McDonald's Stock Deep Dive Analysis: MCD price target at $200 on high valuation, flat revenues

Welcome back to the deep dive series. This time our focus shifts to consumer giant McDonald's Corporation (MCD). As ever we will outline our valuation framework using discounted cash flow and relative valuation techniques. Then we will adjust based on some assumptions on an overall macroeconomic level as well as more company-specific measures. After that we add to this with an overview of the charts to see how it fits in before coming up with our final 12-month price target for McDonald's stock price.

Contents

- Company overview and history

- Wall Street consensus forecasts

- Key valuation rating metrics

- Peer value comparison

- Macroeconomic backdrop, market cycle and sector analysis

- Recent news and earnings

- Forecast and valuation

- Technical analysis

- Executive summary, recommendation and price target

McDonald's company overview and history

Not sure how much detail we really need to go into for this one. Practically everyone is familiar with McDonald's and the products and services they offer. McDonald's was founded in 1955 and is headquartered in Illinois. It quickly became an American institution and has undergone a rapid global expansion, mostly during the 1970s and 1980s, and is now practically visible in every country on earth. McDonald's operates in the restaurant sector through direct ownership and franchise business. The company offers a range of signature lines such as the Big Mac, McChicken and ice cream sundaes. Over the past number of years, the company has adapted its menu to account for changes in consumer tastes; now salads, fruit and coffee are mainstays on the menu. McDonald's went public on April 21, 1965.

Also read: Tesla Stock Deep Dive: Price target at $400 on China headwinds, margin compression, lower deliveries

As we can see below, overseas markets represent over 50% of McDonald's revenue with the US being the other major source. This means the strong dollar is a major headwind for earnings in the current cycle.

Source: Refinitiv

McDonald's operates mostly via franchises with less than 10% of its restaurants directly owned. To this day, it is one of the most successful franchise models in history.

