Can Trump make volatility tremendous again?

The key event for this week will be Trump's address to Congress later this evening, 2100 ET, 0200 GMT (Wednesday). This much-anticipated speech is worth staying up for. With volatility ticking higher, but remaining at low levels, Treasury yields ticking higher and US stocks continuing to touch record levels, whether or not current trends persist is likely to depend on Trump's performance this evening.

Does an address to Congress actually mean anything?

To answer this question we need to analyse two things: firstly, what is he expected to announce, secondly, what function does this address to Congress hold? There have been some leaks about the speech. Last week the new Treasury Secretary Mnuchin said that a tax plan should be in place by August. On Monday, Trump told the National Governors' Association that his first budget will focus on keeping out terrorists and boosting spending on law enforcement. While this may play well to his supporters, we doubt it will be enough for the markets' that are greedy for signs that Trump will cut taxes and spend big during his term in office.

But this doesn't mean that Trump's speech, even if it is lacking in detail, will trigger a market sell-off. His comments on Monday that he wanted a $54BN boost to military spending helped to push the Dow Jones to a fresh record high. Although this isn't a formal State of the Union speech, it is very similar to one and it has the same function. Essentially it is the President's laundry list of wants from Congress. However, it is crucial to remember that President Trump cannot pass tax and spend laws unilaterally, he needs Congress to do this for him. President Obama could not get Congress to pass the majority of his plans, while it may be easier for President Trump to get his plans passed by a Republican Congress, it is not a given at this stage. There are some key differences between the President and some members of the Republican Congress who don't want to boost national debt levels and may not be willing to pass a big infrastructure plan even if the President mentions it on Tuesday night.

Have equity traders bought the rumour only to sell the fact?

So, where does this leave traders? We expect the markets to hang on Trump's every word, at least initially. If he does mention numbers, particularly the scale of the corporation tax cut that he wants and the size of the infrastructure programme then there could be further gains for stocks, and we may see fresh record highs on Wednesday. If he is fairly vague on the size and scale of his fiscal plans then we would expect a decline in US markets this week, however, the extent of the sell-off could depend on a few other factors.

Will Yellen have the final word?

The Fed could also bring this equity market rally to a halt. We will hear from Janet Yellen on Friday at 1800 GMT. Her reaction to Trump's speech will be critical. If Trump is vague on his fiscal plans and the stock markets sell-off, Yellen could cushion the blow by sounding cautious about the prospect for aggressive tightening from the central bank if fiscal policy isn't as loose as expected. In contrast, if Trump signals a massive fiscal boost during his term in office, then she could bring market exuberance to a dramatic halt by indicating that rates may need to rise at a faster pace in order to bring inflation expectations under control. Thus, it could end up being Trump himself who heralds the end of the "Trumpflation" rally. The prospect of fiscal largess combined with rate hikes could be the trigger for a spike higher in volatility, which tends to lead to a market decline.

Bond traders remain wary

Interestingly, ahead of the Trump speech we have seen US Treasury yields have retreated to their lowest levels of the year so far, even though they managed to rise slightly on Monday. The dollar also fell on a broad basis at the start of the week, while stocks had a mixed session, starting off on a weak note before recouping some losses. As we lead up to Trump's main event there is still a dichotomy in the markets, with Treasuries and FX acting like Trump is bound to disappoint and the Fed will not hike rates as expected, while the equity market is more optimistic on Trump's pro-growth agenda. However, maybe equity traders think they can't lose – even if Trump doesn't deliver on his pro-growth agenda the Fed will be there to cushion the blow. To put it simply, equity markets are not acting like Trump is a threat. We'll know if they are being too optimistic in about 24 hours.

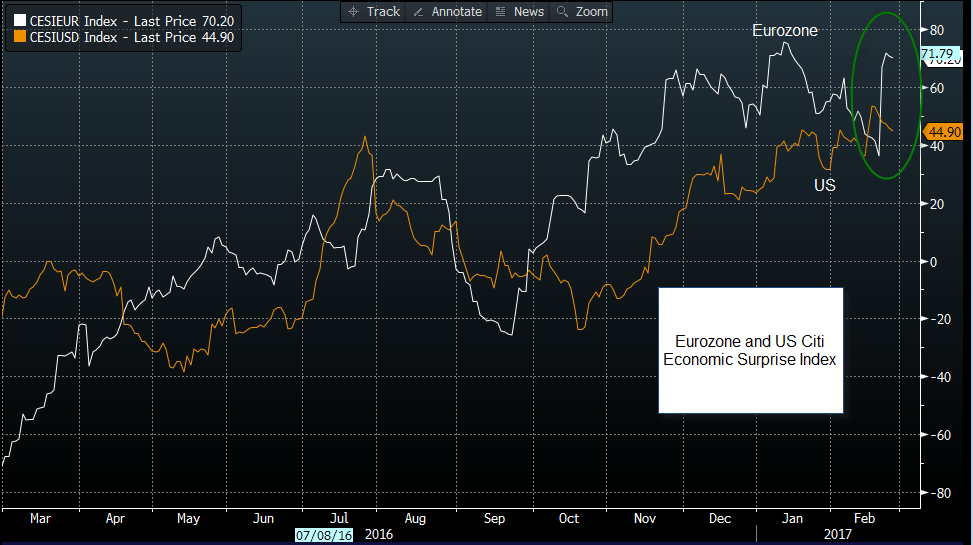

Pound still hit by Brexit risks, while euro outperforms

Elsewhere, the pound failed to recover on Monday after newspaper reports spooked the markets about an "early" Brexit and a second Scottish Independence Referendum. The euro stormed higher during Monday's trading session, and well it might. People are focusing on the political risks in Europe, which are undoubtedly a concern for 2017, but they should also look at Europe's improving economic fundamentals. The chart below shows the economic surprise index for the US and for the Eurozone, as you can see some data misses from the US has meant there have been more Eurozone positive surprises on the data front in recent days, which is helping to fuel a recovery in EURUSD, which moved above 1.06 on Monday. Could we get back to the 1.07 mid-Feb high on the back of fundamentals alone?

Overall, the market is focussed on Trump today, and aside from the second reading of US GDP we expect price action to be fairly subdued ahead of Trump's speech, although it could be the calm before the storm.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.