Here is what you need to know on Thursday, July 14:

The equity market held up well on Wednesday after the CPI number also held up well. In truth, the CPI number was shockingly high, coming in well above expectations on both metrics. Equities reacted as you would expect on the number with the Nasdaq and S&P 500 falling about 2% in the ten minutes after the release. From then on a counterintuitive rally ensued, and the main indices more or less ended the day flat.

Bond yields ticked up but not dramatically so. Money markets have moved to price in a near certainty now of a 100-basis-point hike from the Fed in July. The Bank of Canada may have made their job easier by leaking the possibility essentially when they did their own 100 bps hike. Now Fed funds futures are pricing an 84.5% chance of a 100 bps hike in July. Last week that probability was dead zero, and a 75-basis-point hike was at 99%. The bond market has been caught off guard again, and the 2-year/10-year yield curve inverted further into negative territory and is following on in the same vein this morning.

US 10Y-US 2Y yield curve

Corporate earnings season is up and running now with JPMorgan and Morgan Stanley both missing on top and bottom lines. JPMorgan increased provisions for bad debts, and Morgan Stanley said it was hit by reduced investment banking revenue. JPMorgan CEO Jamie Dimon reiterated his comments from a few weeks ago when he said he sees a hurricane coming for the US economy. This is the start of earnings deterioration we have been speaking of in our weekly preview articles now for some time. This will be the next leg lower for equities. Analyst forecasts are way too high and need to come down by 20% on average for S&P 500 earnings.

Back to inflation, the so-called reasoning behind Wednesday's move was the fact that the far end of the curve is flattening as the US will enter recession by 2023 and the Fed will pivot and cut rates. Exactly why this is good news is bizarre to me, but that argument has already been questioned by the PPI report just out showing another surge in input prices. Inflation was transitory, they said, then it was demand-led. Well, that seems unlikely in my view.

The dollar remains kingpin as the euro remains a basket case, while Italy looks to join the UK in ditching its leader. The dollar index is at 108.78 now. Gold is lower at $1,710, and oil is much lower on recession fears, back to $94 now. Bitcoin yet again clings to $20,000.

European markets are lower: Eurostoxx: -1.7%, FTSE -1.5% and Dax -1.5%.

US futures are also lower: S&P -1.2%, Dow -1.4% and Nasdaq -0.8%.

Wall Street top news (QQQ) (SPY)

PPI 11.3% versus 10.7% expected.

Money markets price in more rate hikes globally, Fed 100 bps now at over 80% probability.

JPMorgan (JPM) misses EPS and revenue.

Morgan Stanley (MS) also misses top and bottom lines.

Netflix (NFLX) picks Microsoft (MSFT) to help with its advertising platform.

Taiwan Semiconductor (TSM) beats on revenue and EPS.

Ericsson (ERIC) misses earnings on strong component costs. Read across for many tech companies.

Twitter (TWTR) rises on lawsuit versus Elon Musk.

Conagra (CAG), food producer, defensive stock, says margins are shrinking. Earnings in line.

