The New Silk Road: A special report

When the first caravans carrying Chinese silks arrived in ancient Rome, it set off a female fashion craze. The wives of senators and generals had never felt or seen anything so lustrous. Like the Chinese elite, they adopted the material as a symbol of wealth and status, embroidered silk robes with gold and wore them to the grave.

China announced a Digital Silk Road (DSR) in 2015 with a white paper that described a range of technology and communications projects. But it wasn’t obvious what, if anything, would play the role of silk. Now it’s clear that just as threads spun from the pupae of silkworms drove the growth of a global trade network, China’s digital yuan may weave an international system of finance. The first inroads have already been dug: Developing economies have adopted the yuan as their own, and wealthier economies in Asia and beyond are exploring their own fiat digital currency, whether they like it or not, to stay competitive with China.

“[Government leaders] are looking for the light at the end of the tunnel and the train is the light; it’s coming right at them,” said Don Tapscott, executive chairman of the Toronto-based Blockchain Research Institute. The stakes are high, with implications for everything from financial privacy to the global balance of power. “If China wins with its central bank digital currency, they’ll roll it out across … Africa, into Southeast Asia,” he said. “The [yuan] becomes the currency of record and that’s the end of the American hegemony in the world.”

Faster, cheaper money

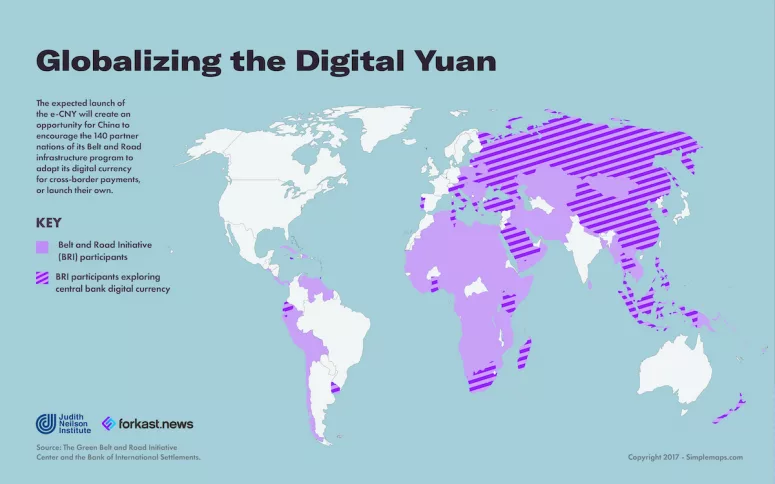

The DSR is an essential component of China’s global infrastructure plan, the Belt and Road Initiative (BRI), announced in 2013. A project of staggering scope — though without much transparency — the BRI is China’s estimated trillion-dollar down payment in development and investment initiatives that span the transcontinental routes of the original silk road from Asia to Europe and the maritime shipping lanes that displaced them in the late 18th-century. By China’s count, 140 countries have signed on.

From a project management perspective, the BRI and DSR have one major headache in common: contending with outdated and often ineffectual banking systems. Beijing sees the digital yuan as a solution to this problem as well as a way to mutually reinforce the reach of both projects, said Stanley Chao, president of a Los Angeles-based firm that consults on Asian business strategies.

“In emerging markets with poor banking systems, it can take a week to clear transactions, slowing everything down and causing delays,” he said. “China sees a digital currency as a solution. Payments will be instantaneous. Transaction fees will be almost down to zero because you have no middle man.”

“At some point, I could see China making trade pacts where it said, ‘Let’s do one currency. We’ll save a lot of money on transaction fees, no third-party banking system,’” said Chao. “There are countries, not only in Asia, but in Africa, Eastern Europe and South America, that might jump at the idea.”

The conjecture is already a reality. In December 2019, to facilitate a US$54 billion project known as the China-Pakistan Economic Corridor, Pakistan announced the yuan as its new second national currency—a role long occupied by the dollar. Six months later, Turkey Telekom agreed to use yuan for import payments.

In China’s view, the digital yuan would fuel a virtuous cycle: The more countries see the benefits of settling accounts in yuan, the greater the network effect in further expanding the orbit of Chinese economic influence.

Between 2000 and 2015, China’s trade settlement in yuan increased from roughly zero to US$1.1 trillion, according to the National Bureau of Asian Research, close to a third of the country’s total trade. But even by 2021, only 2.5% of international payments worldwide were transacted in yuan, according to the CSIS China Project, compared to 39% in the U.S. dollar and 36% in the euro. That leaves the yuan with considerable room to grow.

