Exxon Mobil (XOM) Stock Deep Dive: Falling oil prices result in a HOLD rating with a $94 price target

Welcome back to our deep dive series where we dive into the oil sector this time with a focus on Exxon Mobil. Exxon trades on the NYSE under the ticker XOM. As ever, we will go through some valuation methods and tweak them to come up with a 12-month price target. We will use discounted cash flow (DCF) analysis as well as a relative valuation framework. These methods will then be adjusted to take into account the macroeconomic backdrop and oil price projections, as well as the technical outlook on the stock.

Contents

- Company overview and history

- Wall Street consensus forecasts

- Key valuation rating metrics

- Peer value comparison

- Macroeconomic backdrop, market cycle and sector analysis

- Recent news and earnings

- Forecast and valuation

- Technical analysis

- Executive summary, recommendation and price target

Exxon Mobil: Company overview and history

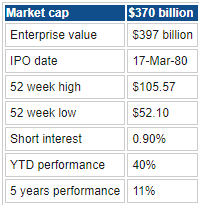

Exxon Mobil is an oil and gas explorer and producer that operates in the US and internationally. Exxon explores extracts, produces and refines oil and gas products as well as related petrochemical products. Exxon Mobil has a long history, having been founded in Texas in 1870 and is still headquartered in Irving, Texas. The company has over 60,000 employees globally and approximately 20,000 wells. Exxon Mobil listed via IPO on the New York Stock Exchange on March 17, 1980.

Exxon Mobil splits its revenue breakdown across three main divisions. Upstream is oil and gas extraction, Downstream is the production and distribution of that oil, and obviously Chemicals are, well, petrochemicals. Exxon then divides those three divisions – Upstream, Downstream and Chemicals – into US and non-US segments. Downstream non-US is the biggest segment by revenue. Also of note is intersegment revenue, which basically accounts for revenue from one division of Exxon to another. Downstream, i.e. selling the final oil and or gas, is the main revenue driver here.

For the most recent full year of 2021, Exxon Mobil's average selling price per barrel of oil was approximately $66. With current oil prices having nearly doubled from that level, it is no surprise that 2022 has seen a big boost in revenue terms.

Source: Refinitiv

The Exxon Mobil (XOM) stock price has neatly followed the crude oil price higher.

Exxon Mobil (XOM) versus WTI Oil weekly to 2019

XOM Stock: Wall Street consensus forecasts

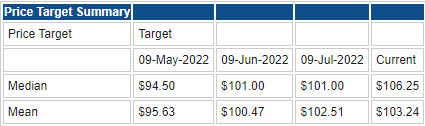

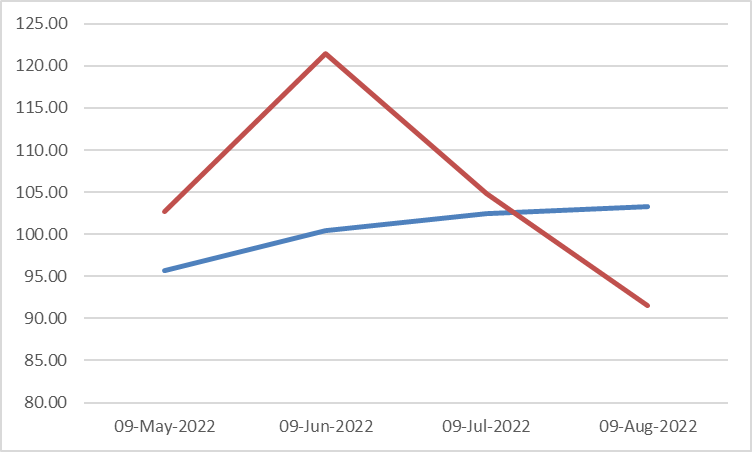

The interesting point to note is how forecasts have recently been upgraded based on strong earnings. Earnings are historical and not predictive though. The biggest predictive factor in terms of oil stock performance is the oil price itself. Oil prices are falling as fears grow over a global recession. This will hurt oil demand, so as we see below Wall Street has consistently raised price targets for XOM while oil prices have quite frankly collapsed.

Source: Refinitiv

Below we can see how the average analyst price target (blue line) has been rising while the oil price (red line) has been falling. Based on the strong correlation we showed above, this does not really make sense in our view.

