Three dividend stocks that look interesting for the long run: BHP, MRNA, BTI

- Dividend stocks have been gaining attention as many are value orientated.

- With low bond yields, dividend stocks can look attractive.

- Rising bond yields mean higher dividend payments are required for higher risk.

Dividends are always of interest to those looking for a regular income or those seeking to live from a retirement portfolio. With interest rates having been pinned to multi-decade lows until recently, investors had been seeking yield in other areas like the equity or bond markets. Most of the recent capital inflows were to areas of questionable credit quality with junk debt yields being incredibly low versus historical norms and the spread over US treasuries being much too narrow for this author's risk tolerance. Equities saw inflows but mostly to the high-growth sector where investors looked for capital appreciation rather than a sustainable dividend.

However, with rising interest rates and the recent discovery that bear markets are not a prehistoric relic, investors have once again begun to look for safety. This has meant avoidance of high-growth names and a return to cash cows and value-based investing. In this article, I will outline some strong dividend stocks – those that have high cash generation or cash balances and have a long history of paying stable and growing dividends. I will also add to the mix one that is a bit out of left field but may be interesting going forward.

BHP Group (NYSE: BHP)

In this inflationary environment, a cursory look back to the last period of sustained inflation saw commodities outperform and offer a possible hedge against inflation and recession. BHP is a mining company involved in mining precious metals, coal, silver, uranium and other commodities. Several macroeconomic factors may benefit this commodity mix going forward, especially with the recent geopolitical developments. Chief among them is the increasing electrification of vehicles and other industries. This requires intensive mineral usage, namely copper.

Uranium has also recently seen a sharp uptick in interest as the nuclear energy debate reignites following the oil price spike and Russia-Ukraine conflict. Copper prices have been declining this year on the expectation of a global recession, which would likely hit demand. However, the longer-term outlook looks more bullish. Like the oil industry, the past number of years have seen underinvestment in mining. While we may have short-term headwinds, the longer-term outlook is one of shortage. This is a similar outlook to oil and why we will be looking to add oil stocks on any fall back to the $70s. Oil stocks have instead focused on cash generation and returning cash to shareholders via buybacks and chunky dividends.

BHP looks attractive on just about every level bar momentum. BHP stock is down 17% this year and a significant 30% over the past six months. That has come despite the company reporting record profits of $41 billion in 2022. BHP has also focused on reducing its debt levels and now carries a tiny amount of debt, meaning more cash is available to shareholders – be that via buybacks or dividends. The company has just paid its last dividend at the start of this month, and at current prices the yield is an enticing 11%.

During the last earnings presentation, BHP said it will look to expand its iron ore operations as it expects Chinese demand to increase. This is the key driver in my view. China appears to be in an economic slowdown but is also engaging in loose monetary policy to offset this. By now we are all aware of how loose monetary policy leads to outsized equity performance, and BHP has exposure to the Chinese market. The miner has also been looking to add to its copper production to expose itself to the green energy transformation.

With a yield of 11% and a strong cash position, BHP looks like an attractive proposition. The key caveat is its over-reliance on China, but the company has virtually no debt, so it will look for acquisitions to give it more diversification and exposure to green energy as well as the potential for buybacks and dividends.

Below we can see growing net income and revenue and the paydown of long-term debt. BHP now has cash over its debt pile, so it could essentially pay it down if it wanted to.

Source: Refinitiv

Technically, we can see BHP has already priced in a global slowdown and has retraced much of its recent gains. The pandemic low is $22, and it is unlikely we will test that price given the current macro environment. Inflation is typically supportive of rising commodity prices. There is the possibility of some headwinds ahead as the bear market in equities continues and China deals with its likely property sector slowdown. This could present an interesting pullback for BHP in my view. It is an attractive long-term proposition to combat inflation and potential rising commodity prices.

Moderna (MRNA)

