Yen finds a bid as Sterling weakens

GBPJPY, H1

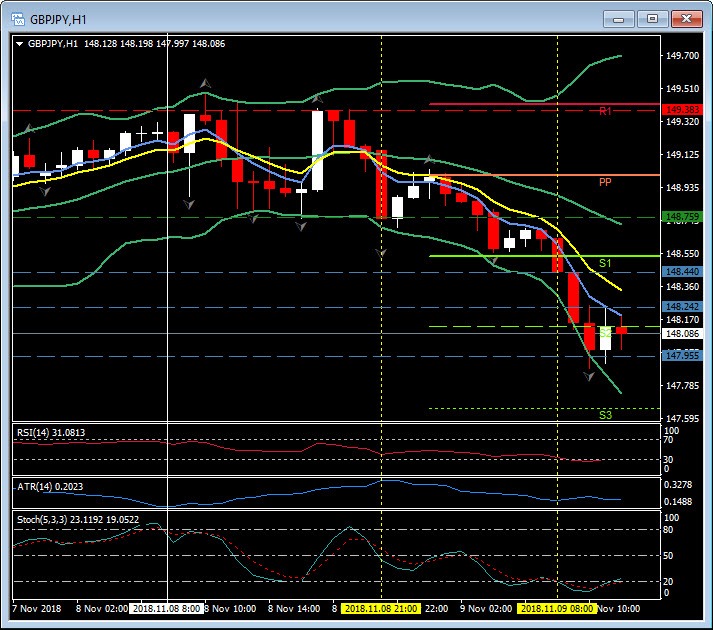

The Yen was in demand during the Asian session and this has followed through to the European session. USDJPY traded below 113.75 from an overnight high of 114.07, with both EURJPY and GBPJPY falling below S2 to 128.92 and 147.88, respectively. The raft of UK data this morning (see below) was far from inspiring but it has stalled the fall in Sterling as GBPUSD rose back over the key 130.00 and GBPJPY regained 148.00.

UK Q3 GDP rose 0.6% q/q, as expected in preliminary data, and by 1.5% in the y/y comparison. The q/q expansion was the quickest q/q rate since the final quarter of 2016. Most of the quarterly gain was driven by a strong m/m increase in July, while there were signs of weakness in September, with slowing retail sales and a decline in car purchases, though a decline in car imports led to an improvement in the trade deficit. Quarterly growth was mainly driven by the service sector, contributing 0.33 percentage points to the headline, while the manufacturing sector returned to growth after two consecutive quarters of negative growth, although only contributing 0.06 percentage points to GDP. Construction posted its biggest quarterly growth since Q1 2017.

UK September industrial production came in near expectations at flat growth for both the m/m and y/y comparisons. For Q3, industrial output rose 0.8% q/q, driven primarily by a 0.6% rise in manufacturing. In September trade data, the visible deficit improved to GBP 9.7 bln from a deficit of GBP 11.7 bln in August. A decline in car imports drove the improvement. The total trade deficit narrowed GBP 3.2 bln to GBP 2.9 bln, with goods exports increasing GBP 5.0 bln versus the GBP 2.1 bln rise in goods imports.

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c