(Forkast News)

Peer pressure

For many countries, developing their own fiat digital currency is more appealing than adopting China’s. According to a January 2021 survey by the Bank of International Settlements — the central bank of central banks — 86% of its 65 members are exploring the idea; 60% have begun experiments; and 14% have pilots underway.

This interest is shared among economies of every size and state of development. In October 2020, the Bahamas announced the arrival of the “sand dollar,” a CBDC pegged to the U.S. dollar. That same month Cambodia launched the digital bakong, describing it as a “hybrid CBDC” that supports transactions in both the Cambodian riel and U.S. dollar. Indonesia’s central bank governor confirmed in May that Southeast Asia’s largest economy would launch a digital currency. And South Korea is preparing its CBDC for a pilot test in August. Meanwhile, Singapore recently completed a five-year experiment in blockchain-based financial architecture. One of the prongs involved a cross-border payment model developed with U.S. banking giant JPMorgan and Singapore global investment firm Temasek.

“China’s CBDC was really creating some peer pressure here in the region,” said Charles d’Haussy, Asia managing director of Consensys, a blockchain software firm that is working on CBDC projects for the central banks of Australia and Hong Kong. “It’s a big shift in the industry [that] shows there is institutional and regulatory adoption.”

Even as they move forward, however, some central banks have expressed reluctance, aware that they are being forced to chase China’s lead.

In a March 2021 speech at an annual tech summit co-hosted by the Nikkei, Bank of Japan Governor Haruhiko Kuroda described the digital yen as an obligation more than a choice. “Central banks share the view that it is not an appropriate policy response to start considering CBDC only when the need to issue CBDC arises in the future,” said Kuroda. He also reiterated that the bank had no plans to issue a digital yen.

If Japan feels that it is being dragged into the digital age of money, it is not alone. Ten years ago, India was considered an economic and political competitor to China. But even with an economy expected to be the world’s third-largest by 2030, India has failed to keep technological pace with its regional rival.

Despite having world-class technology universities and a large pool of elite programmers, India has generally followed China’s hostility to private cryptocurrencies like Bitcoin but without also adopting its embrace of blockchain as an infrastructure of the future. India nonetheless recognizes the network effect in play and has recently — and ambivalently — stepped into the brave new world of government-backed digital currency.

In the span of a single week this past February, the Reserve Bank of India released a report stating that CBDC “poses a risk of disintermediation of the banking system,” followed a few days later by the bank’s governor publicly acknowledging the digital rupee is “receiving our full attention.”

“Now that China and other nations are talking about central bank digital currency, India is also definitely motivated,” said Nischal Shetty, founder and CEO of WazirX, one of India’s largest cryptocurrency exchanges. He speaks widely on related regulatory issues. (In June, Indian authorities notified Shetty that it was investigating the use of WazirX for money laundering.) He said the competition between India and China in CBDC is healthy. “I want more countries around the world to experiment with [CBDCs] so that every other nation is motivated to participate,” he said. Shetty predicts India will have made substantial progress in a CBDC within two years.

The rapid move by central banks toward the development of CBDCs raises the question: How will the digitization of cross-border transactions and settlements impact the role of SWIFT, the dominant global network for interbank transaction communications that has been at the center of global currency flows since 1973?

This past February, four central banks took a first step toward deploying their digital currency in cross-border trade without using the SWIFT system as an intermediary. They announced a pilot project, called m-CBDC, or multiple CBDC, that amounts to a transactions bridge among the central banks of China, Hong Kong, Thailand and the UAE. The trial — intended to identify technical and regulatory pain points in commercial digital currency transactions — is being closely watched by governments everywhere.

“This is the first time you are seeing four different central banks working on building a shared infrastructure to go cross-border,” said d’Haussy. “It’s probably the most ambitious proof-of-concept in terms of digital currencies in 2021, after China’s retail digital yuan.”

Three months after the m-CBDC announcement, SWIFT released a joint discussion paper with consulting firm Accenture on how it could accommodate cross-border CBDC payments and, the subtext suggested, remain relevant. Touting that it is “neutral and currency agnostic,” SWIFT contended that “there is little advantage in reinventing the wheel.”

If anything, reinventing the wheel appears very much to be the point. “Using a new type of money in old pipes will probably not bring all the value proposition of digital assets,” said d’Haussy. “When you reinvent money, it’s a good opportunity to rethink the world ecosystem.”

As it happens, this is exactly what concerns the United States, the country with the most to lose from a diminution of SWIFT’s role in the global financial order. Part Three will examine how power and privacy may change with the new money.

Author

CoinDesk Analysis Team

CoinDesk

CoinDesk is the media platform for the next generation of investors exploring how cryptocurrencies and digital assets are contributing to the evolution of the global financial system.