Megacap earnings preview: Trick or treat? AI spend decides

As five of the "Magnificent 7" tech giants—Apple, Alphabet, Amazon, Meta, and Microsoft—report earnings this week, investors will be keenly watching their updates on core businesses such as advertising and cloud services, and more importantly, spending on artificial intelligence (AI) and its tangible returns. These companies, with a combined market cap of $12 trillion, have driven market gains this year, making their results pivotal for the ongoing equity rally.

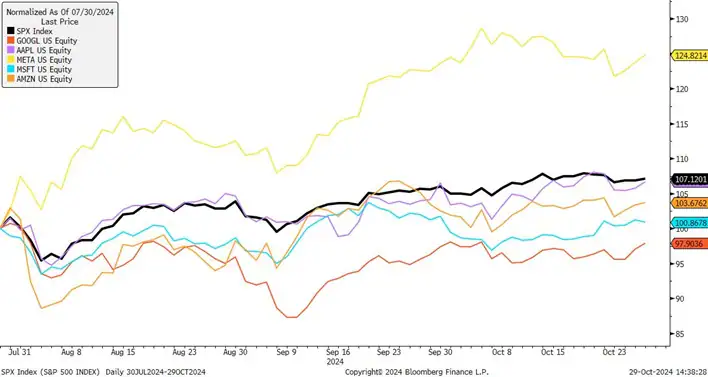

However, since peaking on July 10, the gap between Big Tech and the rest of the market has been narrowing amid closer scrutiny on the efficacy of their AI spend. Microsoft, Alphabet, Amazon, and Meta collectively ramped up their capital expenditures in Q3, pouring $56 billion—a 52% year-over-year increase—into areas like AI. While the transformative potential of AI is widely acknowledged, investors are now questioning the timing and scale of returns from these hefty investments. This earnings season could serve as a critical test for these megacap leaders, many of whom (except Apple and Meta) have yet to reclaim their July highs, even as they trade at valuations above historical norms and the broader market.\

Alphabet: Growth anchored by Ads and cloud, but AI spending looms large

-

Earnings due: Tuesday (Oct 29) after-market.

-

Revenue estimate: $86.44 billion (vs. $76.69 bn in Q3 2023).

-

EPS estimate: $1.84 (vs. $1.55 in Q3 2023).

-

Capex estimate: $12.88 bn (+60% YoY).

-

Key drivers: Youtube and Search ad revenue, Cloud computing growth.

-

Key risks: Regulatory scrutiny over monopoly practices, Long-term risks to Google’s Search business, Competition from Meta’s AI search engine, Waymo (self-driving car business) growth after a recent pact with Uber.

-

Other thoughts: Alphabet’s setup remains relatively undemanding, having underperformed the S&P 500 since Q2, largely due to ongoing regulatory concerns. This positioning could offer an opportunity if earnings reflect AI and cloud momentum despite the headwinds.

Meta: AI-optimized Ads enabling outperformance

-

Earnings due: Wednesday (Oct 30) after-market.

-

Revenue estimate: $40.26 bn (vs. $36.15 bn in Q3 2023).

-

EPS estimate: $5.25 (vs. $4.39 in Q3 2023).

-

Capex estimate: $11.03 bn (+69% YoY).

-

Key drivers: Ad revenue and profitability, driven by Meta’s AI optimization driving efficiency for advertisers.

-

Key risks: ROI on AI spending, Slowing economic growth.

-

Other thoughts: With Meta's stock trading near all-time highs, the bar is higher, and any signs of slowing ad spend due to consumer weakness could weigh on sentiment. Meta’s ability to show that its AI investment is effectively translating into ad revenue growth will be crucial.

Microsoft: Azure growth meets costly AI expansion

-

Earnings due: Wednesday (Oct 30) after-market.

-

.Revenue estimate: $64.52 bn ($56.52 bn in Q1 FY2024).

-

EPS estimate: $3.11 ($2.99 in Q1 FY2024).

-

Capex estimate: $14.55 bn (+47% YoY).

-

Key drivers: Azure growth.

-

Key risks: AI prospects and associated costs, Competition from Meta’s AI search engine, margin contraction amid datacenter expansion, Copilot adoption.

-

Other thoughts: While Microsoft’s Azure growth remains solid, the market will closely watch its AI-driven capital expenditures. The ability to maintain or grow margins amid heavy investment in AI infrastructure will be pivotal for the stock's performance.

Apple: Limited AI exposure but service revenue in focus

-

Earnings due: Thursday (Oct 31) after-market.

-

Revenue estimate: $94.31 bn (vs. $89.50 bn in Q4 FY2023).

-

EPS estimate: $1.59 (vs. $1.46 in Q4 FY2023).

-

Key drivers: Less relative AI spending, Strong momentum in service revenues.

-

Key risks: Any signs of sluggish demand of latest iPhone, Popularity of Apple Intelligence, Scaling back of Vision Pro production.

-

Other thoughts: Apple’s high stock price close to all-time highs sets a higher bar for earnings, especially in a weaker consumer spending environment. Strong results and guidance in services revenue, rather than AI, will be essential to justify current valuations.

Amazon: Short-term AI costs clash with long-term potential

-

Earnings due: Thursday (Oct 31) after-market.

-

.Revenue estimate: $157.29 bn (vs. $143.08 bn in Q3 2023).

-

EPS estimate: $1.16 (vs. $0.94 inn Q3 2023).

-

Key drivers: AWS, e-commerce and digital ad sales.

-

Key risks: Capex guidance risking profit erosion, especially around its satellite initiative, Project Kuiper.

-

Other thoughts: Amazon's growth in AWS and ad sales remains solid; however, high capital expenditure could put pressure on profitability. As ad budgets may soften with a weakening consumer, Amazon’s guidance on costs and AI-related investments will be closely scrutinized.

Source: Bloomberg

What Megacap earnings mean for Nvidia?

Sustained capital expenditures (capex) on AI by tech giants like Alphabet, Amazon, Microsoft, and Meta is a double-edged sword: while it could accelerate their growth and maintain competitive advantages in AI, it also puts pressure on profitability, especially as investors start questioning the return on these massive investments.

For Nvidia, however, this continued spending is an unequivocal positive, as it translates directly into demand for its advanced GPUs, which are critical for powering AI workloads. As long as Big Tech remains committed to advancing their AI infrastructure, Nvidia stands to benefit as the go-to supplier, securing its growth trajectory even if some tech giants face profitability pressures.

While sustained capex spending by Big Tech is undoubtedly a growth driver for Nvidia, there are potential risks that could temper this upside. Supply constraints, especially around Nvidia's upcoming Blackwell chips, could limit its ability to meet soaring demand from AI-driven projects. Additionally, competition in the AI hardware space is intensifying, with companies like AMD and Google developing their own AI chips, which could eventually impact Nvidia's market share. Finally, if regulatory scrutiny on AI or tech spending tightens, this could dampen Big Tech's capex budgets, indirectly affecting Nvidia’s sales outlook. Despite these risks, Nvidia remains well-positioned as a key beneficiary of the current AI boom. Note that Nvidia doesn’t report earnings until November 20.

Read the original analysis: Megacap earnings preview: Trick or treat? AI spend decides

Author

Saxo Research Team

Saxo Bank

Saxo is an award-winning investment firm trusted by 1,200,000+ clients worldwide. Saxo provides the leading online trading platform connecting investors and traders to global financial markets.