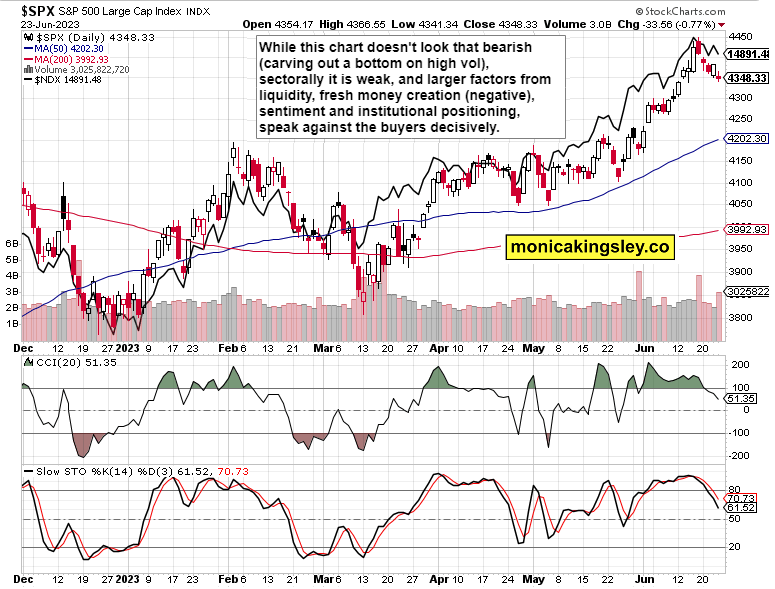

Eye of the storm

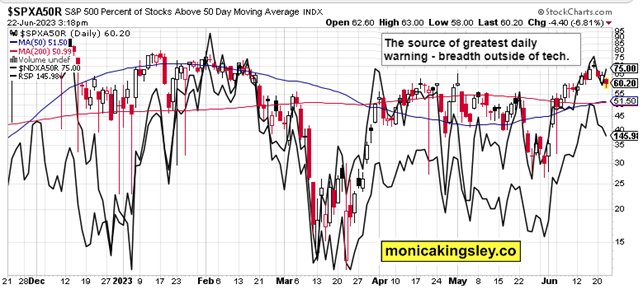

Friday‘s S&P 500 intraday reversal higher didn‘t last into the close even if bonds favored that. The odds though remain heavily stacked against the buyers – from negative money supply growth, LEIs down for 14 months in a row, ISM data, yield curve, tight Fed, Treasury replenishing TGA, greedy sentiment, bank reserves likely to decline as reverse repos won‘t be enough for boosting TGA, sharply up bankruptcies vs. year ago, tax collection down some 20% YoY, tight bank lending standards, rising credit card debt, strain in leading job market indicators – or the narrow leadership that‘s not seeing a broadening of market breadth, but represents eye of the storm, if you will.

Last week, I compared the rally to both the false dawns of the dotcom crash and the advance beginning in spring 2008 till the Beijing Olympics. Analogical to the no landing or soft landing hopes, this will have consequences – and the money flows into stocks just aren‘t there compared to bond funds.

Ask yourself – can a sustainable stock market bottom be reached before recession even strikes, and before Fed turns dovish or a major fiscal stimulus is announced? Hardly, not really.

The rally off Oct lows is failing, monetary tightening around the world continues, core inflation is still resilient for now, and certain elements of inflation (owners‘ equivalent rent and energy prices as a minimum) would return in the 2H 2023, proving the stagflationary character of the environment we would be in.

And don‘t forget about profit margins and overall corporate revenues that are going to be hit in a recession – so, it‘d not about just P/E, but also E. All in all, bearish.

Real estate would positively surprise during a recession, but the key winners would be necessities of life, disruptive tech, and resource stocks making a return, preceded by gold and silver rising.

And how about the latest events iu Russia? Introducting uncertainty and unpredictability is hardly a bullish recipe. Yet I was able to foeree a quick resolution before the brokered deal was announced thanks to my extensive knowledge of Russia, its society and language. Just as I was uneasy in Feb last year before the hostilities, and called for no longs in the stock market.

S&P 500 and Nasdaq outlook

Friday‘s seesaw turned the bearish direction pretty fast, and following 4,415, there is 4,360s as the next milestone for the sellers. I expect the 4,385 not to stand in the way much. Similarly in an environment of rising yields, utilities wouldn‘t offer much of a protection, and when Big Tech succumbs to the disconnect to yields, the ES decline would quicken. Retail, smaillcaps and transportation joining in are the ingredients that put an end to the new bull market narrative.

Sectoral view is enough to determine that the sellers have an advantage that the tech isn‘t to overcome.

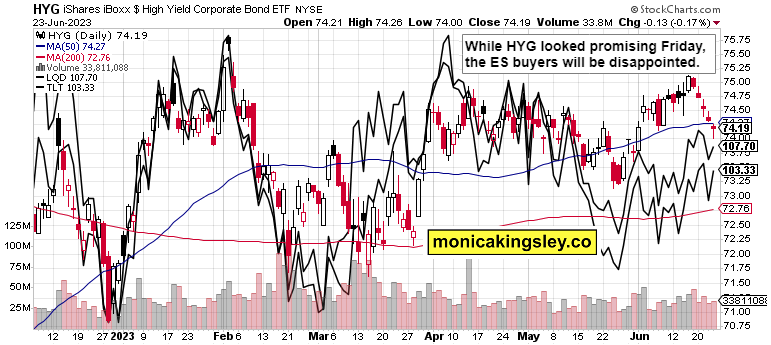

Credit markets

Friday‘s bonds posture reflects the intraday rally attempt in stocks, which however wouldn‘t be sufficient for ES gains ahead. This chart evens the stock market outlook for Monday – the sellers are though to eventually win.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.