Source: Refinitiv

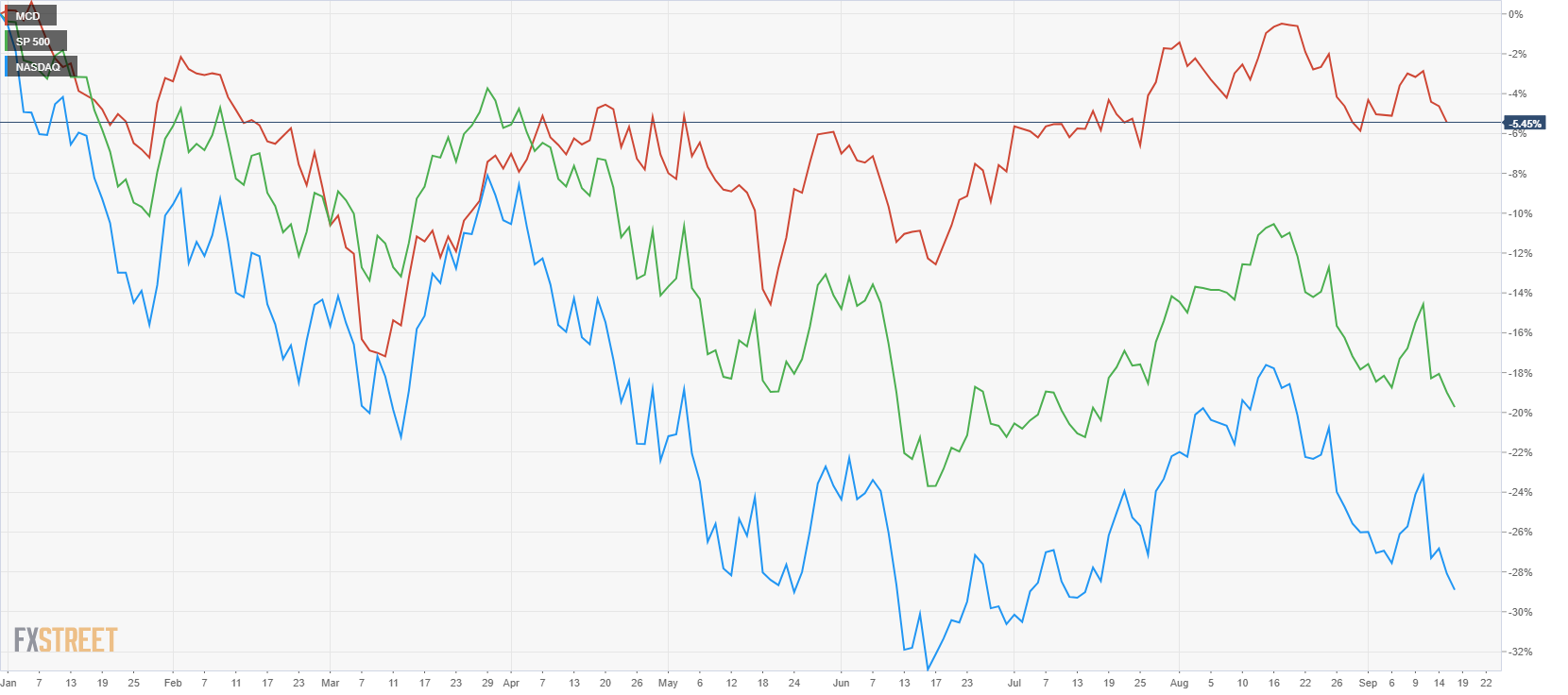

Given its huge and long established business, McDonald's would be seen as a relatively defensive stock. Below is the performance since the start of this year. McDonald's stock has comfortably outperformed the main indices. McDonald's is down 5% for the year, while the S&P 500 is down 20% and the Nasdaq down 29%.

However, if we go back over the last five years, the picture changes with the Nasdaq outperforming, while McDonald's still outperforms the S&P 500.

-637989157683758148.png)

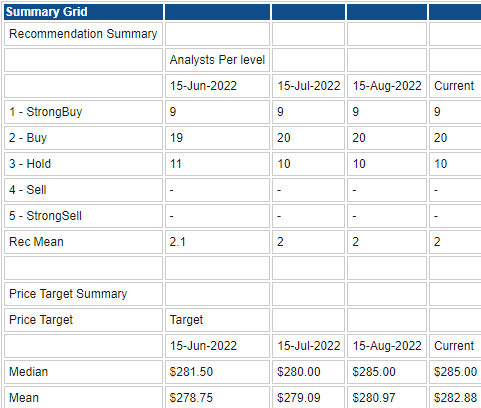

Wall Street consensus forecasts

The amazing thing is that there is not a single Sell recommendation. Given that the stock is down 5% on the year so far, you would think at least one analyst would have noticed this and the bear market we find ourselves in, but the optimism of Wall Street analysts continues to baffle. McDonald's is defensive for sure. It is always the lowest price point and has incredible pricing power with consumers and its suppliers.

In an economic downturn it remains a "treat" for the family and replaces more expensive dining out options. Still with the advent of inflation and consumers reigning in spending, it may be hard for McDonald's to grow revenues and margins. This is something we will look into in more detail below.