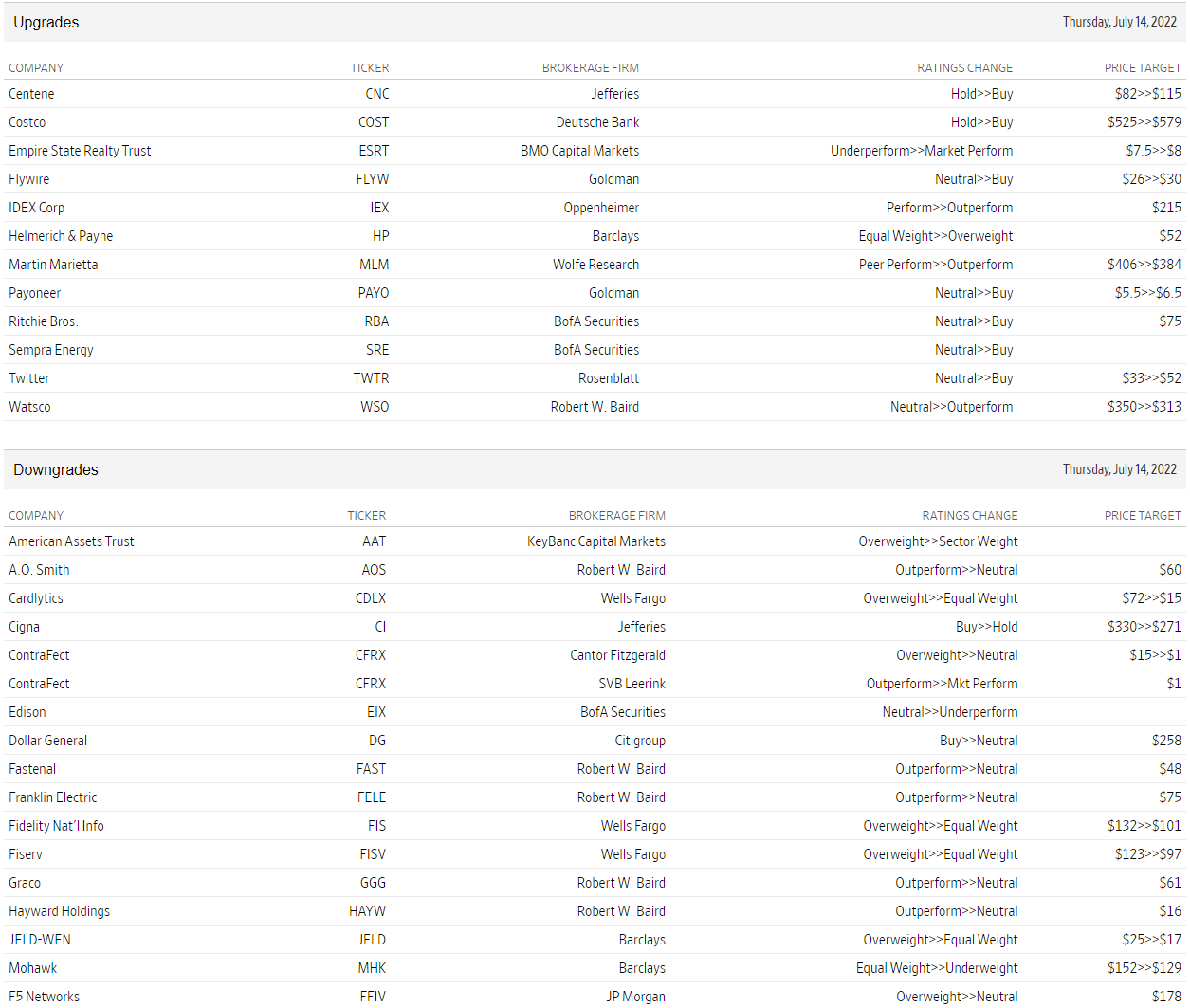

Upgrades and downgrades

Source: WSJ.com

Economic releases

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

Gold holds the record run to near $3,500

Gold price retreats slightly from near $3,500, or a fresh all-time highs in the early European session on Tuesday as bulls pause for a breather amid overbought conditions on short-term charts. Any meaningful corrective downfall, however, still seems elusive on sustained US Dollar weakness.

EUR/USD stays firm near 1.1550 as US Dollar wilts again

EUR/USD extends its gains for the third successive session, holding higher ground near 1.1550 in ealy Europe on Tuesday. The pair catches a fresh bid as the US Dollar comes under fresh selling pressure as investors remain wary of the US financial stability amid Trump's attacks on Fed Chair Powell.

GBP/USD recaptures 1.3400 on renewed US Dollar weakness

GBP/USD is back above the 1.3400 mark in the European trading hours on Tuesday, drawing support from a renewed bout of US Dollar selling across the board. Fears of a US economic slowdown and concerns about the Fed's independence remain a weight on the US Dollar, serving as a tailwind for the major.

3% of Bitcoin supply in control of firms with BTC on balance sheets: The good, bad and ugly

Bitcoin disappointed traders with lackluster performance in 2025, hitting the $100,000 milestone and consolidating under the milestone thereafter. Bitcoin rallied past $88,000 early on Monday, the dominant token eyes the $90,000 level.

Five fundamentals for the week: Traders confront the trade war, important surveys, key Fed speech Premium

Will the US strike a trade deal with Japan? That would be positive progress. However, recent developments are not that positive, and there's only one certainty: headlines will dominate markets. Fresh US economic data is also of interest.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.