Source: Refinitiv

See Also: Tesla Stock Deep Dive: Price target at $400 on China headwinds, margin compression, lower deliveries

Key valuation rating metrics

Source: Refinitiv and TradingView

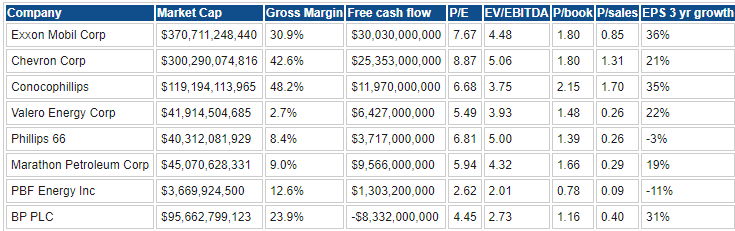

Peer value comparison

Source: Refinitiv

Macroeconomic backdrop, market cycle and sector analysis

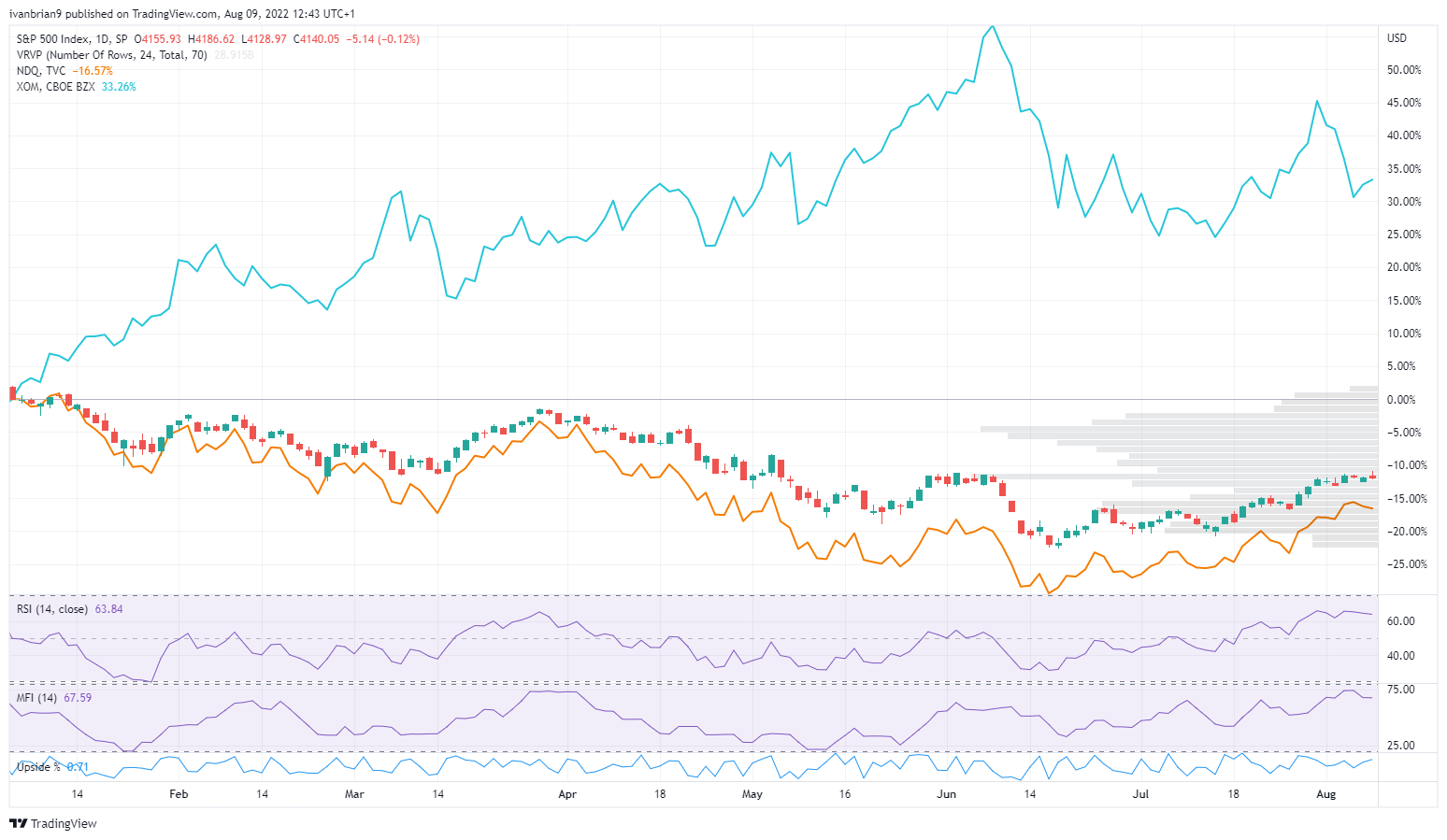

Macro matters have been driving markets this year. Equities have priced in a recession, and a bear market was eventually triggered across all the main indices. Despite all this, the energy sector managed to be the shining beacon, thanks largely to the surge in oil prices from the Russian invasion of Ukraine. Indeed, the main energy sector index, the XLE, is up 28% year to date, while the Nasdaq and S&P 500 languish.

Exxon Mobil (XOM) stock versus Nasdaq (orange line) and S&P 500 (bars), year to date

While most of our focus in performing macroeconomic research has been on the impact on valuations and multiples, this is not applicable to an energy stock. What is more pertinent, however, is how the price of oil is affected by the macro economy and then how that will flow through to Exxon's bottom line. Note that the most recent quarterly results in our view probably represent peak earnings and peak oil for the next 12 months.

Oil demand is likely to be curtailed by a global slowdown or recession. Gasoline demand has already fallen this summer driving season in the US as consumers adapt to soaring prices. Consumers are choosing to take shorter journeys or not at all. The situation in Europe is even grimmer, and the EU has already implemented plans to reduce gas consumption by 15%. It seems clear to us then that the recent fall in oil prices from $120 to $90 is likely to see the trend continue.