Source: Refinitiv

Key valuation rating metrics

Market cap: $186 billion

Enterprise Value: $228 billion

Free Float: 735.7 million

IPO date: 21st April 1965

52-week high: $271.15

52-week low: $217.675

Short interest: 0.50%

YTD performance: -5%

3-year performance: +16%

Source: Refinitiv, TradingView and FXStreet calculations

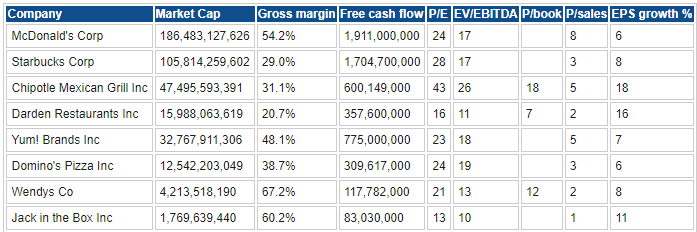

Peer value comparison

Source: Refinitiv, TradingView and FXStreet calculations

Macroeconomic backdrop, market cycle and sector analysis

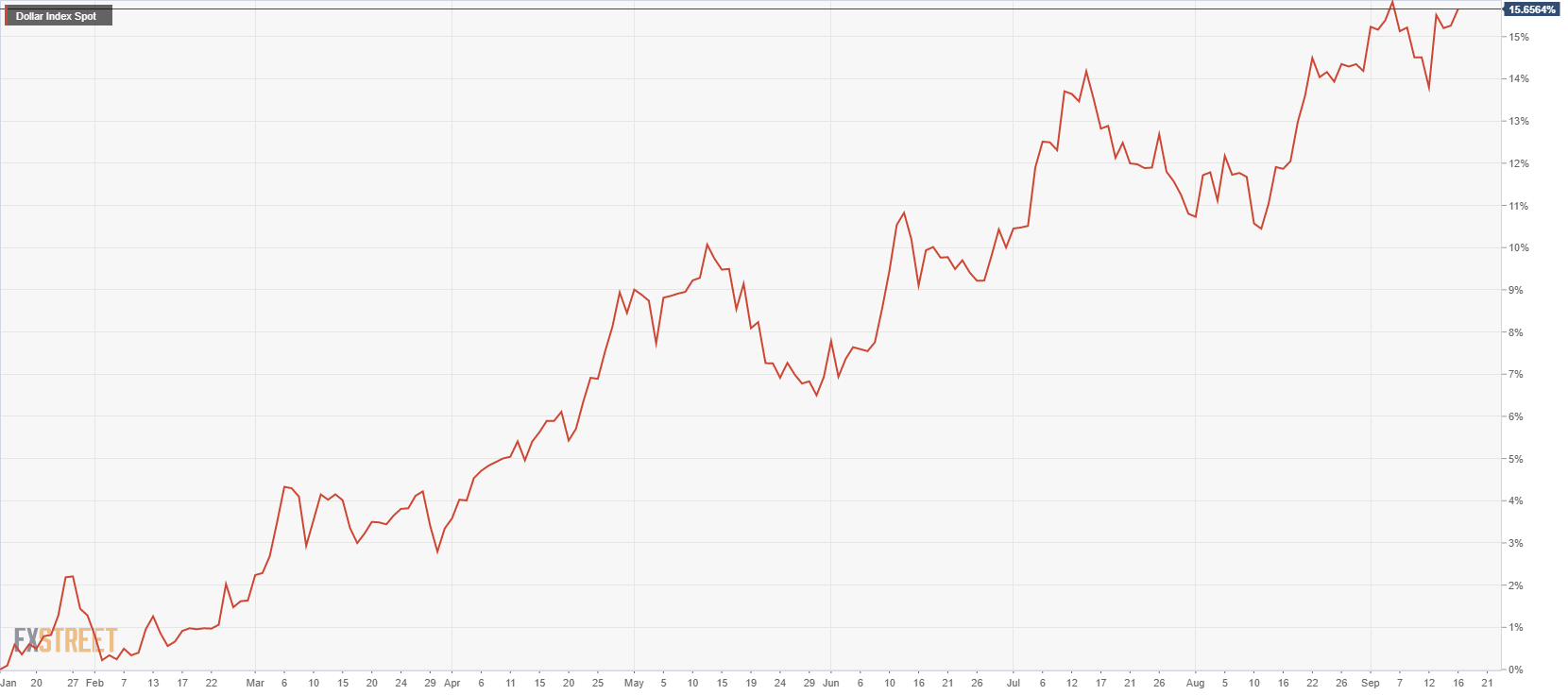

Regular readers may find this section a bit repetitive, but it is important to put the cycle into context. This after all determines stock performance as much as individual micro factors or management skill. Especially for a truly global company such as McDonald's, there is no escaping the macro backdrop. As mentioned the rising dollar will be a serious headwind when converting overseas revenue back into USD. This is perhaps being overlooked by the analyst community.