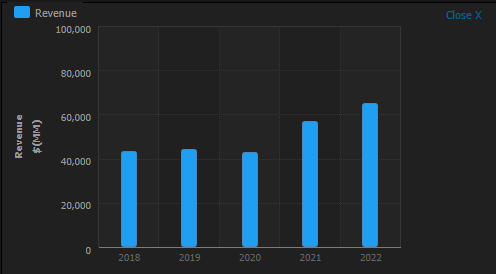

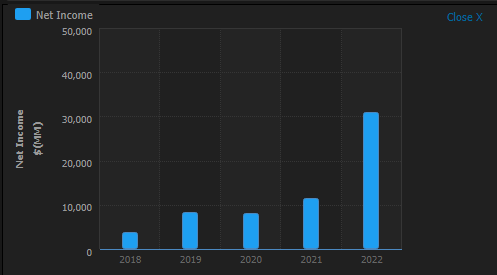

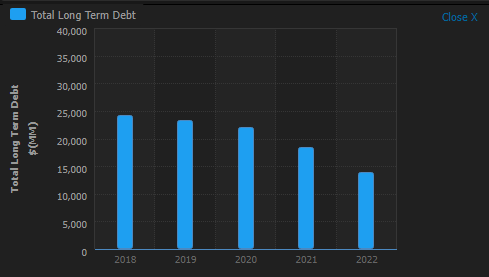

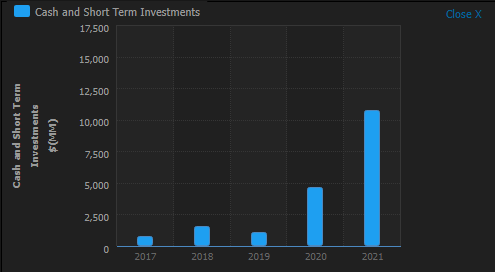

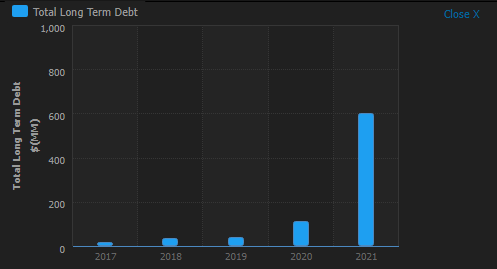

One unusual stock to put in an article about dividends does not pay any dividends. Bear with me, I have not lost my marbles. Moderna (MRNA) has piles of cash after the pandemic, and it will look to do something with it. Looking at our chart below, we can see that Moderna has about $11 billion dollars in cash and debt of $600 million. Basically, it is sitting on $11 billion of cash.

The pandemic is hopefully entering its final winter, but there is one more round of vaccine rollouts upon us, and it may be that this becomes an annual event much like the flu and associated flu vaccine. On that note, Moderna is developing a flu vaccine, and with the emergence of new covid variants it seems likely that the company will continue to generate cash and so add to that enormous cash pile.

At some stage, shareholders will look to be rewarded, and the healthcare sector is one with a history of dividend payout. Pfizer (PFE) has a dividend yield of nearly 4% and has grown its dividends for over a decade. If you want your dividend payout now, perhaps Pfizer is the stock to go for, but I think Moderna offers the better potential. Pfizer trades on a P/E of over seven, whereas Moderna's P/E is just over four. Yes, that's right – four. It is difficult to find many stocks trading on such a low multiple, selling a product with global demand, piles of cash and virtually zero debt. The pandemic has yet to run its course. Just witness how China is still engaged in rolling lockdowns.

