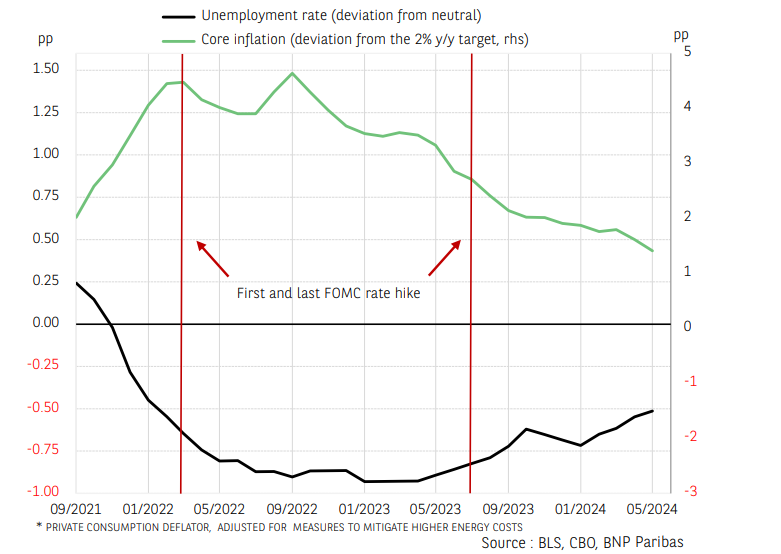

So far, the fall in inflation (-5.2 percentage points between March 2022, the start of monetary tightening, and May 2024, the latest point available) and core inflation (-3.1 pp), measured by the CPI, have gone hand in hand with a fairly contained rise in the unemployment rate (+0.4 pp over the same period, still below its neutral level according to the Congressional Budget Office). At the same time, growth remained at a robust rate of +2.5% in 2023 as an annual average and +1.3% at an annualised rate in Q1 2024.

However, changes in the unemployment rate alone provide only fragmentary information about the state of the labour market. Another relevant indicator is the participation rate of 25-54-year-olds (prime age), which has been at its highest level since 2001 (as of May 2024), while the employment rate has remained above 60% since the start of monetary tightening, despite the deterioration in the unemployment rate. The rebalancing of the labour market (in the sense of reduced hiring difficulties) has been made possible by an improvement in the supply component – which was not the Fed's central scenario – which has so far prevented the labour market and the economy from experiencing a hard landing. However, the trend in the unemployment rate is tending towards the trigger point for the Sahm Rule. The Sahm Rule links an increase of +0.5 pp in the three-month moving average of the unemployment rate at its 12-month low to a recession.

Furthermore, in a research paper[3], Robert J. Tetlow, economist and adviser to the Board of the central bank, highlights the downward pressure exerted by the anchoring of inflation expectations and the credibility of monetary policy on the level of the sacrifice ratio. However, the sacrifice ratio is still difficult to estimate and is thought to have increased over time. Yet, we have not seen any slippage in long-term (10-year) inflation expectations, as measured by the Cleveland Fed (+2.5% in May 2024), during the current cycle, despite a definite appreciation. This could be related to the firmness shown by the Federal Reserve on the need to maintain its policy at a restrictive level, even when there was a consensus within the economic community in 2023 on the upcoming occurrence of a recession.

