Why we still expect a Bank of England rate cut in August

The UK inflation story is looking better despite some recent upside surprises in services. Thursday’s meeting looks like a close call, but we’re sticking to our long-held base case that the Bank will indeed cut rates then.

Markets are on the fence about an August rate cut

We’re a week out from the next Bank of England meeting and investors reckon a rate cut is a 50:50 call.

The logic is simple enough. Two out of the nine-strong committee have already started voting for rate cuts. Two, maybe three, take the opposite view and are visibly resistant to cuts. That leaves four or five in the middle who appear torn. June’s meeting revealed that some - perhaps most - of those officials thought that decision was finely balanced. But apart from that, we’ve heard next to nothing from those policymakers since the general election was called in late May.

That lack of commentary makes it hard to make a strong conviction call about Thursday’s meeting. But we’re sticking with our long-held base case that we will get a rate cut in August.

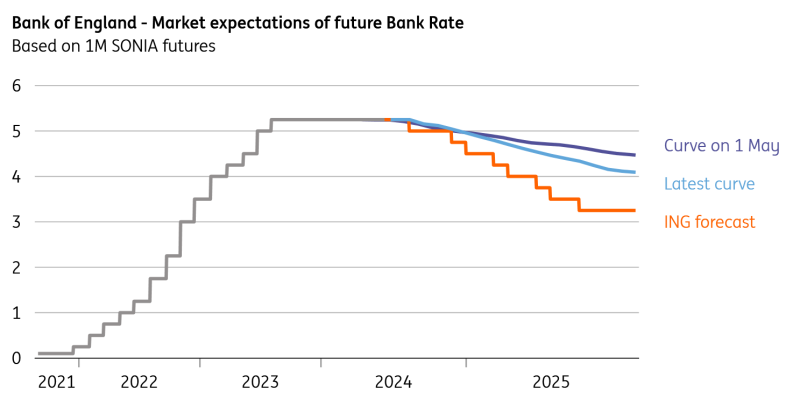

We expect more rate cuts this year and next than the market

Source: Macrobond, ING calculations

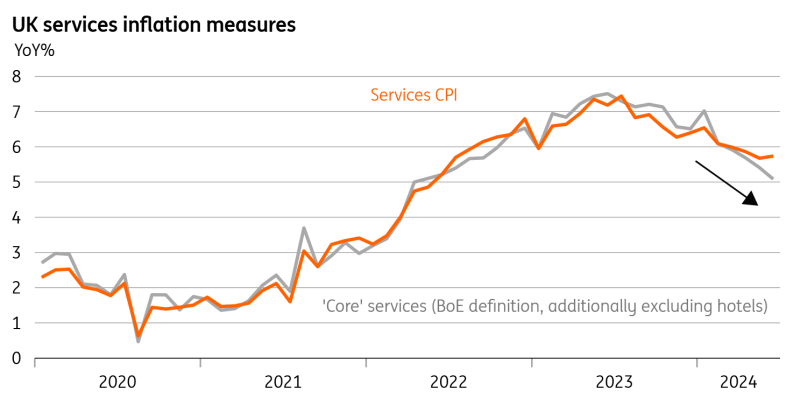

Services inflation isn't as bad as the headlines suggest

There are two questions BoE officials need to answer.

Firstly, does the recent upside surprise to services inflation tell us anything about where it’s likely to be in 1-2 years’ time? We don’t think it does.

And secondly, does the recent improvement in UK growth point to a renewed rise in price pressure down the line? Again, we think the answer is no.

So let's start with services inflation – the guiding light for BoE policy right now – and the story doesn’t look great at first glance. It stood at 5.7% in June, only slightly below readings from earlier in the year and critically, well above the BoE’s 5.1% forecast. It’s also considerably higher than elsewhere in Europe.

But a lot of this looks like noise. Take April’s data, which saw much chunkier annual contract-linked price hikes than many had expected. It was a very similar story back in 2023. Those increases can’t be totally ignored, but they are inherently backward-looking. They’re often directly linked to past and more elevated rates of headline inflation. Just think about your phone or internet bills.

More recently, services inflation has been propped up by a spike in hotel prices. Drilling into the data reveals that this was caused by just two hotels that more than doubled their prices in June. The achieved sample size of hotel prices was also lower than usual.

Without hotels, services inflation would have fallen to 5.5% rather than sticking at 5.7% in June. If we take that exclusion process further, it would be lower still. The Bank of England likes to look at a custom measure of “core services” inflation which, in its most recent iteration, excludes rents, package holidays, airfares and education. The logic here is that these items are either highly volatile or don’t tell us much about the future persistence of inflation.

We’ve calculated that Bank of England metric, and additionally removed hotels. And what it shows is that “core services” inflation has fallen more aggressively this year and was at 5.1% in June, directly in line with the Bank’s most recent forecast for overall services CPI.

BoE's measure of "core" services inflation has fallen more sharply

In the May Monetary Policy Report, the BoE presented a measure of services inflation that excludes rents, package holidays, air fares and education. We have additionally excluded hotels here, given recent volatility.