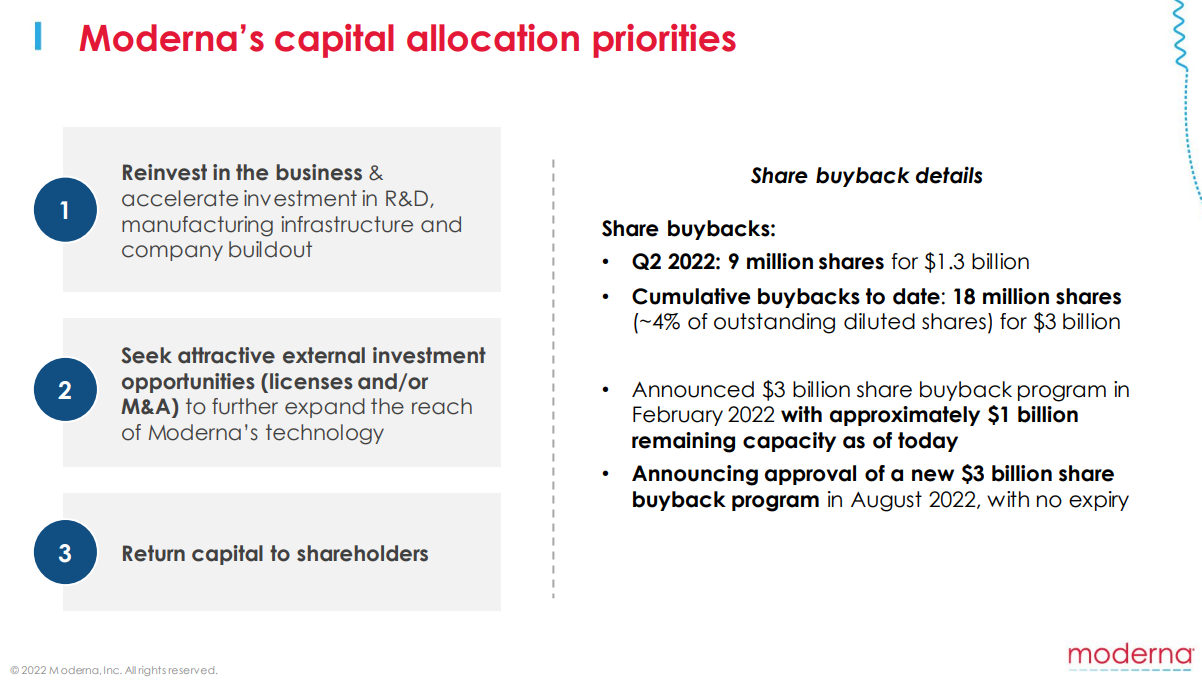

Recent trends in various countries approving the Omicron vaccine attest to further demand. Moderna in short is a play on its strong cash position. It recently completed a massive buyback program and has the capital to do more by returning capital to shareholders via dividend. The company has already announced a new buyback program of $3 billion.

Source: Refinitiv

British American Tobacco (BTI)

Tobacco companies have been under pressure for the past number of years as regulations tighten on the industry. However, tobacco companies are highly cash generative, as well as offering large hordes of cash. Interestingly, the majority of research I have read seems to indicate smoking increases during a recession. If correct this could add some defensive qualities to a high dividend yield and cash-rich stock.

