Key points

-

Trump’s victory fuels market confidence: The Red Sweep in the US elections has helped to clear uncertainty, fueling optimism in sectors like financial services, defense, and small-caps, especially regional banks.

-

China’s stimulus disappoints: The 10 trillion yuan debt relief package offers stability but falls short of boosting consumption and the property market, dampening near-term market optimism.

-

Equity rotation: The market is shifting beyond tech dominance, with small-cap stocks and cyclical sectors benefiting from pro-growth policies, though earnings growth remains a key factor to watch especially for the small-cap space.

-

Earnings focus: Investors will watch Disney’s Q4 report on streaming and theme parks, while Home Depot faces pressure from high interest rates and consumer uncertainty.

US elections: Trump victory clears path for pro-growth policies

Election outcome clears uncertainty: Trump’s sweeping victory across swing states removes election uncertainty, creating a smoother path for market confidence. Though some House races remain uncalled, a Red Sweep appears likely, strengthening expectations for policy continuity and economic support.

Focus on pro-growth policies: Investors anticipate Trump’s tax cuts and deregulatory stance, which underscore U.S. market resilience and exceptionalism. Sectors benefiting from his agenda, particularly those tied to domestic growth and smaller-cap companies, are already seeing gains. The financial services sector stands out, with regional banks spiking 10% on hopes of regulatory relaxation, lower capital requirements, and a friendlier M&A landscape. For an in-depth discussion on which sectors and stocks were the winners and loser in the aftermath of the US elections and what it means for Big Tech, read this article.

Fiscal risks and inflation watch: The other side of this growth-focused agenda is rising fiscal pressure. Extending current tax cuts could push deficits up by an estimated $5 trillion by 2034, driving national debt further above 100% of GDP. Additionally, any tariff escalations or tightened immigration policies could add inflationary pressures, particularly concerning after recent inflationary years. Investors will be closely watching the U.S. CPI report on Wednesday; a stronger-than-expected reading could challenge the Fed’s dovish pivot, potentially pointing to a shallower rate cut cycle.

Equity rotation: Small-cap stocks shine, but can it last?

Growth vs. inflation outlook: Despite expectations of a gradual easing cycle from the Fed, strong U.S. economic growth is expected to support corporate earnings, keeping stocks in play. With S&P 500 earnings forecast to accelerate from 0.5% in 2023 to 9% in 2024 and 14% in 2025, risk-reward for equities remains tilted higher.

Broadening leadership: Since Q3, the market has shifted beyond its tech-heavy leadership, with value stocks, cyclical sectors, and small- and mid-cap stocks now gaining momentum. With potential tax cuts and deregulation on the table, this could add fuel to the rally. Key Trump Trade themes of reshoring, defense and domestic production could mid-cap U.S. stocks and industrials could remain well-positioned.

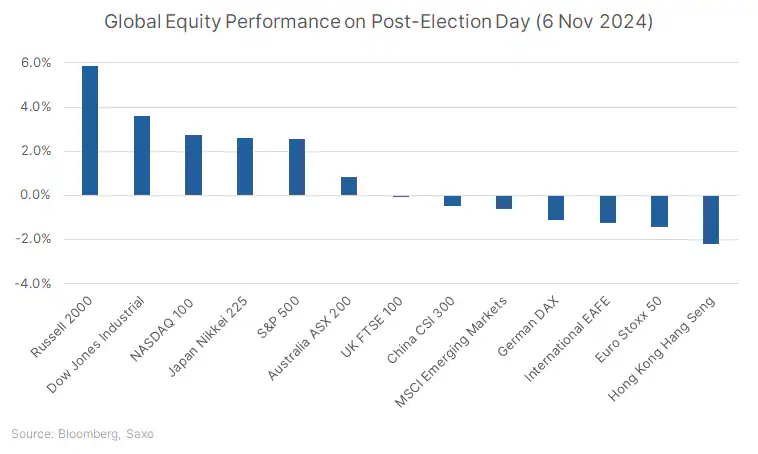

Can the small-cap rally be sustained? The Russell 2000 small-cap index jumped 8.5% last week to all-time highs, outperforming the S&P 500 (+4.7%) and NASDAQ 100 (+5.4%). However, this rally could face obstacles due to weak earnings growth, with nearly 40% of Russell 2000 companies unprofitable. It’s crucial to be selective, with focus on small-caps that show strong financial health. For a complete primer on the small-cap Russell 2000 index, read this article.