Dollar Index year to date % change

Last week's CPI number certainly put any notion of inflation quickly coming under control back to sleep. Inflation it seems is here to stay, and that will hurt consumer demand. Bond yields have already spiked considerably after the CPI number. We can use any number of bond yields, but the picture is the same – interest rate predictions have been increased and sit at the top of recent rages.

Also of particular note is that yields are higher than when the S&P 500 bottomed in June. This either indicates equities are behind and need to play catch up or they are a leading indicator and the bond market has got it wrong. In any event, it looks like a continued difficult environment for equities.

US 10 year (orange line) versus Eurodollars Dec 2023

Goldman Sachs has outlined their predictions for valuation metrics based on a recession or earnings slowdown. Q3 earnings will be key.

This chart from Global Investment Research shows S&P 500 price sensitivity based on P/E and expected EPS. pic.twitter.com/FjGIisQBMl

— Overlooked Alpha (Charts) (@OverlookedAlpha) September 15, 2022

This is generally what happens where we are going to.

The Price to Earnings Ratio (P/E) is higher when inflation is low and growth rates are high. During stagflation or times when growth is slow & inflation is high, the P/E ratio goes down. In the stagflationary '70s, the P/E for the S&P 500 $SPY went to single digits. pic.twitter.com/l86bRaKLxz

— Ben Woodward, CFA (@BennettWoodman) September 9, 2022

Big tech, aka FANNGT (whatever you want to call it), still looks to be the ones causing much of the relative overvaluation, so they may have the furthest to fall still despite some spectacular collapses so far (Netflix, Meta Platforms).

The P/E ratio on the S&P 490 is 14.6 pic.twitter.com/v2Bje6VH4n

— Mike Zaccardi, CFA, CMT (@MikeZaccardi) September 1, 2022

Already we can see how valuations for small-caps and mid-caps have corrected, so big caps could and should be next.

The relative strength we have been seeing within middle caps and small caps for weeks now is mainly due to their valuation metrics imo.

— THE SHORT BEAR (@TheShortBear) September 15, 2022

The downturn started about February 2021, almost 2y ago now via $ARKK as a proxy.$IWM was quick to follow, building a range in March 2021. pic.twitter.com/WoMLl1MIZc

Also read: Apple Stock Deep Dive: AAPL price target at $100 on falling 2023 revenues

Recent McDonald's news and earnings

McDonald's missed on the top line in its last earnings report. Earnings per share came in at $2.55 versus consensus estimates of $2.47, but revenue was $5.72 billion versus $5.81 billion. The company instigated price increases to offset rising costs and relied on international markets to pick up the slack versus the US slowdown.

As expected McDonald's mentioned currency impacts during the call, and we expect these to continue given the ongoing strength of the dollar. McDonald's took a charge of just over $1 billion from exiting Russia. The next earnings are scheduled for October 24. What is of particular interest is the number of downward revisions in the past three months. There were 17 downgrades versus just 14 upgrades to earnings estimates.

Also read: Citi Stock Deep Dive: Earnings, Buffet factor support our BUY rating and $60 price target