Source: Macrobond, ING calculations

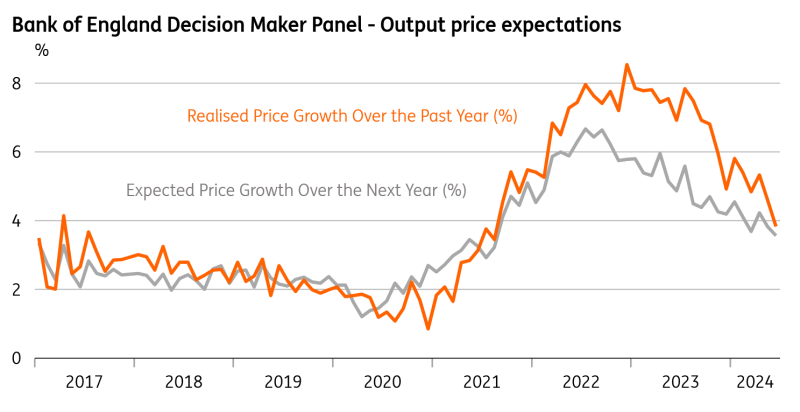

Pricing surveys point to less aggressive inflation

You’d be forgiven for thinking this sounds a bit dubious. If you remove all the inconvenient stuff from the basket, then it’s not exactly surprising that you end up with a more flattering inflation rate. But there is some logic in doing so. For instance, rents make up 16% of the services basket, and the link between the recent inflation spike and the health of the wider economy or jobs market is not so obvious right now.

If you’re still sceptical, then just remember that the Bank of England itself has been promoting this measure as a gauge of underlying price pressures in the economy. It’s a fair bet that this sort of chart will have been presented to officials ahead of the meeting next week.

This more dovish interpretation of the recent CPI numbers is also supported by surveys that show firms are raising prices and wages much less rapidly. The Bank of England’s survey of Chief Financial Officers, its Decision Maker Panel, has consistently shown just that.

Admittedly that has been true for a while, and BoE hawks used to make the point that firms were making a habit of saying one thing on pricing and doing quite another. Survey data on ‘realised’ price growth consistently exceeded what the same firms were saying they expected to do with prices in future months. But that’s no longer the case, as the chart below demonstrates. And it’s a very similar story if you look at the latest services PMI data on pricing.

Firms are raising prices less aggressively than they were

Source: Macrobond

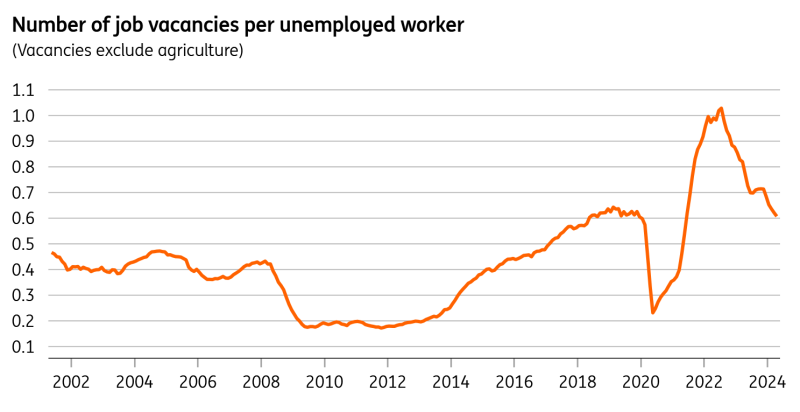

The recent improvement in UK growth shouldn't derail rate cuts

It’s exactly this sort of data that’s helping the Bank to become more confident in its inflation forecasting ability. And that’s enabling officials to more confidently look through some of the recent upside surprises on services inflation and take a more forward-looking view.

It also argues against putting too much emphasis on the recent improvement in economic growth. After strong growth in the first half of the year, the UK economy was probably more than half a percent larger as of the second quarter than the Bank of England had forecast just three months ago.

But does this herald a fundamental rethink on where inflation goes next? We suspect not. Growth is improving mainly because real wages are recovering. That’s ultimately a short-term cyclical story. And importantly it’s coinciding with a further cooling jobs market. Vacancies are almost back to pre-Covid levels and the unemployment rate is rising in line or even slightly faster than BoE forecasts. Central bankers, not just in the UK, are becoming visibly wary that these signals risk meaning they've been too late with rate cuts.

The vacancy-to-unemployment ratio is back at pre-Covid levels

Source: Macrobond, ING calculations

Some of the recent economic recovery can also be traced back to expectations of imminent rate cuts. And decent growth for the rest of 2024 relies, in part, on those cuts being delivered, a fact that won't have been lost on BoE officials. Remember that the passthrough of higher rates has been more rapid in the UK relative to some other parts of Europe or, indeed, the US.

The bottom line is that there is just about enough in the recent data to give the Bank confidence to begin lowering rates. Governor Andrew Bailey said back in May that the Bank could cut rates faster than markets expect, and we suspect he and a majority of committee members would prefer to get the job started next Thursday. We expect a total of three rate cuts this year.

Read the original analysis: Why we still expect a Bank of England rate cut in August

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.