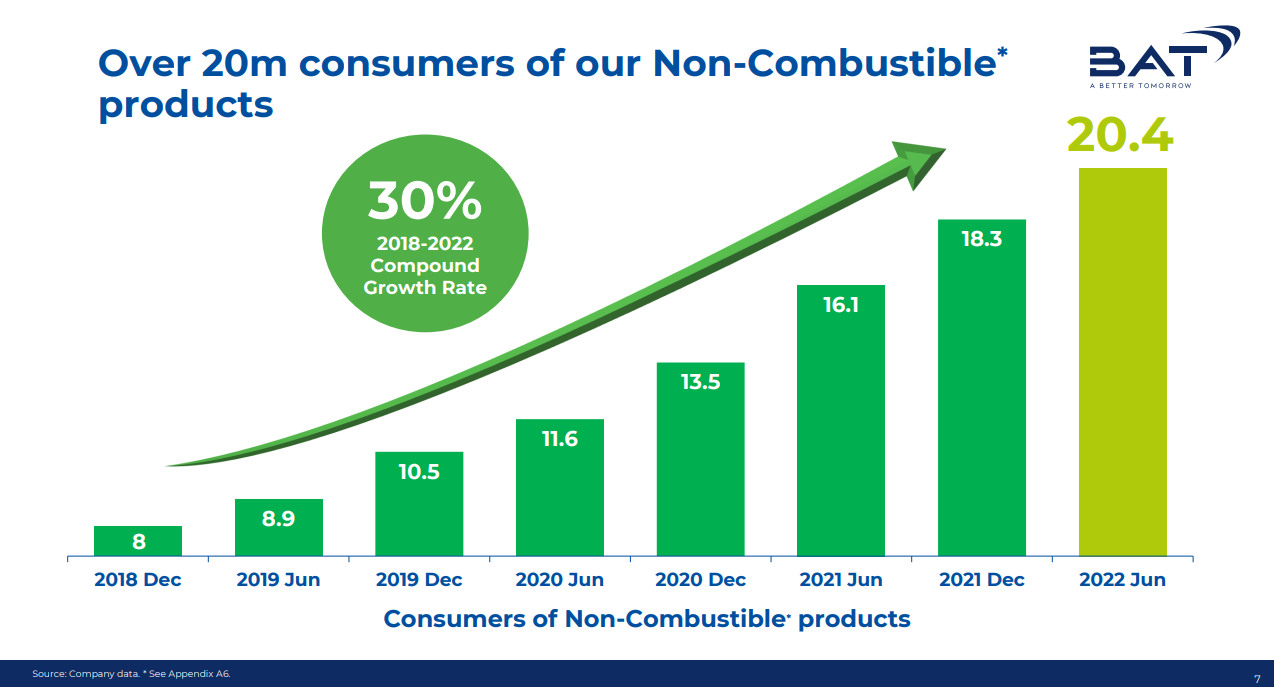

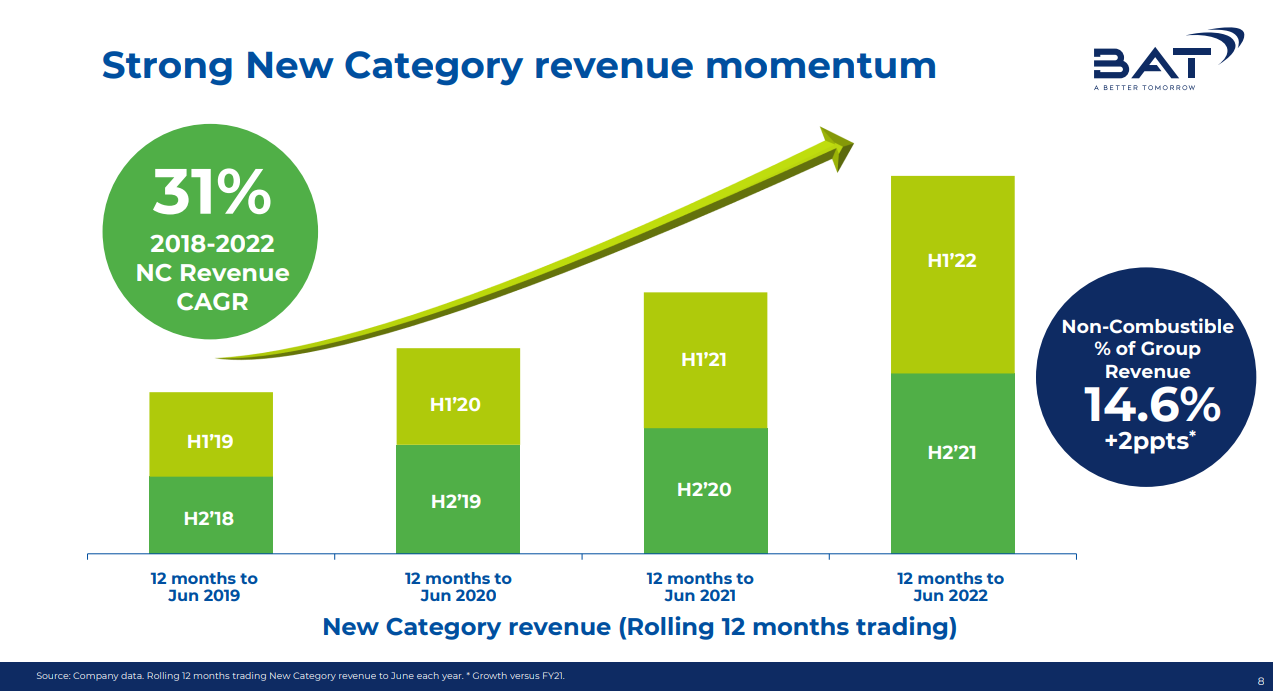

British American Tobacco (BTI) currently offers an attractive yield of 7.5%. BTI holds over $5 billion in cash on its balance sheet. The recent sell-off in the stock market has not been felt here with BTI actually up 5% so far year to date. BTI has expanded its revenue stream into the growing e-cigarette business and expects this growth to continue. As we can see from the company slides below, non-combustible now accounts for nearly 15% of total revenues. This sector is growing sharply, reducing BTI's dependence on cigarettes.

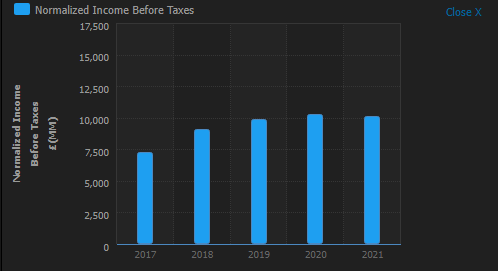

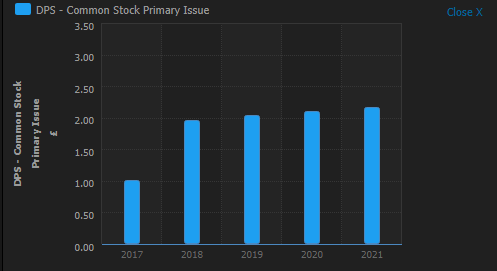

Despite this as we can see, revenue growth is steady overall at the group level, and income and dividend payments remain the same. The company should, therefore, continue to benefit from the emergence and strong growth of the e-cigarette sector while having some defensive qualities from cigarette revenues in a recession. Recall from Econ101 that cigarettes are an inelastic demand model, meaning demand remains relatively constant despite the price.

