US Dollar Index looks for direction around 91.80

- DXY alternates gains with losses around 91.80.

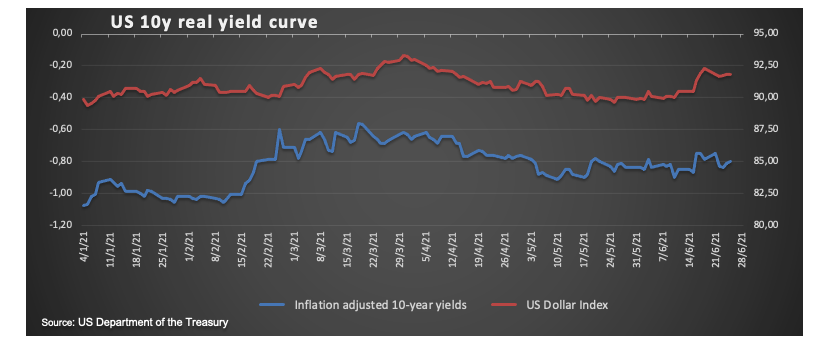

- US 10-year yields stay side-lined above the 1.50% level.

- The Dallas Fed Index, Fedspeak come next in the docket.

The greenback starts the week on a choppy fashion and motivates the US Dollar Index (DXY) to trade without clear direction in the 91.80 region.

US Dollar Index looks to yields, data

The index remains within a consolidative mood on Monday, always against the backdrop of flat US yields and rising cautiousness ahead of key data releases later in the week.

Indeed, yields of the key US 10-year note manage to keep business above the 1.50% level so far, gaining a couple of bps from last week’s trading range.

In the meantime, investors are expected to keep tracking the debate between higher inflation, the Fed’s (still) dovish stance and prospects of tapering in the shorter-than-anticipated horizon. Additionally, recent results from the Consumer Sentiment (Friday) came in lower than forecast and fell in line with some loss of momentum in the US docket as of late, which could also be limiting the upside potential in the buck.

Data wise in the US calendar, the Dallas Fed Manufacturing Index will be the sole release on Monday. In addition, NY Fed J.Williams (permanent voter, centrist) and FOMC’s R.Quarles (permanent voter, centrist) are due to speak later in the NA session.

What to look for around USD

The dollar remains supported by the key 200-day SMA so far, always amidst the recent consolidation below the 92.00 yardstick and the muted performance of YS 10-year yields. The likeliness that the tapering talk could kick in before anyone had anticipated and a potential rate hike in H2 2022 fuelled the sharp bounce in the buck post-FOMC event to levels last seen in mid-April and at the same time introduced some uncertainty into the debate surrounding the extension of the “transient” inflation. The strong upside in DXY was also supported by higher yields in the shorter end of the curve, which in turn widened the spread differential vs. their German peers. In the meantime, further progress on the reopening of the economy, the vaccine rollout and results from key fundamentals remain key for the dollar’s price action/sentiment in the short-term horizon.

Key events in the US this week: House Price Index, Conference Board’s Consumer Confidence (Tuesday) – MBA Mortgage Applications, ADP Report, Pending Home Sales (Wednesday) – Initial Claim, ISM Manufacturing PMI, Markit’s June final Manufacturing PMI (Thursday) – Nonfarm Payrolls, Unemployment Rate, Balance of Trade, Factory Orders (Friday).

Eminent issues on the back boiler: Biden’s plans to support infrastructure and families, worth nearly $6 trillion. US-China trade conflict under the Biden’s administration. Tapering speculation vs. economic recovery. US real interest rates vs. Europe. Could US fiscal stimulus lead to overheating?

US Dollar Index relevant levels

Now, the index is losing 0.08% at 91.74 and faces the next support at 91.51 (weekly low Jun.23) followed by 91.13 (100-day SMA) and finally 89.53 (monthly low May 25). On the other hand, a breakout of 92.40 (monthly high Jun.18) would open the door to 92.46 (23.6% Fibo level of the 2020-2021 drop) and finally 93.43 (2021 high Mar.21).

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.