BNP Paribas is regulated by the FSA for the conduct of its designated investment business in the UK and is a member of the London Stock Exchange. The information and opinions contained in this report have been obtained from public sources believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate or complete and it should not be relied upon as such. This report does not constitute a prospectus or other offering document or an offer or solicitation to buy any securities or other investment. Information and opinions contained in the report are published for the assistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient, they are subject to change without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein. Any reference to past performance should not be taken as an indication of future performance. No BNP Paribas Group Company accepts any liability whatsoever for any direct or consequential loss arising from any use of material contained in this report. All estimates and opinions included in this report constitute our judgements as of the date of this report. BNP Paribas and their affiliates ("collectively "BNP Paribas") may make a market in, or may, as principal or agent, buy or sell securities of the issuers mentioned in this report or derivatives thereon. BNP Paribas may have a financial interest in the issuers mentioned in this report, including a long or short position in their securities, and or options, futures or other derivative instruments based thereon. BNP Paribas, including its officers and employees may serve or have served as an officer, director or in an advisory capacity for any issuer mentioned in this report. BNP Paribas may, from time to time, solicit, perform or have performed investment banking, underwriting or other services (including acting as adviser, manager, underwriter or lender) within the last 12 months for any issuer referred to in this report. BNP Paribas, may to the extent permitted by law, have acted upon or used the information contained herein, or the research or analysis on which it was based, before its publication. BNP Paribas may receive or intend to seek compensation for investment banking services in the next three months from an issuer mentioned in this report. Any issuer mentioned in this report may have been provided with sections of this report prior to its publication in order to verify its factual accuracy. This report was produced by a BNP Paribas Group Company. This report is for the use of intended recipients and may not be reproduced (in whole or in part) or delivered or transmitted to any other person without the prior written consent of BNP Paribas. By accepting this document you agree to be bound by the foregoing limitations. Analyst Certification Each analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the analyst's personal views about any and all of the issuers and securities named in this report, and (ii) no part of the analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed herein. United States: This report is being distributed to US persons by BNP Paribas Securities Corp., or by a subsidiary or affiliate of BNP Paribas that is not registered as a US broker-dealer, to US major institutional investors only. BNP Paribas Securities Corp., a subsidiary of BNP Paribas, is a broker-dealer registered with the Securities and Exchange Commission and is a member of the National Association of Securities Dealers, Inc. BNP Paribas Securities Corp. accepts responsibility for the content of a report prepared by another non-US affiliate only when distributed to US persons by BNP Paribas Securities Corp. United Kingdom: This report has been approved for publication in the United Kingdom by BNP Paribas London Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas London Branch is regulated by the Financial Services Authority ("FSA") for the conduct of its designated investment business in the United Kingdom and is a member of the London Stock Exchange. This report is prepared for professional investors and is not intended for Private Customers in the United Kingdom as defined in FSA rules and should not be passed on to any such persons. Japan: This report is being distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited, Tokyo Branch, or by a subsidiary or affiliate of BNP Paribas not registered as a financial instruments firm in Japan, to certain financial institutions permitted by regulation. BNP Paribas Securities (Japan) Limited, Tokyo Branch, a subsidiary of BNP Paribas, is a financial instruments firm registered according to the Financial Instruments and Exchange Law of Japan and a member of the Japan Securities Dealers Association. BNP Paribas Securities (Japan) Limited, Tokyo Branch accepts responsibility for the content of a report prepared by another non-Japan affiliate only when distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited, Tokyo Branch. Hong Kong: This report is being distributed in Hong Kong by BNP Paribas Hong Kong Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas Hong Kong Branch is regulated as a Licensed Bank by the Hong Kong Monetary Authority and is deemed as a Registered Institution by the Securities and Futures Commission for the conduct of Advising on Securities [Regulated Activity Type 4] under the Securities and Futures Ordinance Transitional Arrangements. Singapore: This report is being distributed in Singapore by BNP Paribas Singapore Branch, a branch of BNP Paribas whose head office is in Paris, France. BNP Paribas Singapore is a licensed bank regulated by the Monetary Authority of Singapore is exempted from holding the required licenses to conduct regulated activities and provide financial advisory services under the Securities and Futures Act and the Financial Advisors Act. © BNP Paribas (2011). All rights reserved.

Recommended Content

Editors’ Picks

AUD/USD finally broke above 0.6700… will it last?

AUD/USD added to Tuesday’s advance and rose markedly in a context favourable to the risk-associated space following the sharp data-driven sell-off in the Greenback, while auspicious results from the domestic calendar also lent legs to AUD.

EUR/USD: Bullish outlook expected above the 200-day SMA

EUR/USD extended its multi-session recovery north of 1.0800 the figure following the persistent retracement in the US Dollar and against the backdrop of steady expectation ahead of the second round of French elections on July 7.

Gold reaches $2,360 on broad USD weakness

Gold gathers bullish momentum and trades at its highest level in nearly two weeks above $2,360. Following the disappointing ADP Employment Change and ISM Services PMI data from the US, the 10-year US yield declines sharply, helping XAU/USD extend its daily rally.

Ripple legal battle underway as on-chain metrics turn bullish, XRP eyes recovery to $0.50

Ripple made a comeback above $0.48 on Tuesday and hovers above that level in Wednesday’s European session. Ripple on-chain metrics such as transaction volume and Network Realized Profit/Loss (NPL) have turned bullish, supporting a recovery in the altcoin.

Disinflation in the United States: The scale of the sacrifice on the labour market

Since a 1977 act, the dual mandate of the Federal Reserve (Fed) has de jure entrusted it with the objectives of maximum employment and price stability (the latter being expected to favour the former in the long term).