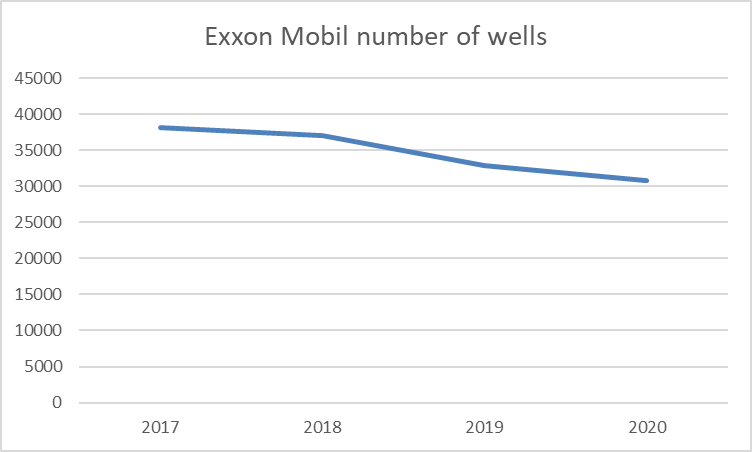

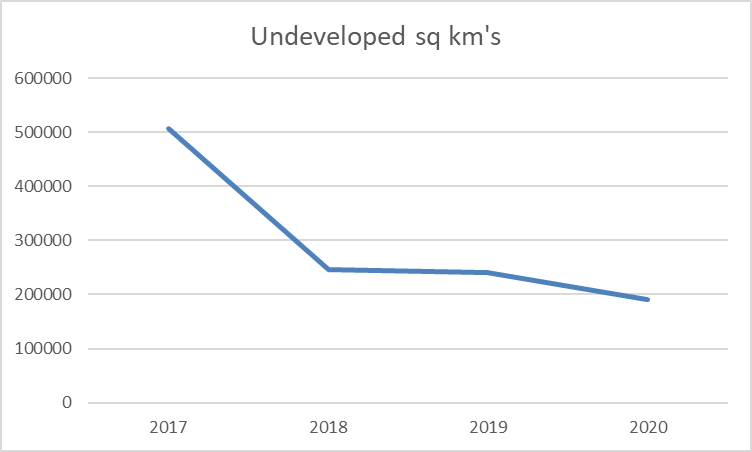

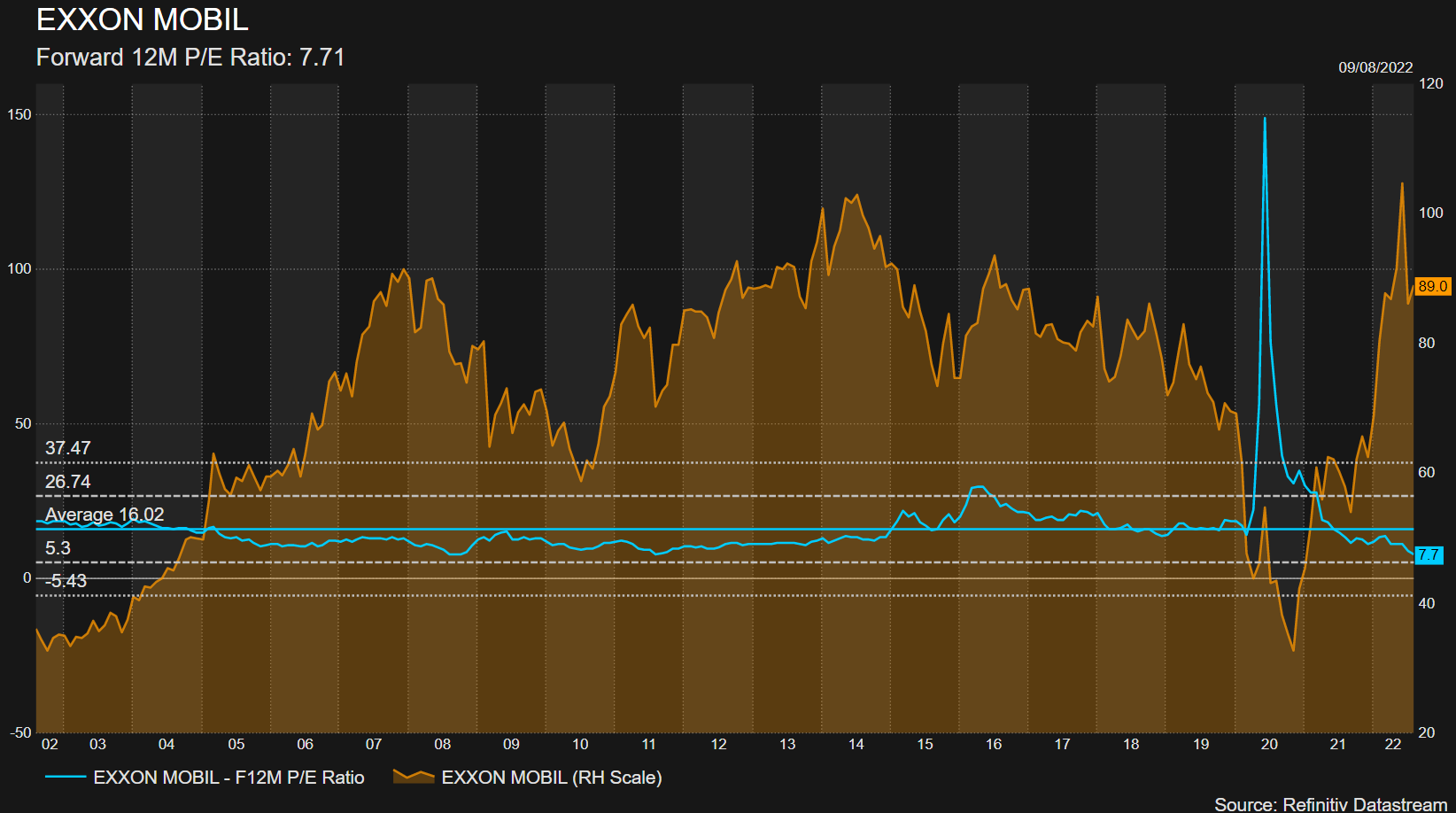

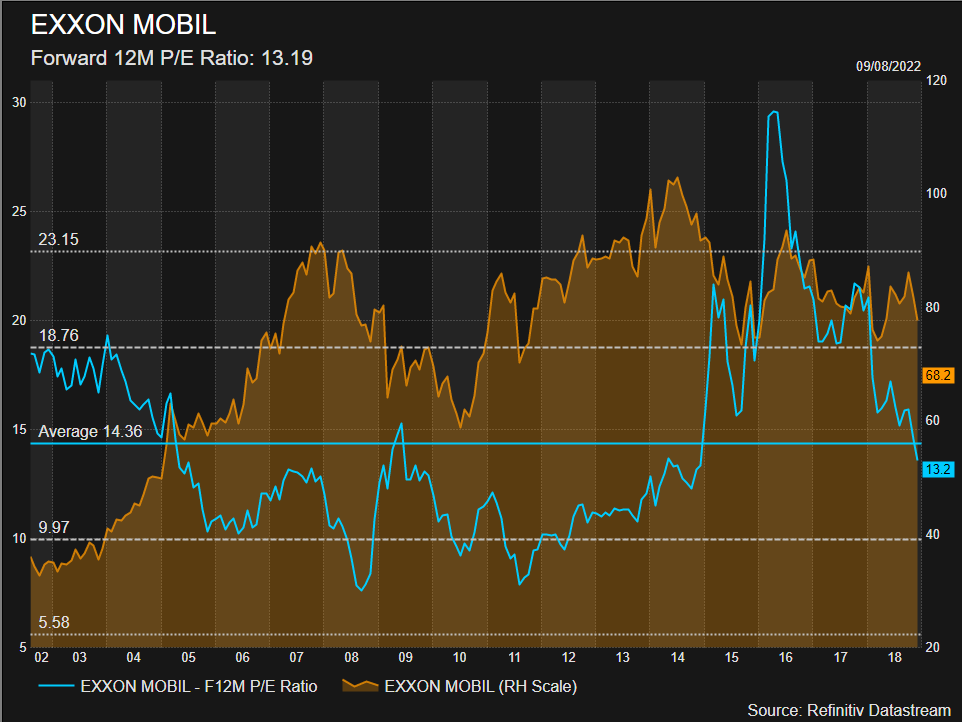

The longer-term view is slightly less bearish though. Oil companies such as Exxon have dramatically reduced capital expenditures on exploration over the past number of years. Searching for new oil and gas sources is notoriously capital intensive. The shift toward greener sources of energy has been supported by governments at the expense of new investments in fossil fuel sources. This has resulted in oil companies instead using surplus cash for massive buyback and dividend programs. There has been little incentive for them to explore. So in a slightly longer time horizon, this is strongly supportive of crude oil prices and hence energy stock prices such as XOM.

The two graphs below show falling investment in exploration for Exxon Mobil, but this is reflected across the entire industry. There simply has been no incentive