Source: Refinitiv

The recent sell-off in Altria has dragged the sector lower and presents an opportunity.

BTI has retraced to its 200-week moving average, and despite recent price falls we still see a rising accumulation/distribution line. This would indicate buying power holding constant.

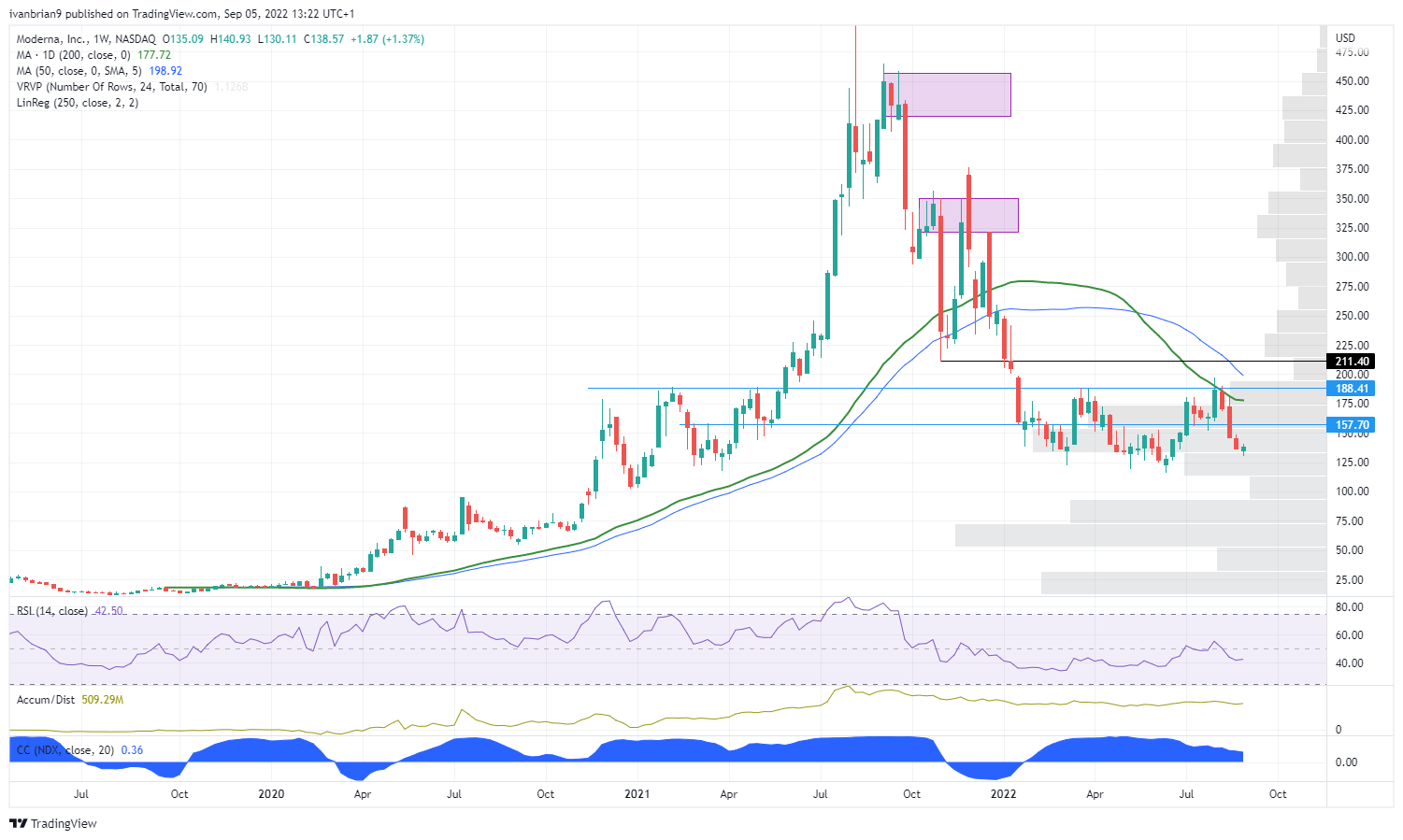

BTI weekly chart

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.