International risks: Risks like trade tensions and a potentially stronger dollar could hinder international equities. As such, underweighting developed-market international stocks and instead positioning for relative strength within U.S. markets could be attractive in this environment. Emerging market themes are likely to be more nuanced. Countries exposed to tariffs may struggle, while those driven by domestic demand, like India, or benefiting from supply chain shifts, like Vietnam, could see stronger performance.

China’s stimulus misses the mark: What it means for investors

Debt relief package unveiled: China's National People’s Congress approved a 10 trillion yuan ($1.4 trillion) debt swap package to help local governments refinance hidden debts, extending relief funding through 2028. This move aims to ease immediate debt repayment pressures and reduce servicing costs, allowing local governments greater budget flexibility to pursue growth targets.

Limited boost to growth: While the debt relief offers stability, Friday’s announcement lacked additional fiscal stimulus to support China’s sluggish consumption and struggling property market. This conservative approach, some speculate, could signal that Beijing is conserving resources in anticipation of potential anti-China measures under Trump’s administration.

Market reaction muted: With fiscal measures at the low end of expectations, Chinese markets are showing caution. Although officials have pledged deeper fiscal spending in 2025, the immediate lack of stimulus may curb optimism in the near term. Investors are on alert for further policy actions and tech earnings are a key focus this week, but more importantly any China-related headlines from the Trump administration could add to market volatility.

Earnings in Focus: Chinese tech giants Tencent, Alibaba, and JD.com report earnings this week, which could set the tone for sentiment in China’s tech sector amid this policy uncertainty.

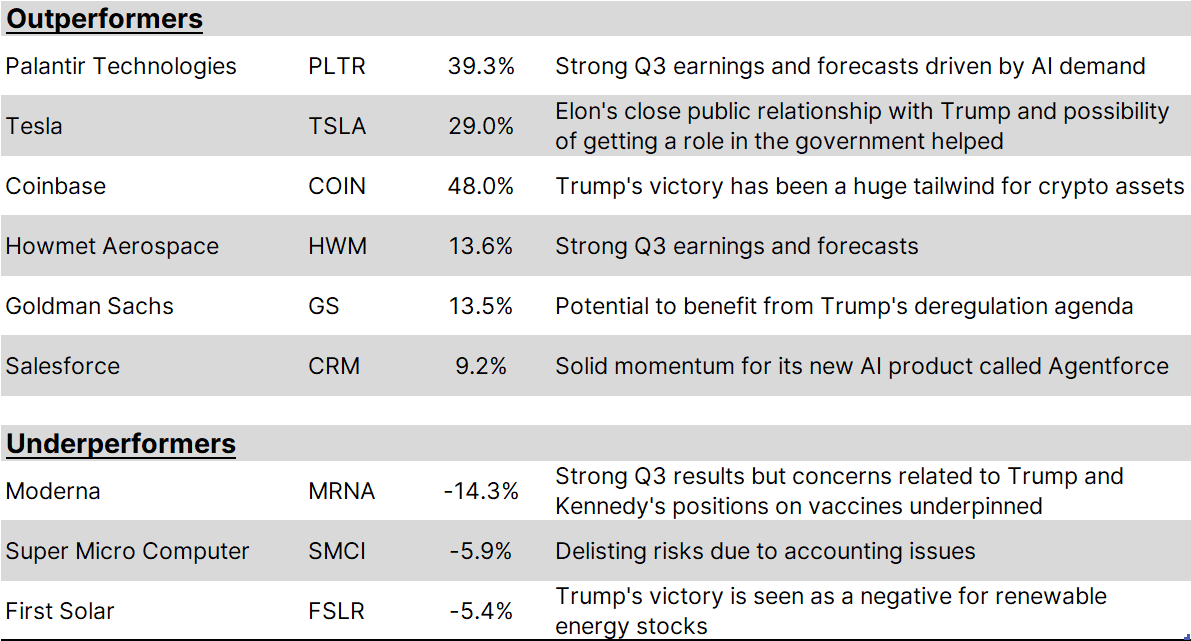

Market movers: Key stock outperformers and underperformers

Source: Saxo

Earnings to watch: Disney and Home Depot

As we approach the tail end of Q3 earnings season, two high-profile companies are set to report: Disney on Thursday and Home Depot on Tuesday.

