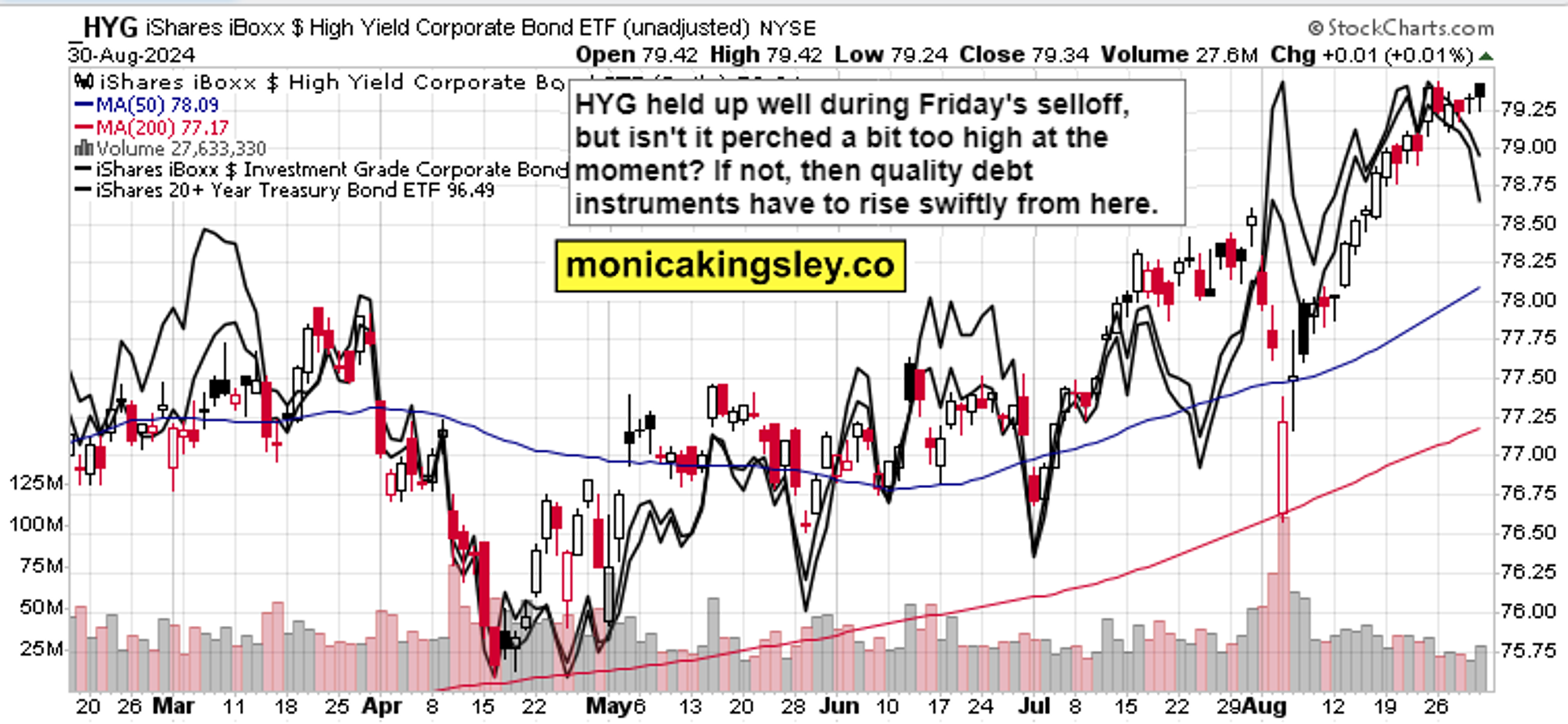

Why sudden risk-off

S&P 500 ascent to well below my key level given to clients was rejected soon after the opening bell, already in the low 5,640s – core PCE in line with expectations wasn‘t good enough reason to bid equities higher. Chicago PMI at 46 is a marginal improvement on the prior reading as the economy remains mired in manufacturing recession for two good years already.

Tired rise in the dollar and yields represents an underappreciated risk – risk of a recession to the soft landing consensus – as the Fed‘s focus is to turn from inflation to the weakening job market. There was the Jackson Hole victory lap, disinflation continues, and also Friday‘s UoM inflation expectations were revised lower to only 2.8%.

With unemployment claims well below the psychological 250K level, there isn‘t enough attention paid to rising continuing claims – and the 2024 revision of job creation to the tune of 818K was earlier shrugged off very fast in the markets. No fear of earnings or consumer strength, discretionaries continue recovering, and S&P 500 is being led by financials amid continuing tech underperformance.

With global easing ahead and ongoing, the medium-term path in equities is higher (appreciation of interest rate sensitive plays talked ever since Jul CPI, is to be rewarded (nevermind the slow housing data, all eyes on… clients know) – be watching the Jul peak), but hard landing fear (recession fear) carries the greatest short-term setback potential to S&P 500.

It‘s „what if the Fed is cutting not because inflation is under control and declining, but because the outlook of the economy and job market is worse than we the traders and investors appreciate them to be“?

And this macroeconomic slash fundamental risk (hello AI trade that‘s still getting second look following NVDA beat, SMCI filing reworking that was though kind of waved off as not material Friday, and indirectly as well via Bitcoin not yet surging on the liquidity galore ahead) is what I‘m sharing with clients in search of best places on the long side.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.