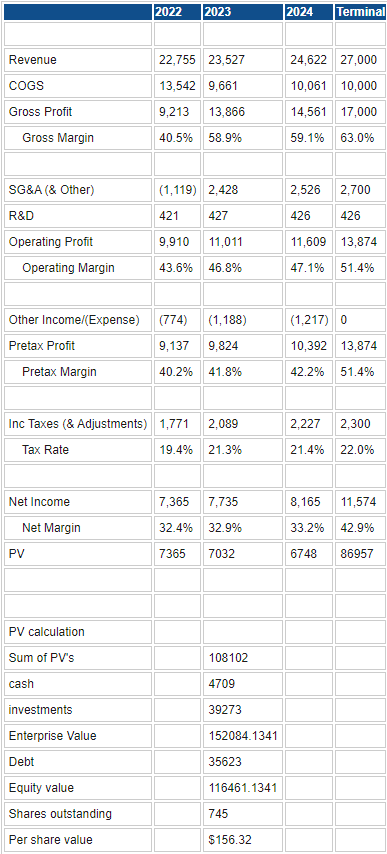

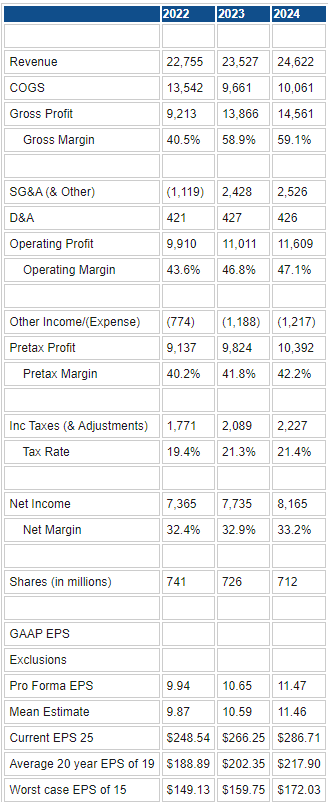

McDonald's forecast and valuation

As ever we use two models: the discounted cash flow and relative valuation models. First, we start with consensus estimates and tweak them based on what we see happening to margin and sales growth. We then add an extra layer of analysis from the overall macro environment and technical analysis to get our overall 12-month price target.