- Disney preview: Disney’s upcoming Q4 earnings report on November 14 will capture investor attention, with a focus on the performance of Disney+ streaming, theme parks, and CEO Bob Iger’s succession plans, set for 2026. The streaming segment shows profit growth, aided by potential price hikes, and the ESPN streaming service launching in 2025 could further support this trend. However, theme park results may be under pressure due to recent disruptions like the Shanghai closure, the Paris Olympics, and Hurricane Helene. Rising operational costs tied to Disney Cruise Line’s pre-launch activities also pose headwinds. Consensus forecasts for Q4 are as follows:

-

Revenue: $22.45 billion (vs. $23.16 billion in Q3).

-

EPS: $1.10 (vs. $1.39 in Q3).

-

- Home Depot Preview: The home improvement giant could face further pressure from high interest rates and ongoing consumer uncertainty. Consensus forecasts for Q3 FY2025 are as follows:

-

Revenue: $39.2 billion (vs. $43.2 billion in Q2).

-

EPS: $3.66 (vs. $4.67 in Q2).

-

Read the original analysis: Weekly stock spotlight: Trump victory propels small-cap surge and US outperformance

The Saxo Bank Group entities each provide execution-only service and access to Analysis permitting a person to view and/or use content available on or via the website. This content is not intended to and does not change or expand on the execution-only service. Such access and use are at all times subject to (i) The Terms of Use; (ii) Full Disclaimer; (iii) The Risk Warning; (iv) the Rules of Engagement and (v) Notices applying to Saxo News & Research and/or its content in addition (where relevant) to the terms governing the use of hyperlinks on the website of a member of the Saxo Bank Group by which access to Saxo News & Research is gained. Such content is therefore provided as no more than information. In particular no advice is intended to be provided or to be relied on as provided nor endorsed by any Saxo Bank Group entity; nor is it to be construed as solicitation or an incentive provided to subscribe for or sell or purchase any financial instrument. All trading or investments you make must be pursuant to your own unprompted and informed self-directed decision. As such no Saxo Bank Group entity will have or be liable for any losses that you may sustain as a result of any investment decision made in reliance on information which is available on Saxo News & Research or as a result of the use of the Saxo News & Research. Orders given and trades effected are deemed intended to be given or effected for the account of the customer with the Saxo Bank Group entity operating in the jurisdiction in which the customer resides and/or with whom the customer opened and maintains his/her trading account. Saxo News & Research does not contain (and should not be construed as containing) financial, investment, tax or trading advice or advice of any sort offered, recommended or endorsed by Saxo Bank Group and should not be construed as a record of our trading prices, or as an offer, incentive or solicitation for the subscription, sale or purchase in any financial instrument. To the extent that any content is construed as investment research, you must note and accept that the content was not intended to and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such, would be considered as a marketing communication under relevant laws.

Recommended content

Editors’ Picks

EUR/USD stays near 1.0400 in thin holiday trading

EUR/USD trades with mild losses near 1.0400 on Tuesday. The expectation that the US Federal Reserve will deliver fewer rate cuts in 2025 provides some support for the US Dollar. Trading volumes are likely to remain low heading into the Christmas break.

GBP/USD struggles to find direction, holds steady near 1.2550

GBP/USD consolidates in a range at around 1.2550 on Tuesday after closing in negative territory on Monday. The US Dollar preserves its strength and makes it difficult for the pair to gain traction as trading conditions thin out on Christmas Eve.

Gold holds above $2,600, bulls non-committed on hawkish Fed outlook

Gold trades in a narrow channel above $2,600 on Tuesday, albeit lacking strong follow-through buying. Geopolitical tensions and trade war fears lend support to the safe-haven XAU/USD, while the Fed’s hawkish shift acts as a tailwind for the USD and caps the precious metal.

IRS says crypto staking should be taxed in response to lawsuit

In a filing on Monday, the US International Revenue Service stated that the rewards gotten from staking cryptocurrencies should be taxed, responding to a lawsuit from couple Joshua and Jessica Jarrett.

2025 outlook: What is next for developed economies and currencies?

As the door closes in 2024, and while the year feels like it has passed in the blink of an eye, a lot has happened. If I had to summarise it all in four words, it would be: ‘a year of surprises’.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.