BP fails to impress the market, as Fed rate cuts get priced back in

BP has released what it calls its reset, with a renewed focus on oil and gas, reallocated capital and more cost cutting. All of this is aimed at driving shareholder returns in the long term. Unfortunately, this means reduced shareholder returns in the short term, which has triggered a small sell off in the stock price. The shareholder presentation will be delivered later today, but the company had to announce its plans to the LSE earlier this morning.

The highlights from the ‘reset’ include reducing capex spend by $1-3bn compared to 2024 levels, with capex expected to be $15bn this year. The bulk of this spend will be on oil and gas investment projects, with $10bn currently allocated. Net zero/ transition investment has been dramatically slashed to $1.5bn – 2bn, down from the $5bn that was previously announced.

Although there were no new job cuts announced, the plan includes cutting costs by $4-5bn, which is likely to include job losses in the future. These will likely hit non-oil and gas sectors and the energy transition teams. As expected, the company will also make $20bn of divestments over the next 2 years, including Castrol oil, which will go some way to reducing the company’s net debt pile by $14-18bn by 2027.

The company is optimistic for shareholder returns. The guidance included in the reset includes a distribution of 30-40% of operating cash flow over time to shareholders, through share buybacks and what it calls a ‘resilient dividend’ which could rise by up to 4% a year.

The company is also setting a primary target of generating higher returns of more than 16% by 2027 . However, if the company hoped to get a head start on this, it hasn’t worked as yet. The stock has reversed earlier gains and is now down nearly 1% on Wednesday. This could be a reaction to the pledges on shareholder returns: 1, BP has cuts its current share buyback plan and 2, it has failed to give a concrete timeline for when it can deliver shareholder distributions of 30%-40% of free cash flow.

Slashing shareholder returns in the near term could be a tough pill for investors to swallow

In Q4, BP’s share buyback programme totaled $1.75bn, this has been slashed to $0.75-$1bn in Q1. The fact that the company is saying it wants to boost shareholder returns at some point in the future, at the same time as slashing its buybacks for this quarter could be hard for some investors to swallow.

Added to that, for BP to meet its goals of increasing free cash flow and raising returns, it needs a Brent crude price of $70 per barrel or more, the Brent price is currently just above $73 per barrel, which may be too close for comfort, which may also curb investor enthusiasm for this stock.

BP’s timing is wrong, yet again

The problem for BP is that it flip flopped away from net zero and back to oil and gas too late. Added to this, the reset could not come at a worse time, when the price of oil is falling. The key event will not be the presentation from BP CEO Murray Auchincloss, but the judgement from Elliott Management, the activist investor who has built a near 5% stake in BP and is threatening to oust management if the company does not pivot back to oil and if performance does not improve. Its Elliott’s time scale that really matters for BP, and whether the investor will give the company time to see if its reset will work.

For now, the reaction to the reset has been tepid, and we do not think that this alone can boost the share price or narrow the valuation gap with its peers.

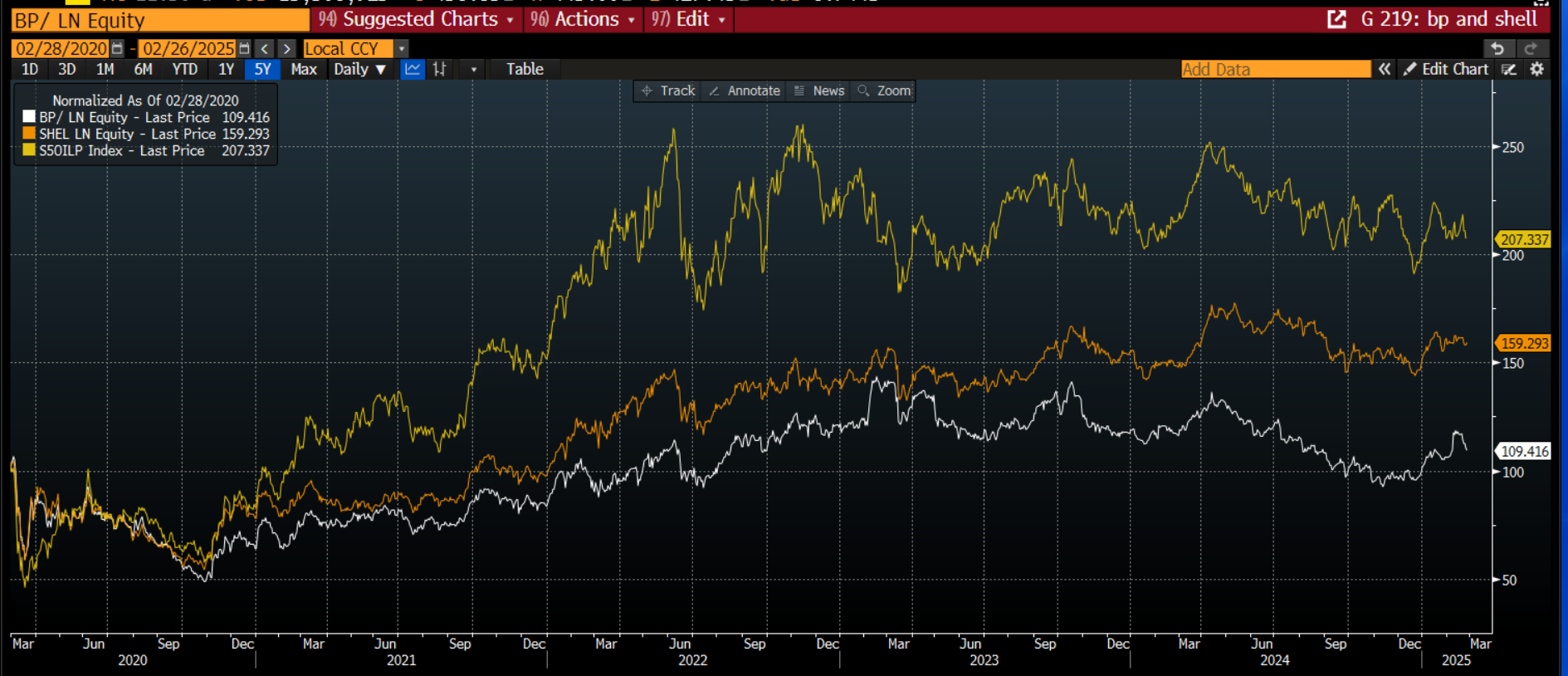

Chart: BP, Shell and S&P 500 Oil and Gas sector, normalized for five years

Source: XTB and Bloomberg

US economic weakness: Focus on rate cuts and FX so far, but could stocks be next?

Elsewhere, there has been a turnaround in US Fed rate cut expectations. As economic data has surprised on the downside, the market has priced in more rate cuts by the Fed by year end. The market now expects US interest rates to end the year at 3.78%, this is the lowest level of the year so far. The market is now expecting just over 2 rate cuts from the Fed this year. There is now a 50% chance of a rate cut in July, a month ago it was 42%. Added to this, there is also a 36% chance of two rate cuts by October, this was 26% a week ago. The increase in Fed rate cut expectations explains the weakness in the dollar. The USD is the weakest performer in the G10 FX space so far this year, especially vs. the yen.

The weakness in the economic data has played out in the FX market and in the interest rate futures market. Although US stock markets have underperformed European markets, they are still higher on the year. If weakness in US economic data accelerates, stocks could be next to come under downward pressure. However, it’s worth remembering that most US blue chip and mid cap stocks have international exposure, and this could protect them from a domestic US economic downturn, which explains US stock market outperformance relative to other US assets.

Author

Kathleen Brooks

XTB UK

Kathleen has nearly 15 years’ experience working with some of the leading retail trading and investment companies in the City of London.