Source: Refinitive, FXStreet calculations

Source: Refinitive, FXStreet calculations

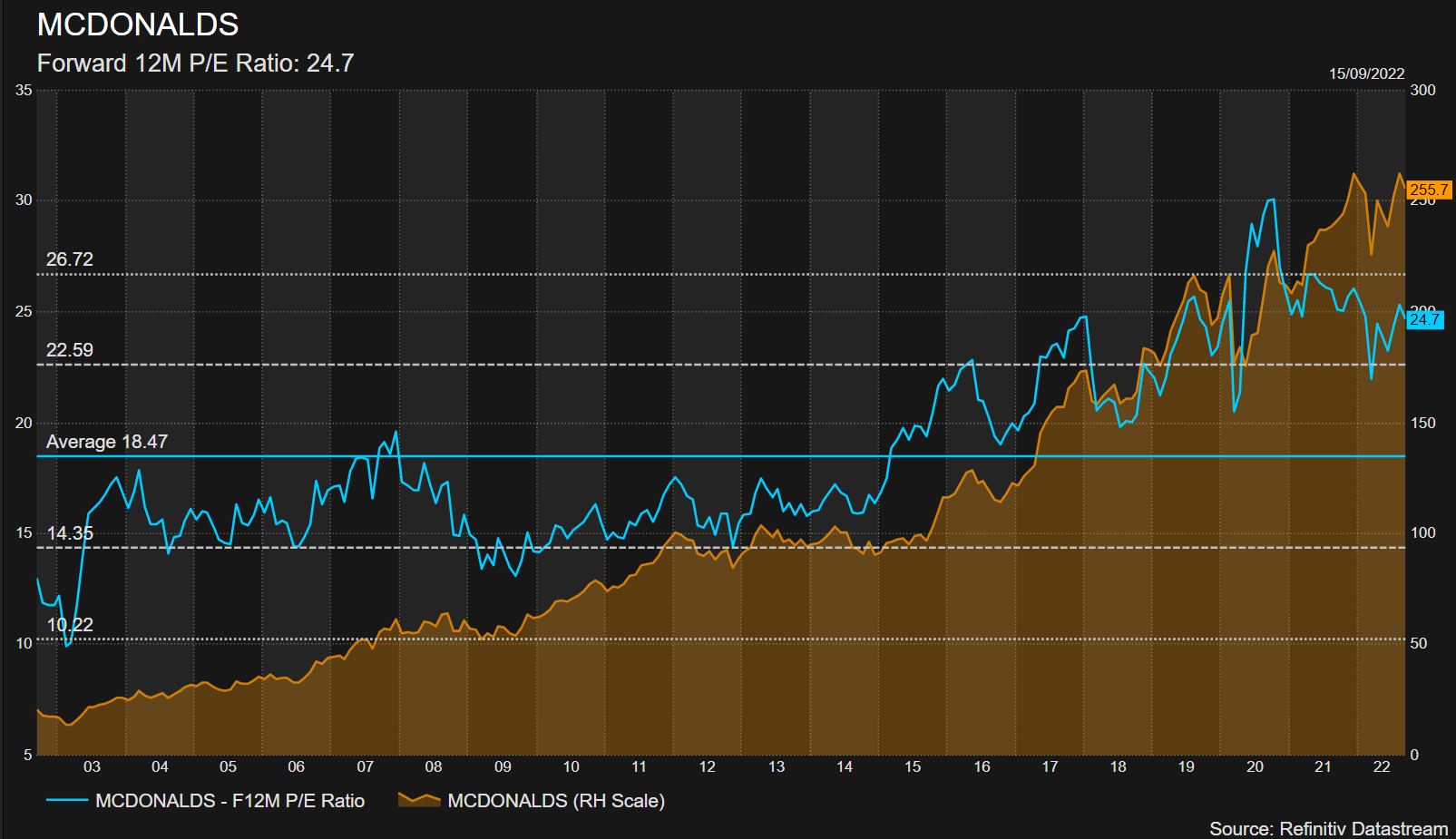

There is not much need to adjust our figures as it is becoming clear McDonald's stock is overvalued. Trading on a current P/E of 25 is toward the top of the 20-year average range. Forecasting revenues to grow at consensus gives us a possible upside to $266 based on the P/E remaining constant. Looking at the DCF calculation, however, that would give us a fair value of $156. Again that is based on consensus. I tend to think 2023 will see a flatlining in terms of revenue and margins. That means EPS of $9.94, giving us a price target at current levels of $248.

However, I also tend to think McDonald's will see its P/E ratio rerate along with the S&P 500 back to at least 20. This gives a price target of $189. This is more in keeping with the discounted cash flow outcome.

