Here is what you need to know on Friday, June 25:

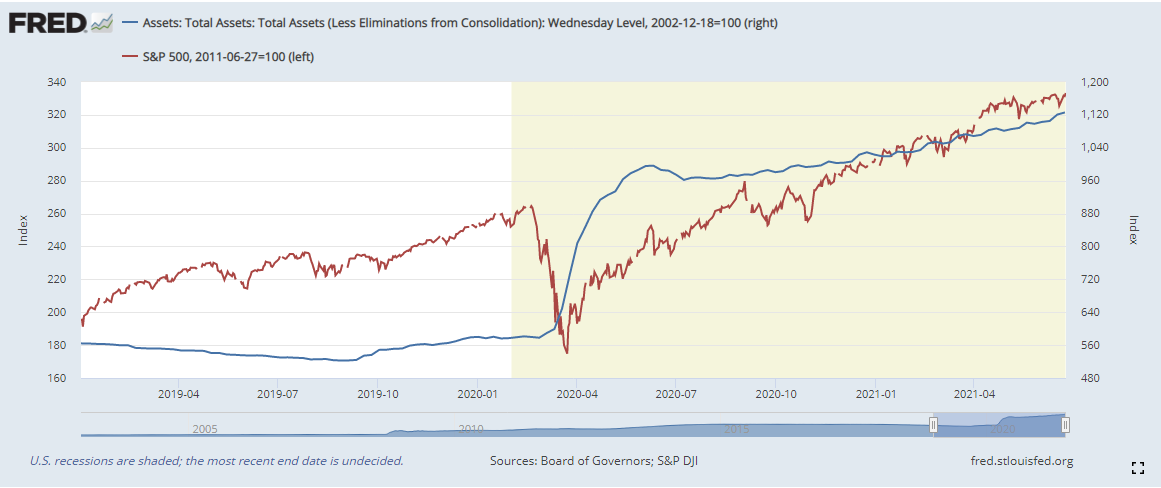

Equity markets continue to set more and more records as 2021 progresses with any dip in danger of being devoured by hungry buyers. The Fed wobble from last Thursday and Friday set up the latest dip and sure enough record highs swiftly followed. The Fed's balance sheet hit another record high keeping the strong correlation in place, the Fed being the lead indicator. The chart below shows the correlation and note that the Fed balance sheet hit a record high again last week.

Mega tech continues to drive higher with Facebook (FB) and Alphabet (GOOGL) both at or near record highs on Thursday, while Tesla continues its breakout (see more) and Apple also breaks higher, see here.

The dollar remains steady at 1.1950 versus the euro, Oil is flat at $73.30, Bitcoin lower by 4% at $33,200 and Gold is $1,788. The fear guage VIX and yields are lower. The VIX is at 16 while the 10-year yield slumbers at 1.49% despite the high PCE data. PCE Core highest since 2008, PCE index highest since 1990's!

European markets are mixed but largely around flat, FTSE +0.1%, Dax -0.1% and EuroStoxx -0.2%.

US futures are flat for S&P and Nasdaq, while the Dow is up 0.3%.

Wall street top news

US consumer spending 0.0% versus expected 0.4%.

US PCE Price Index, Core +0.5% versus forecast +0.6%.

University of Michigan Sentiment is due at 1500 GMT/1000 EST.

Delta variant of Covid continues to become the dominant strain as governments and countries ponder delays to reopening strategies. Israel, the world's most vaccinated country, sees cases quadruple as it reintroducess mask guidance.

US Senate leader Mitch McConnell says he is pessimistic on the infrastructure bill after President Biden's comments.

Germanys Economic Minister says expected to reach an agreement between EU and US over steel tariffs by end of 2021.

Virgin Galactic (SPCE) looks like being the first stock to the moon (sorry AMC and GameStop) as it receives FAA ok to fly passengers to space. Up 15% premarket.

Nike (NKE) keeps going in premarket after last night's numbers, up 12% as EPS but in particular guidance beat estimates.

FedEx (FDX) EPS $5.01 just ahead of forecast, revenue also ahead. CEO says can't find enough workers though so the stock drops 3% in premarket. You'll hear this a lot.

CarMax (KMX) EPS beats, shares up 6% premarket.

FootLocker (FL) and UnderArmour (UA) up 4% in premarket, most likely dragged up by Nike (NKE).

Logitech (LOGI) downgraded by Goldman. Drops 3% premarket.

Netflix (NFLX) upgraded by Credit Suisse. Up 2% premarket.

Blackberry (BB) meme name down 3% premarket as reports better than expected loss and higher revenue than forecast on Thursday but Canaccord and CIBC downgrade on Friday.

Bank stocks (JPM, BAC, C) pass Fed stress tests meaning they can resume buybacks and dividends. CNBC.

Nokia (NOK) Godman upgrades, up 3% premarket.

NetApp (NTAP) Raymond James upgrades, stock up 3% premarket.

Upgrades, downgrades, premarket movers

Source: Benzinga Pro

Economic releases

Like this article? Help us with some feedback by answering this survey:

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

EUR/USD struggles to hold above 1.0400 as mood sours

EUR/USD stays on the back foot and trades slightly below 1.0400 following the earlier recovery attempt. In the absence of high-tier data releases, the negative shift seen in risk mood helps the US Dollar gather strength and forces the pair to stretch lower.

GBP/USD declines toward 1.2500 on renewed USD strength

GBP/USD loses its traction and declines to the 1.2500 area in the second half of the day on Monday. The US Dollar (USD) benefits from safe-haven flows and weighs on the pair as investors await US Consumer Confidence data for December.

Gold drops below $2,620 as US bond yields edge higher

After starting the week in a quiet manner, Gold comes under bearish pressure and retreats below $2,620. The benchmark 10-year US Treasury bond yield stays in positive territory above 4.5%, making it difficult for XAU/USD gain traction.

Bitcoin fails to recover as Metaplanet buys the dip

Bitcoin hovers around $95,000 on Monday after losing the progress made during Friday’s relief rally. The largest cryptocurrency hit a new all-time high at $108,353 on Tuesday but this was followed by a steep correction after the US Fed signaled fewer interest-rate cuts than previously anticipated for 2025.

Bank of England stays on hold, but a dovish front is building

Bank of England rates were maintained at 4.75% today, in line with expectations. However, the 6-3 vote split sent a moderately dovish signal to markets, prompting some dovish repricing and a weaker pound. We remain more dovish than market pricing for 2025.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.