to explore when governments have been pursuing green energy policies such as wind, solar, etc. Now we are in a global energy crisis, and a shortage of supply will be a key factor supporting long-term oil prices in our view, just not perhaps in the face of an immediate economic slowdown.

Source: Refinitiv

Source: Refinitiv

Recent Exxon Mobil news and earnings

Exxon Mobil reported record earnings on July 29. The surge in oil and gas prices was understandably behind the record-breaking profits. The average price for crude oil given by Exxon in its quarterly results presentation was $107.78. That led to revenues of $115.68 billion for the quarter versus $67.7 billion a year ago. Earnings per share were $4.21 versus $1.10 in the same quarter last year. Exxon naturally increased output in the face of rising prices and demand. Going forward this will likely be a double hit: falling prices and falling demand.

See Also: Walmart Deep Dive Analysis: Hold WMT to play defense vs upcoming US recession

Exxon Mobil forecast and valuation

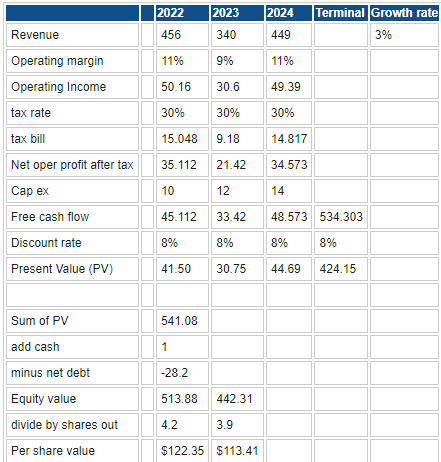

We now go through our valuation scenarios. We have used a traditional discounted cash flow model as well as a relative valuation scheme. For the discounted cash flow, we have assumed margins will fall into 2023 based on inflation, supply chain issues, tanker costs and wages. The cost of production overall should increase in an inflationary environment. We have also forecasted revenue to fall significantly in 2023 based on a global recession with related falling oil demand and oil prices. While this is contrary to what OPEC and other energy agencies are forecasting, we look back at all previous global recessions and fail to find an example where oil demand increased. We have, however, increased revenue versus consensus for 2024 based on what we see as a shortage of oil supply, which should ultimately see oil prices resume their strength in 2024 as the global economy recovers or at least stabilizes.

