BoJ's rate hike sparks global market turmoil, highlights central bank influence

Outlook

Central banks are the top institution of all the institutions that can affect exchange rates, and can almost always trump any economic data. We got a stunning example of that today with the BoJ suggesting financial conditions in Japan becoming unstable and worse, infecting markets around the world.

Well, yes, unstable in the sense that the BoJ rate hike had set off a firestorm of carry trade unwinding that shoved the yen up almost 10% after hitting a multi-decade low in July. The FT suggests that exiting the yen had sent cash to the tech sector in the US via index following.

The FT quotes a Japanese analyst: “The Nikkei has essentially gone back to where it started in 2024, prior to the market rise which was driven by a combination of US monetary easing prospects and ‘higher for longer’ US interest rates,” said Naoki Kamiyama, chief strategist at Nikko AM.

“’We need to keep in mind that the downturn in Japanese equities was seen to be led in part by macro trend-following index players . . . The downturn they induced could eventually pave the way for others, notably retail investors, to tiptoe into the market once volatility shows signs of settling down.’”

Morgan Stanley tries to insert looming US recession into the mix, but it’s not needed—the developments in the yen suffice.

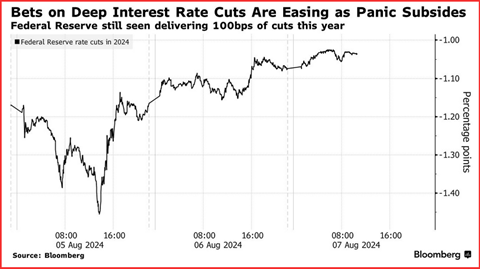

Turning to the US, Reuters reports “Most notable among a series of hastily revised forecasts, U.S. investment bank JPMorgan now projects that we will see two half-point cuts in both September and November, followed by a quarter-point cut in December.

“Not for the first time, this may seem a little overcaffeinated. And it certainly reflects the market volatility present right now in a holiday-thinned August.

But what's happened further out the curve is perhaps more instructive about what investors expect to see in the full easing cycle ahead…. But where the cutting stops is less obvious.

“Looking at futures and money market pricing on Monday, the so-called terminal rate over the next 18 months never got below 2.85%, even during the most extreme part of the day's turbulence. That's a long way down from the current policy mid-rate of 5.38%.

“But it's still above where Fed policymakers see the long-term 'neutral' rate - widely seen as their proxy for the fabled 'R*' rate that neither stimulates or reins in economic activity. That median long-run rate is currently 2.8% - after being pushed up 30 basis points by Fed officials this year.

“So, if anxious money markets don't think the Fed will be forced to go below that, then the slowdown ahead can't be expected to be that bad - despite all the hand wringing of recent days. At the very least, it suggests markets remain equivocal about recession and think the removal of policy 'restriction' may be enough by itself to hold the line.”

Sensibility, at last. Amid the upcoming data on the thin agenda, we wonder if the usual Thursday jobless claims might be a trigger back to normalcy.

Forecast

Just as an “emergency” Fed rate hike was always a silly idea, the market persists in expecting far too many and too big a series of rate cuts. These expectations are driving yields down and taking the dollar with them, with a feedback loop along the lines of yields are the epitome of risk judgment and if they are falling, risk must be rising.

As noted above, the market is pricing in a good 100 bp of cuts this calendar year, which sensible folks must see as wildly overdone. The most that would be “normal” is 25 bp per meeting, and there are only three meetings left in the year.

A 50 bp at one of the meetings would signal panic at the Fed, and the Fed goes far out of its way to avoid the appearance of panic. And it was only a week or so ago that Mr. Powell said the Fed is still cautious about incoming data needing to validate the expectation of a cut in September.

Once the markets decide that 100 bp is not gonna happen, yields can relax and the dollar can recover. Keep the faith. This may take a while.

Political Tidbit: The Harris choice for vice president was not the guy we bet on. And while the press and public like Walz, the gov of Minnesota and former high school teacher, football coach and Army reservist, we thought he was too 1950’s.

But it doesn’t matter whether we like the Dem ticket. The point of this election is to demonstrate overwhelmingly that the US rejects Trump, like the rest of the world except a few dictators. He is a fraudster, a liar, a felon, a racist and sexist, mentally unstable and entirely unfit to represent the US.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat