![]() Ryan Miller

Ryan Miller

Ryan Miller Trading Economics

It is a prevalent notion that low interest rates imply money is loose and high interest rates imply money is tight. In theory, it makes sense, because it allows investors to borrow at cheaper rates, which frees up more cash that would otherwise be spent servicing debt payments on loans with higher rates. The less you have to pay back, the more you are inclined to borrow. The more you borrow, the more spending power you have, which is likely to find its way into the real economy. So, on paper, low rates certainly feel like stimulus. But, let’s take a closer look.

If cutting interest rates provides stimulus to the economy, how long would we have to wait for the economy to actually be stimulated? One year? Two years? Three years? How about thirteen years? We are on year number thirteen since the Global Financial Crisis, and still, we live in a deflationary environment. How could that be? There have been multiple rounds of Quantitative Easing (QE), trillions of newly “printed” dollars, all the while, we are stuck in a low interest rate environment. Certainly after thirteen years of on-and-off stimulus, accompanied by low rates, inflation and economic growth would have prevailed by now, right? Perhaps, low rates mean money is tight, not loose, like mainstream economics suggest.

During the Great Depression, which was a significant period of deflation, rates fell to near zero and stayed there until after WWII. During the inflationary 1970’s, when money was extremely loose, rates ran up into the high double digits, alongside inflation. This period was followed by the disinflation of the 1980’s, when rates fell roughly 70% from their peak in 1981. Now, here we are post-2008, in another deflationary environment, with low rates. If these periods of time aren’t proof that low rates mean money is tight and high rates mean money is loose, then I don’t know what is. Yet, it is still the mainstream consensus that low rates equals stimulus.

When money is loose, borrowing and spending picks up, and we see growth in the economy. As this happens, risk premiums rise. If I’m an investor and risk premiums are rising, then rates on safe investments need to rise too. If I am going to loan money by purchasing a bond, I demand a higher rate of return due to the opportunity cost of not investing in a riskier asset, otherwise I won’t be willing to lend. The opposite holds true during periods of flat or sluggish growth (like the one we’re currently in). Risk premiums are low, so there is no opportunity cost. I am willing to accept a lower rate when I lend money in this environment.

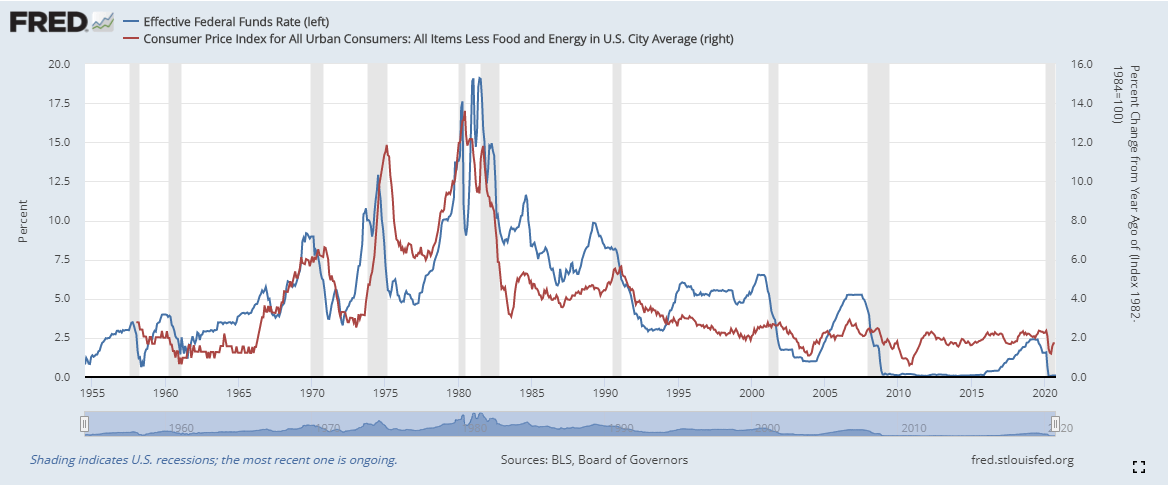

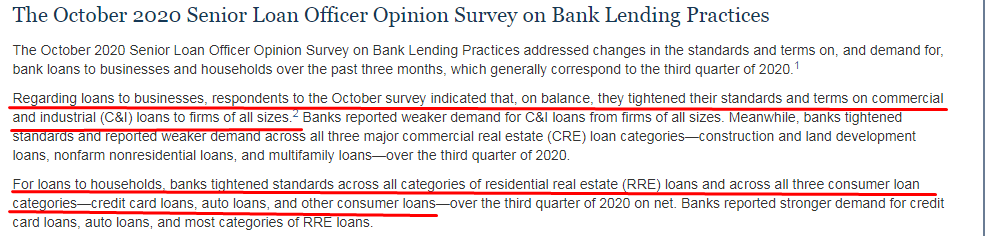

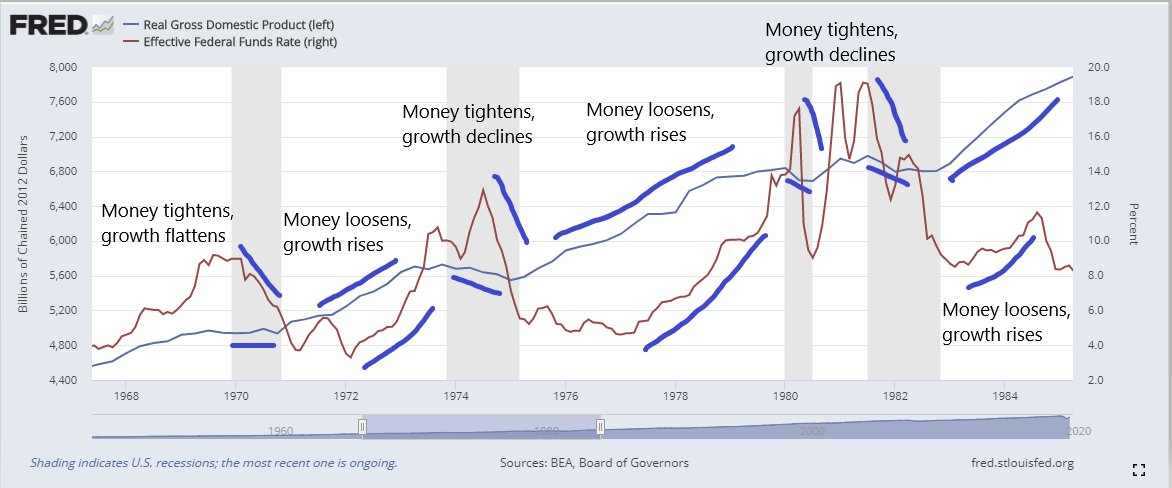

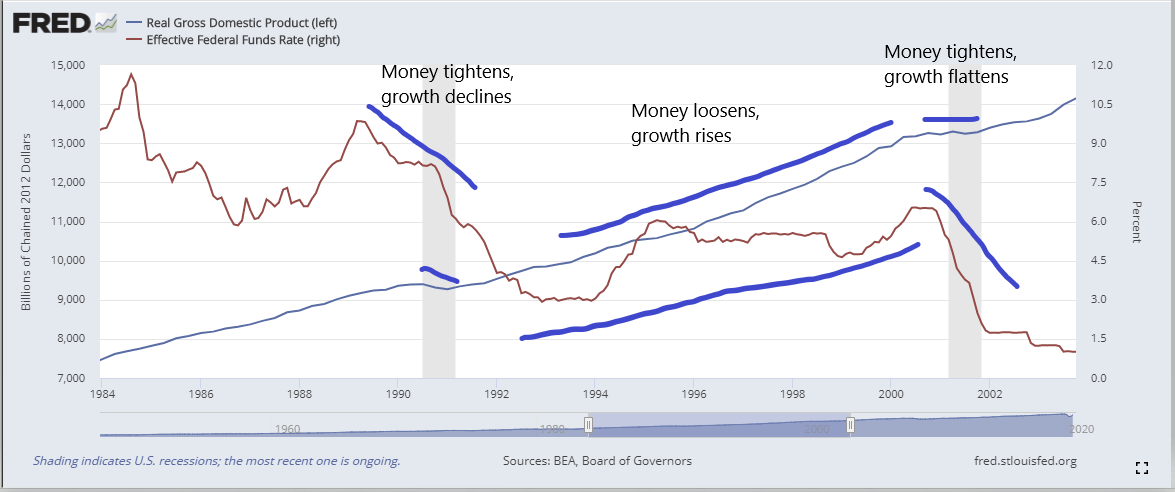

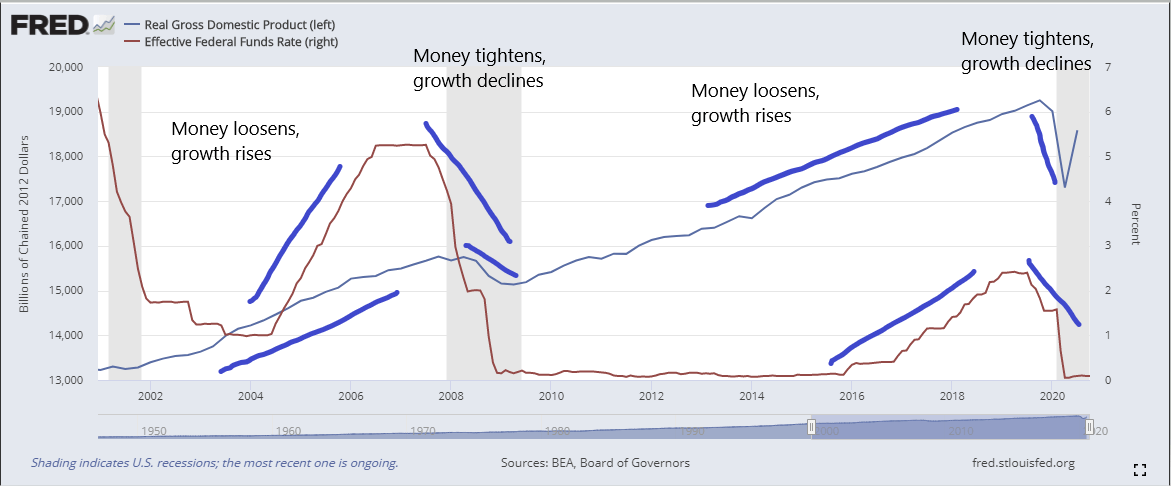

If you look below at EFF (effective federal funds rate) and CPI (consumer price index), you can clearly see the positive correlation that exists between interest rates and inflation. As rates rise, inflation rises and as rates fall, inflation falls. The late 70s, early 80s was the end of the inflationary period and rates and inflation hit nearly 20%. How could it be that inflation was so high during a time of high interest rates? Now compare post-2008 to today, interest rates are near zero and inflation is very low by historical standards. In the second picture below I have the Senior Loan Officer Opinion Survey on Bank Lending Practices which was released on Monday, by the Fed. Here we are in a low interest rate environment and banks are tightening up their lending standards, further indicating money is tight. In our current environment, banks are willing to accept a low rate on their lending, but are only willing to let the most creditworthy borrowers, borrow. So, despite interest rates being low, money is hard to get your hands on, which is why banks hoard safe, liquid assets like US Treasuries during these times. Mainstream economics tells us that the phenomena I am suggesting isn’t possible because high rates mean money is tight and low rates mean money is loose. But all of the evidence points to the contrary.

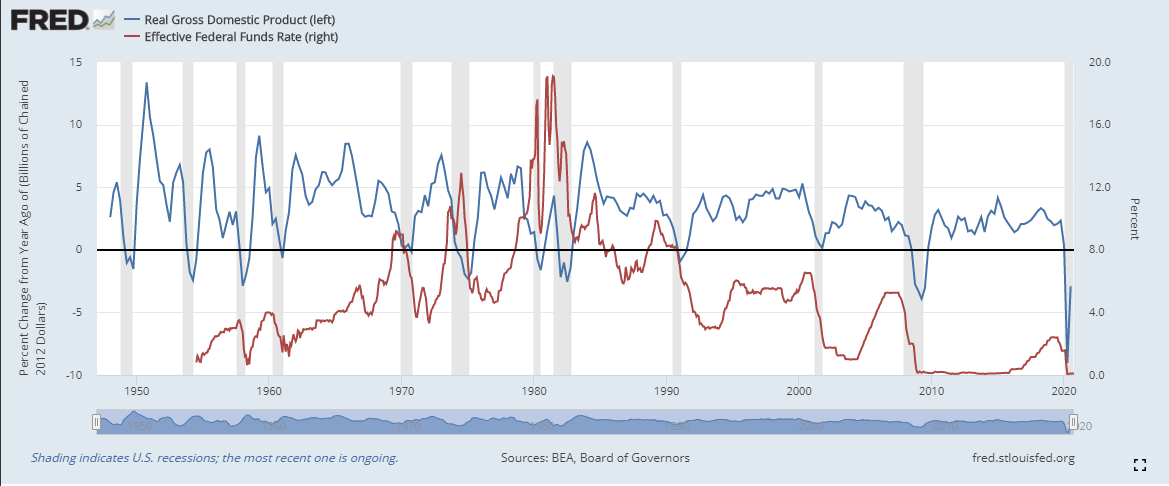

Now, let’s take a look (below) at the relationship between rates and growth. I used the percent change from one year ago on the Real GDP so you can see on a more granular level the relationship between GDP and interest rates. Again, similar to inflation, there is a very strong positive correlation between growth and rising rates. When money is tight (indicated by low rates), GDP will often decline or flatten out.

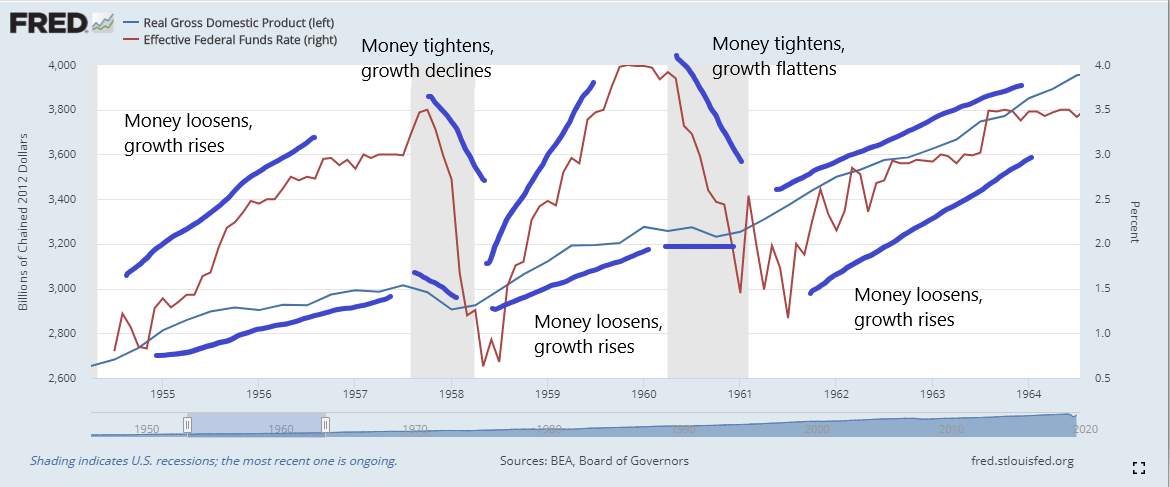

See below, I have four charts going back to the 1950s that show when money is loose (rising rates), we see positive GDP growth. When money is tight (falling rates) we see negative or flat GDP growth.

When money is tight, we do not see positive growth. We see growth when money is loose, which just so happens to be in a high or rising interest rate environment. When money is loose, investors and banks don’t want or need to hold on to safe, liquid assets because capital is easy to get their hands on. In such cases, investors and banks put their money into riskier assets and lending in search of higher rates of return. So, don’t be fooled when central bankers talk about rates staying low for the foreseeable future, because what that means is money is tight, there is no inflation or growth on the horizon, and whether they realize that or not, I’m not sure. Low rates may “stimulate” the economy for a very short time period, but once the illusion of ‘low rates equals stimulus’ wears off, everything rolls back over. Milton Friedman said it best, so, I will leave you with a quote of his: “after the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die.”

There is substantial risk associated with trading in the financial markets. You are solely responsible for your own financial decisions. Information on Ryan Miller Trading Economics is for educational purposes only. Ryan Miller Trading Economics will not be held responsible for any losses you incur. Ryan Miller Trading Economics does not provide any trading advice and is not a professional investment service. Past performance is not necessarily indicative of future results. There is a substantial risk of loss associated with trading currencies, securities, options, futures, equities and options on futures and currencies. Currencies, Futures, Options, Bonds, Equities and other securities trading all have large potential rewards, but they also have large potential risk and may result in monetary losses. You must be aware of the risks and be willing to accept them in order to invest or trade in these markets. Ryan Miller Trading Economics is neither a solicitation nor an offer to Buy/Sell currencies, futures, options, bonds, or equities. No representation is being made that any account will or is likely to achieve profits or losses similar to those discussed on this website. The past performance of any trading system or methodology is not necessarily indicative of future results.