Source: Refinitiv and FXStreet calculations

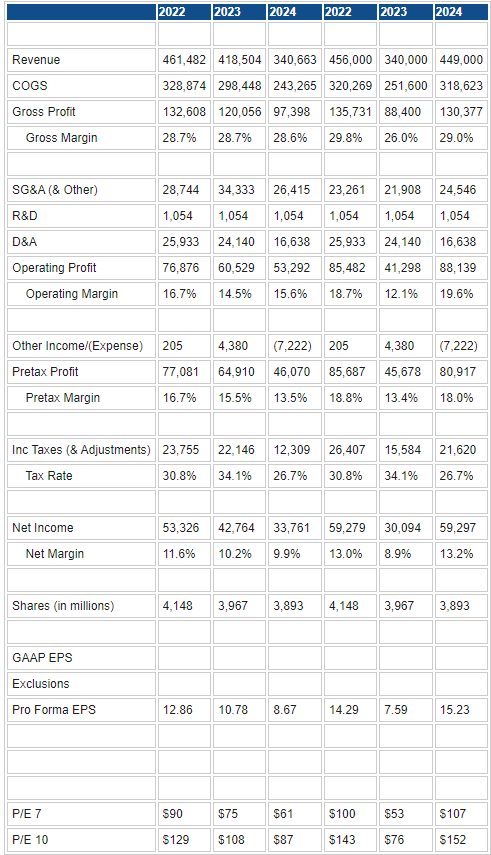

Running the standard discounted cash flow gives us a price target of $122.35, but as this is a 12-month price target, we run with the 2023 estimates and so $113.41. This is also based on the lower share count from continued share buybacks. Using the more common relative valuation below, we again use our lowered revenue projections for 2023. This gives us a worst-case price target of $53. This is based on falling revenue and a price/earnings ratio of 7. This is the bottom of the range and the P/E that XOM traded to during the 2008 crisis. It is significantly below the long-term average of 16. Stripping out the bizarre effects of 2020 when the oil price actually went to $0 for a brief period has skewed this P/E average. The period from 2002 to 2018 gives an average P/E ratio of 13, so as we can see using 7 is overly pessimistic in our view.

Source: Refinitiv and FXStreet calculations

Our price target range, therefore, is set between $76 and $113 based on the two models so far. This gives us an average price target of $94. These figures already take into account our bearish projections for oil prices in 2023 based on a global recession. Essentially, we are attempting to look at the worst-case scenario and adjust now accordingly based on the technical chart.

See Also: Apple Stock Deep Dive: AAPL price target at $100 on falling 2023 revenues

Exxon Mobil technical analysis

We have massive volume-based support at $82. A break of this level would be significant and likely see XOM stock trade toward the $66 support level. Both the Relative Strength Index (RSI) and the Money Flow Index (MFI) are close to overbought levels but have recently stabilized slightly below. Obviously, the trend is strongly bullish, but as we have demonstrated above the main driver has been rising oil prices. XOM made its most recent high in June, which coincided with the last leg higher in oil prices. Most noteworthy is despite record-breaking profits, XOM has not moved toward those June highs and sits some 20% lower. Clearly then the oil price is the driver, not the strong earnings. With earnings likely to have peaked and oil falling, we see this as the peak of the current cycle.

Exxon Mobil (XOM) weekly chart

Executive summary, recommendation and price target

Based on the above, the fair valuation for Exxon Mobil is likely above $100 and would ordinarily warrant a buy rating. However, financial markets are forward discounting and too often stretch like an elastic band too far in one direction before snapping back. Currently, XOM is set to follow the likely move in oil prices lower. This will hit 2023 revenues, and the market will react accordingly. We are more bullish further out into 2024, but we are putting a price target of $94 on Exxon Mobil for the next 12 months. We see near-term risks from falling oil demand to be slightly offset by the prospect of supply constraints due to a lack of investment in oil exploration. This should underpin the longer-term investment thesis. Coupled with the strong cash position, likely buybacks and strong dividends, it does mean we would be inclined to buy any pullbacks. Nonetheless, we see weakness for the medium term and hence our somewhat counterintuitive price target in spite of our valuation models.

Upside risks to our price target

- The global economy does not slow, and oil prices stabilize at current levels.

- Geopolitical turmoil adds to oil supply fears.

Downside risks

- Sever global recession coupled with Chinese economic downturn.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.