US dollar: A bearish false start?

- The US dollar index, DXY, is under pressure below two levels of critical daily support.

- The markets will be looking to the BoC, RBA and ECB for clues of sustainable convergence with the Fed.

The market has fallen out of love with the US dollar due to the prospects of the European Central Bank and others playing catch-up with the Federal Reserve.

The Federal Reserve is expected to announce that it will begin to taper its quantitative easing programme.

Most economists were expecting an announcement to come this fall, potentially as soon as the Federal Reserve interest rate decision and Federal Open Market Committee meeting later this month.

However, following a series of events, including the biggest caveats to the taper, being the Jackson Hole and Nonfarm Payrolls, bets of an imminent taper have been dialled all the way back.

The Federal Reserve's chairman, Jerome Powell, explained at the Jackson Hole that while the Fed has probably got to the point where “substantial further progress” has been made on inflation “we have much ground to cover to reach maximum employment”.

The chairman was referring to tapering at a time when the FOMC is satisfied that the jobs market is firmly on the way to maximum employment.

Since then, we have had two dismal reports in the ADP and the NFP data last week among a series of other less than satisfactory data.

August Nonfarm Payrolls rose just 235k versus expectations for around three times that.

Other disappointing data on Friday showed that the August ISM services index fell to 61.7 vs 64.1.

''US payrolls data clearly showed that the spread of the Delta variant is having an impact on hiring for customer-facing jobs and played into expectations that the Fed will not formally announce its tapering intentions until November at the earliest,'' analysts at ANZ Bank explained.

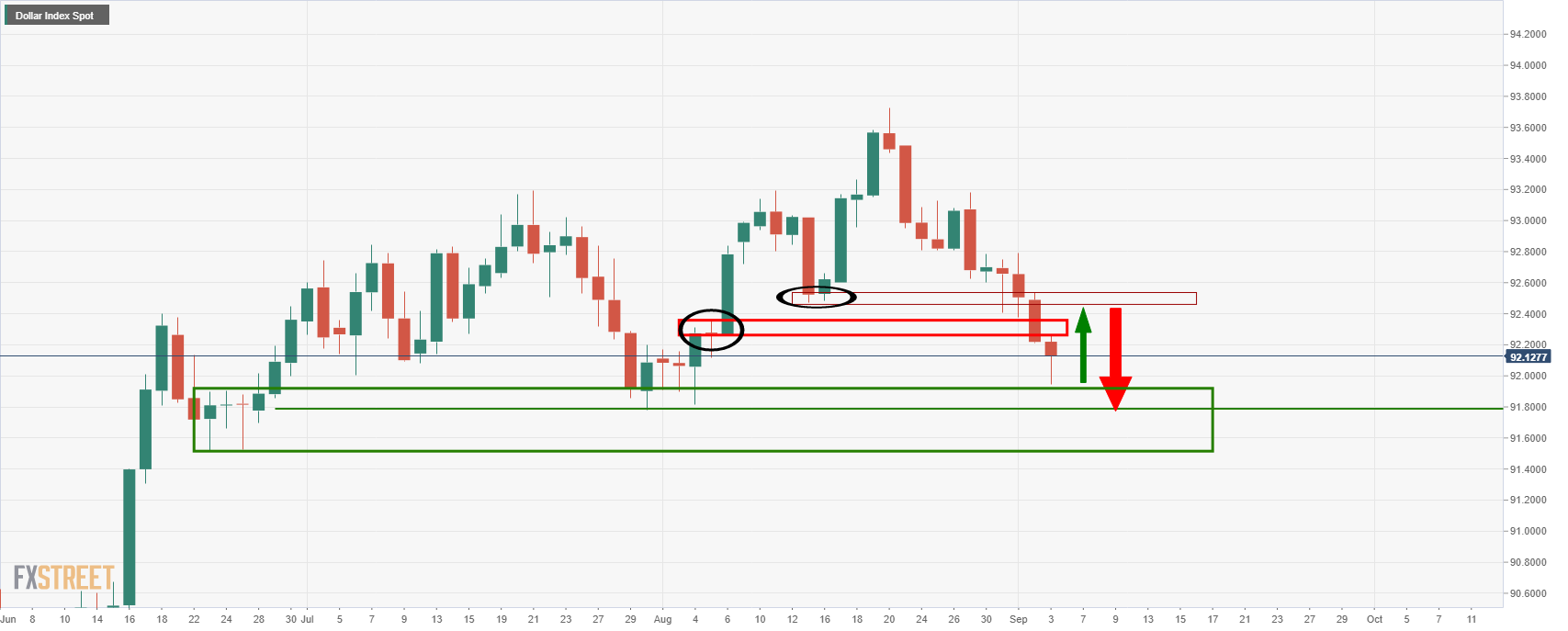

Consequently, the DXY slid to the lowest levels since the start of August:

A bearish false start?

However, the question is whether the bears have jumped the gun?

First and foremost, the NFP report, while terrible, was only one of many other very strong reports.

If there are signs that the Delta variant is coming back under control and should consumer confidence lift, this could just be a temporary glitch in the jobs market's recovery towards maximum employment.

After all, and as the analysts at ANZ Bank point out, ''the three-month average of payrolls growth is an impressive 750k.''

Markets may pause and reflect on this at the start of the week and wait for further evidence that the US economic recovery is under threat from the spread of the highly contagious variant.

''We don't think the report is weak enough for Fed officials to back away from their "this year" tapering signal, especially given the continued strength in wages, but we believe it increases the probability of a formal announcement coming at the Dec rather than the Nov meeting,'' analysts at TD Securities argued.

Other central banks that have already begun to taper, such as the Bank of Canada, or central banks that are on the verge of tapering, such as the Reserve Bank of Australia, potentially set on starting its tapering programme as soon as this month, are exposing the greenback to a long squeeze.

However, the US is not the only economy exposed to the risk of the delta spreading. It all goes back to relative performances.

The US dollar may hold up better than expected since a US recession would likely be part of a broader global downturn.

''However, caution in policy deliberations will prevail,'' the analysts at ANZ Bank argued.

''The release of the Beige Book this week will be important in gauging business sentiment and activity.''

''The next question is how the economy performs in the aftermath of next week’s benefits cliff when supplementary unemployment insurance support ends in all US states.''

''The Fed faces a tricky navigation between the labour market, growth and inflation.''

All eyes on Europe

The markets will now be keen to compare the economic performance in Europe to that of the US in order to gauge what might be coming next from the European Central Bank.

Rising inflation pressures have led some to below that the ECB will be seeking to address their own QE and the tide could be going out in this respect for the greenback.

The market tends to weigh the US dollar to a basket of currencies for which the euro is its main peer, to come 58% of the weight.

In Europe, the recovery is holding up well and should the euro gain traction, it could spell trouble for DXY that is already exposed below two level of critical support, as eclipsed in the above daily chart.

''We think the ECB will announce a gradual scaling back of bond purchases from Q4,'' the analysts at ANZ Bank argued.

Author

Ross J Burland

FXStreet

Ross J Burland, born in England, UK, is a sportsman at heart. He played Rugby and Judo for his county, Kent and the South East of England Rugby team.