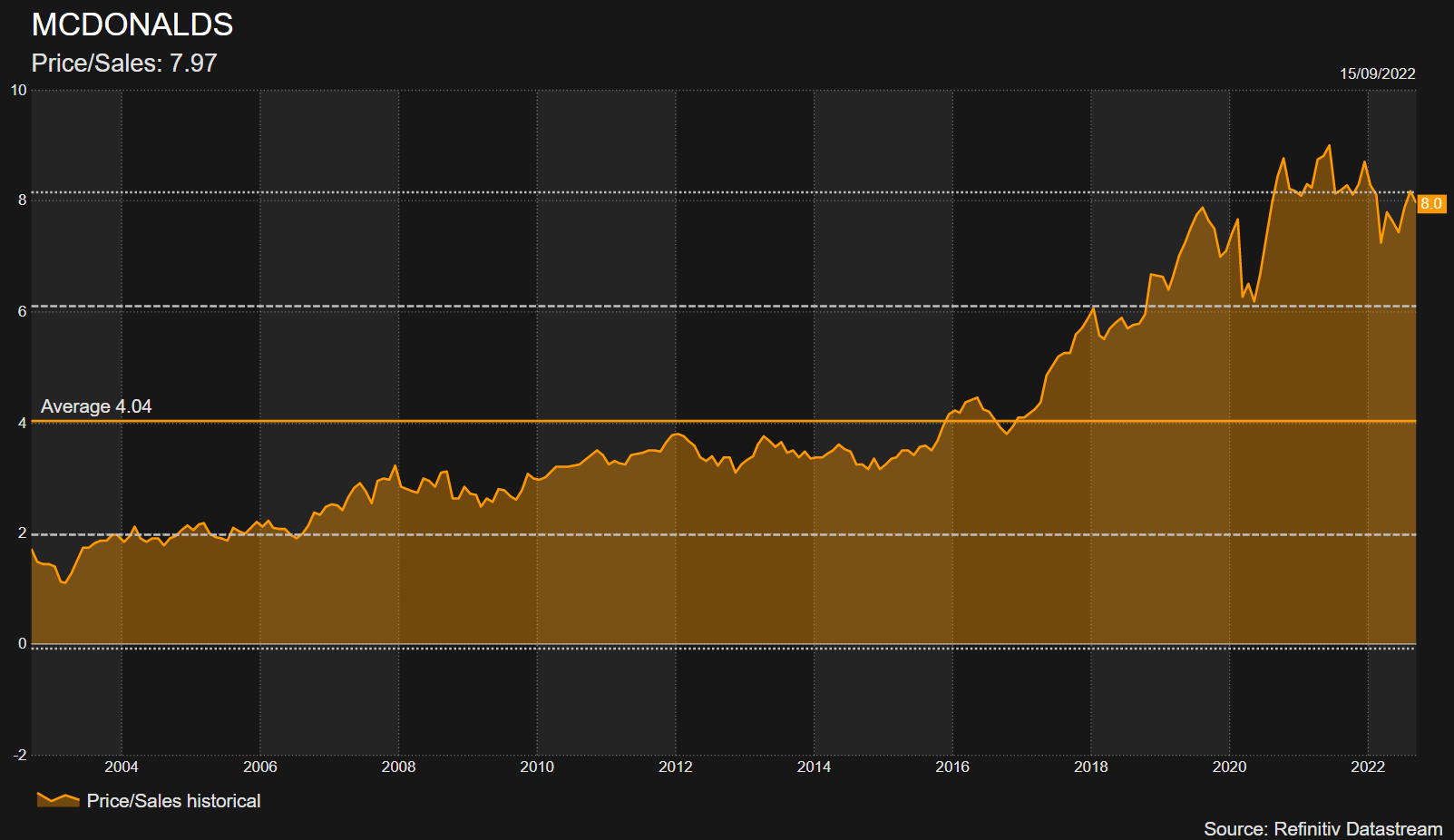

The two charts below show historical comparisons for McDonald's valuation. The average price/earnings (P/E) going back 20 years is 19. It is trading more or less in line with the overall restaurant sector. All sectors appear to be in line for a rerating lower though if current economic forecasts for inflation and interest rates prove accurate. If we look at other metrics, they also look too high.

"McDonald's is a cash cow though and immune to any recession," you interrupt. For starters, not many are immune to recession, inflation, rising costs or a strong dollar. But, yes, McDonald's is an extremely well-run and cash-generative business. However, valuations during this Fed-juiced period have gotten way too over-stretched. McDonald's trades on over 23 times its free cash flow. The 20-year average is nearer to 15.

McDonald's trades at eight times sales. Over the past 20 years, the average is nearer to four. The recent move up is a causative effect of years of monetary stimulus.

Also read: Walmart Deep Dive Analysis: Hold WMT to play defense vs upcoming US recession

McDonald's technical analysis

At present, it does appear that we have put in a bearish double top around $270. If so, this is a negative sign and adds to my concerns regarding the valuation. There is strong support at $220, and only as recently as March McDonald's stock was trading at that level. I have not seen much reason since March to account for a 20% increase in the MCD stock price and neither has the overall market.

MCD is defensive but not to that extent. Forecasting at consensus but with a rerating gives us a price target of $202.35. The market loves round numbers, so it will be too tempting to trade to $200. It may well be that we go below here. In selecting a price target though, 12 months is the standard timeframe. With the market being forward-looking to the tune of about 6-9 months on average, what we are really forecasting is how McDonald's will look in about 18 months' time. My impression is it will be coping well as it always does, but the overall market will have rerated lower. Thus I am going for a 12-month price target of $200.

McDonald's (MCD) stock, weekly

Executive Summary: Price target and recommendation

Therefore, taking $200 as our price target that necessitates a SELL rating on McDonald's (MCD) stock.

Upside risks

Fed pivot, inflation falls sharply as Fed pauses or cuts rates. (This is unlikely, and if they do it means a deep recession, which is not a reason for equities to go higher)

USD falls (Again, this is unlikely unless we get a Fed pivot above, but it may begin to slow as other countries begin to hike rates as the ECB and BoE are doing)

Downside risks

Inflation remains sticky, and we enter a moderate to deep recession. (This will cause an earnings slowdown and a P/E rerating at the same time and necessitate a steeper fall than forecast)

Also read: Three dividend stocks that look interesting for the long run: BHP, MRNA, BTI

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.