Editors’ Picks

EUR/USD off highs, back to around 1.1900

EUR/USD keeps its strong bid bias in place despite recedeing to the 1.1900 zone following earlier peaks north of 1.1900 the figure on Monday. The US Dollar remains under pressure, as traders stay on the sidelines ahead of Wednesday’s key January jobs report, leaving the pair room to extend its upward trend for now.

GBP/USD hits three-day peaks, targets 1.3700

GBP/USD is clocking decent gains at the start of the week, advancing to three-day highs near 1.3670 and building on Friday’s solid performance. The better tone in the British Pound comes on the back of the intense sekk-off in the Greenback and despite re-emerging signs of a fresh government crisis in the UK.

USD/JPY bounces off lows, back above 156.00

USD/JPY is starting the week markedly on the defensive, sliding back toward the 155.50 area where it has met some decent contention for now. The move lower in spot follows FX intervention chatter after PM S. Takaichi scored a landslide win in Sunday’s election..

Editors’ Picks

EUR/USD off highs, back to around 1.1900

EUR/USD keeps its strong bid bias in place despite recedeing to the 1.1900 zone following earlier peaks north of 1.1900 the figure on Monday. The US Dollar remains under pressure, as traders stay on the sidelines ahead of Wednesday’s key January jobs report, leaving the pair room to extend its upward trend for now.

USD/JPY bounces off lows, back above 156.00

USD/JPY is starting the week markedly on the defensive, sliding back toward the 155.50 area where it has met some decent contention for now. The move lower in spot follows FX intervention chatter after PM S. Takaichi scored a landslide win in Sunday’s election..

Gold picks up pace, retargets $5,100

Gold gathers fresh steam, challenging daily highs en route to the $5,100 mark per troy ounce in the latter part of Monday’s session. The precious metal finds support from fresh signs of continued buying by the PBoC, while expectations that the Fed could lean more dovish also collaborate with the uptick.

Crypto Today: Bitcoin steadies around $70,000, Ethereum and XRP remain under pressure

Bitcoin hovers around $70,000, up near 15% from last week's low of $60,000 despite low retail demand. Ethereum delicately holds $2,000 support as weak technicals weigh amid declining futures Open Interest. XRP seeks support above $1.40 after facing rejection at $1.54 during the previous week's sharp rebound.

Japanese PM Takaichi nabs unprecedented victory – US data eyed this week

I do not think I would be exaggerating to say that Japanese Prime Minister Sanae Takaichi’s snap general election gamble paid off over the weekend – and then some. This secured the Liberal Democratic Party (LDP) an unprecedented mandate just three months into her tenure.

RECOMMENDED LESSONS

Making money in forex is easy if you know how the bankers trade!

I’m often mystified in my educational forex articles why so many traders struggle to make consistent money out of forex trading. The answer has more to do with what they don’t know than what they do know. After working in investment banks for 20 years many of which were as a Chief trader its second knowledge how to extract cash out of the market.

5 Forex News Events You Need To Know

In the fast moving world of currency markets where huge moves can seemingly come from nowhere, it is extremely important for new traders to learn about the various economic indicators and forex news events and releases that shape the markets. Indeed, quickly getting a handle on which data to look out for, what it means, and how to trade it can see new traders quickly become far more profitable and sets up the road to long term success.

Top 10 Chart Patterns Every Trader Should Know

Chart patterns are one of the most effective trading tools for a trader. They are pure price-action, and form on the basis of underlying buying and selling pressure. Chart patterns have a proven track-record, and traders use them to identify continuation or reversal signals, to open positions and identify price targets.

7 Ways to Avoid Forex Scams

The forex industry is recently seeing more and more scams. Here are 7 ways to avoid losing your money in such scams: Forex scams are becoming frequent. Michael Greenberg reports on luxurious expenses, including a submarine bought from the money taken from forex traders. Here’s another report of a forex fraud. So, how can we avoid falling in such forex scams?

What Are the 10 Fatal Mistakes Traders Make

Trading is exciting. Trading is hard. Trading is extremely hard. Some say that it takes more than 10,000 hours to master. Others believe that trading is the way to quick riches. They might be both wrong. What is important to know that no matter how experienced you are, mistakes will be part of the trading process.

The challenge: Timing the market and trader psychology

Successful trading often comes down to timing – entering and exiting trades at the right moments. Yet timing the market is notoriously difficult, largely because human psychology can derail even the best plans. Two powerful emotions in particular – fear and greed – tend to drive trading decisions off course.