Why a quick recession is the most plausible scenario for the markets?

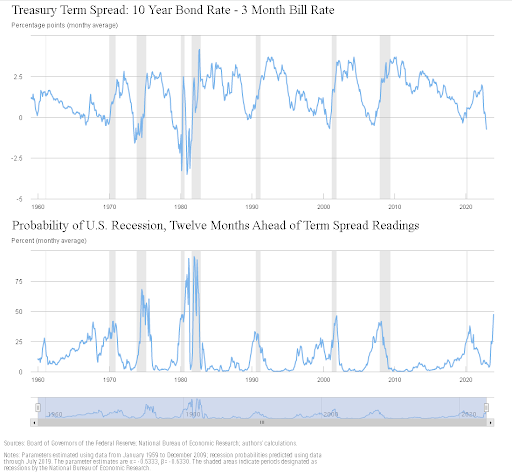

It is not a secret that for a very long time widely respected economic models and indicators have been pointing towards an oncoming recession for the US sometime within the next several quarters. One of the most recognizable indicators for potential oncoming recessions is the slope of the yield curve, or “term spread”. The model utilizes the term spread between the 10-year Bond Rate and the 3 Month Bill rate. New York FED calculates the probability of the US economy sliding into recession within the next 12 months as close to 50 percent.

Clearly, this probability is higher than what it was before the 2001 (Dotcom) and 2008-09 (Global Financial Crisis) recessions loomed, only surpassed by the infamous oil shock in the 1970s (stagflation) and the inflation and interest rate hike spiral (Volker’s Bear market) in early 1980s. The quick come-quick-gone recession of 2020 was also estimated beforehand with a significantly lower chance from the same model.

However, the markets seem unfazed by the risk of an oncoming recession especially judging the performance of risk assets including commodity prices. This seems confusing for a number of reasons. Theoretically, the sizeable negative term spread (which means the 10-year bond has a lower rate than the 3-month bill rate) implies that inflation is expected to slow considerably in the near future due to the hawkish FED and the tightening cycle it is currently overseeing. This sound good on its own right but it spells doom for lending and investment activity because in such times firms will have a very hard time finding loans for their expansion plans and long-term investments. Also, the positive real short-term rates encourage saving for the consumers who rest assured that slowing inflation will enable their savings to buy more goods and services in the future.

This undesirable balance is inevitable when the current inflation is high and the FED has convinced the markets (and households as well) that inflation will come down. The usual mode of business will return once the short-term rates recede to levels close to the FED’s inflation objective of at around 2-2.5%. The quickest way to reach this equilibrium is to experience a harsh but (hopefully) quick recession that brings both annual inflation prints and FED funds rate considerably.

This week’s slew of PMI numbers was mostly better than consensus expectations. However, almost no PMI can be found exceeding the 50.0 threshold. Especially S&P Global US Services underlines a decelerating economy albeit the monthly contraction was less severe than forecasts. Furthermore, January data releases cost burdens were increasing for private firms than what they could reflect onto end-product prices due to slowing demand. This is the primary reason why several blue-chip companies caught headlines with mass layoffs in the past few months.

As a result, we are handed a toxic combination of economic downturn, upward wage pressures, rising inputs costs, and harder conditions for both loan refinancing and credit generation. The YOY M2 expansion rate has gone into negative territory for the first time in the past 4-decades. this entails is that aggressive FED tightening will go on for a while despite higher recession risks. Even the most dovish expectations point to consecutive 25 basis points hikes in the next two meetings and May’s FOMC decision is up for grabs. Many argue the FED will purposefully “tip” the economy that still expands in high single digits in “nominal” dollars into the recession that is all but inevitable.

Hence macro-wise, everywhere you look at is screaming recession and some form of a hard landing. To add insult to injury, reduced long-term interest rates will not cushion the blow much this time since both fiscal excess (in 2023 the US Government is expected to supply $6 trillion USD worth of bonds & bills, while corporates will chip in for another trillion) and China’s reopening and potential risks from Ukraine conflict will set a floor for yields.

This pernicious backdrop has weirdly culminated in the most popular stock market and long-end retail ETFs (SPY and TLT respectively) to yield more than %7 to start the year (which ironically enables FED more wiggle room persist in its hawkish policy). As a trader, I find this somewhat understandable as the market is always eager to front a FED which is almost sure to step down to the fancied 25 basis hikes. As an analyst however, it befalls me to find out that the overly optimistic case for a bull market has funded so many “buyers”, which hinges on the assumption that FED will be done soon and starts scaling back before a hard recession arrives. Rather, the safer bet is to expect a quick and hard recession that will normalize both the FED policy, the yield curve, price levels, and of course the market prices for risk assets which desperately need a wake-up call to reality.

This article is sponsored content

Author

Emre Ozturk

Numberone Capital Markets Limited

Emre Ozturk is a dedicated, analytical and methodical finance professional who graduated in Business Administration from the Bogazici University.