US Dollar Index clings to daily gains near 95.70

- The index adds to Friday’s post-Payrolls gains near 95.70.

- Yields of the US 10-year note in session highs around 2.70%.

- US Factory Orders will be the sole release today.

The US Dollar Index (DXY), which tracks the greenback vs. its main rivals, is posting gains for another session and is testing the 95.70 region so far, or daily highs.

US Dollar Index looks to data

The index is clinching its third consecutive daily advance so far on Monday, as markets continue to adjust to the recently published releases in the US docket.

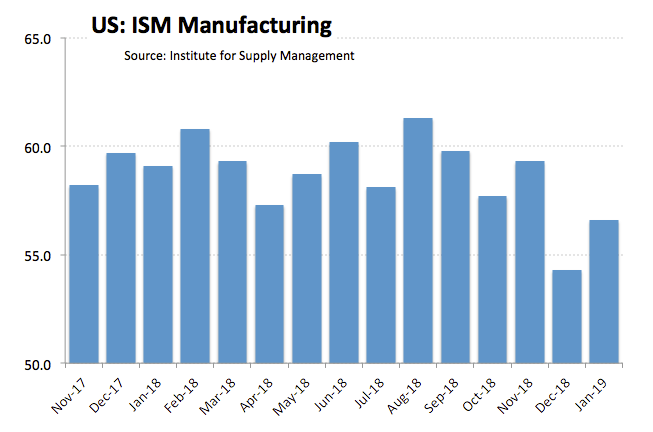

It is worth recalling that January’s Non-farm Payrolls came in above expectations at 304K, the ISM manufacturing ticked higher to 56.6 and US Consumer Sentiment improved to 91.2. On the not-so-bright side, inflation pressures tracked by Hourly Average Earnings expanded at a monthly 0.1%, disappointing estimates.

Data wise today, Factory Orders for the month of November will be the sole publication.

What to look for around USD

The greenback appears to have left behind the recent dovish message from the FOMC at its last meeting. However, investors are expected to remain vigilant on the new neutral stance from the Federal Reserve, as well as any indication of the timing of the balance sheet run-off. In addition, President Trump and China’s Xi Jinping will meet again later in the month amidst the recent improvement in the sentiment surrounding these negotiations.

US Dollar Index relevant levels

At the moment, the pair is up 0.06% at 95.68 and a breakout of 95.76 (50% Fibo of the September-December up move) would open the door to 95.85 (21-day SMA) and finally 95.98 (high Jan.30). On the downside, immediate contention emerges at 95.33 (200-day SMA) followed by 95.16 (low Jan.31) and then 95.03 (2019 low Jan.10).

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.