What’s the best game in town

S&P 500 went up again after Friday‘s opening bell, yet the second day of rising bond prices led to rotations favoring defensives alongside my Monday picks of PLTR and TSLA. Financials continued doing great, industrials are among the easiest bullish choices together with energy readying an upswing. Retailers such as WMT speak as much for consumer strength as XLY and Friday‘s consumer confidence beat while inflation expectations didn‘t (yet) rise.

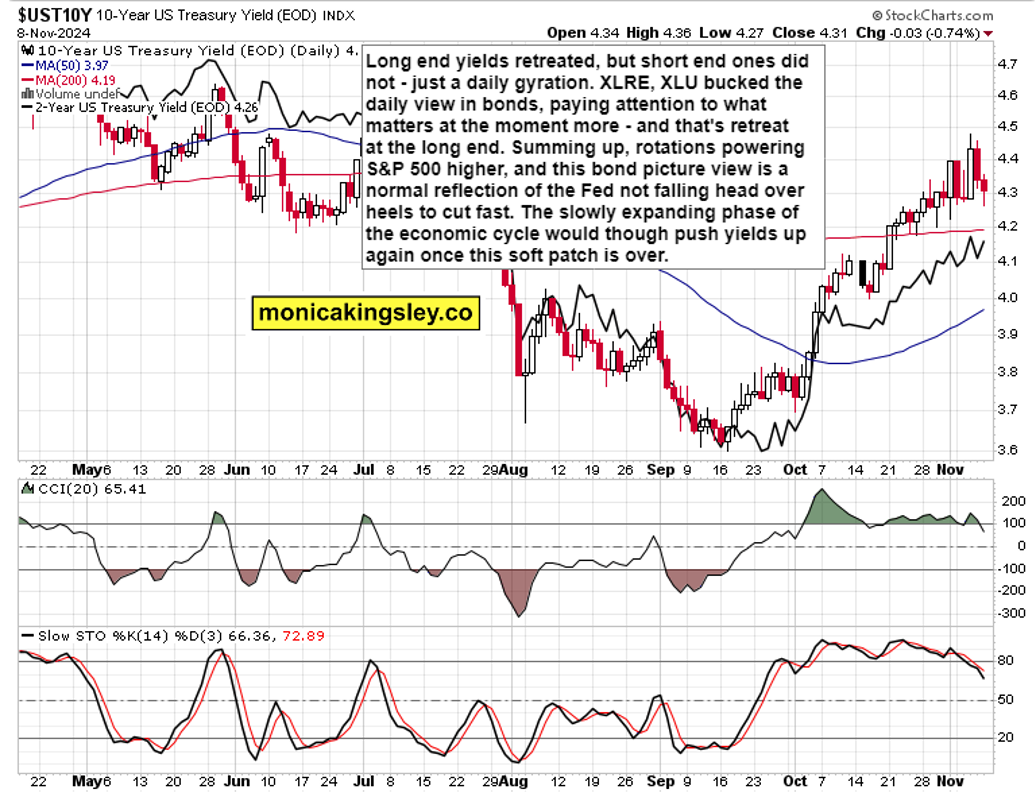

As a first, we got S&P 500 selling into the close, but this doesn‘t change the fact of equities still having higher to go even if tech is led by IGV and not SMH. That‘s all right – the most constructive intermarket move is the retreat in yields that I called for to happen when second half of the week started. After the 10y yield was rejected at 4.50%, we‘ll see whether a reprieve takes it to roughly 4.20% (that would be good for XLRE, ITB and XLU – don‘t expect universally bullish leadership miracles from these, there are easier sectoral plays), or the sum of positive economic surprises talked late in the week, takes yields to high 4.70s%.

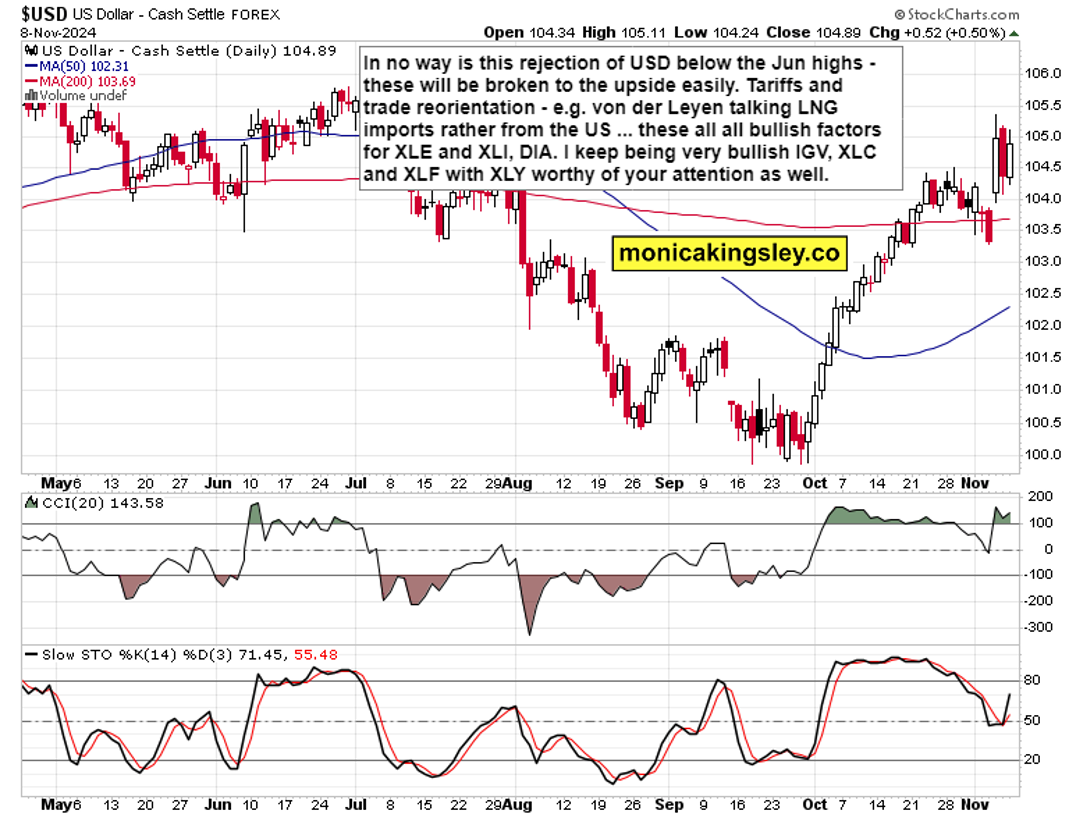

Both the dollar and rate cut odds (there is a distinct shift towards fewer cuts and these arriving later) hint at first no recession ahead, and second at the slowly rising productivity – both of which I have talked about for months. This will lead to the end of disinflation, and rising yields forcing a correction in the S&P 500, beyond the Jan-Feb seasonal weakness.

As regards the period till New Year‘s Eve, remember that right after elections (and the clear results arrived fast this time) the uncertainty-removed-driven (with sweep to multiply it) upswing comes fast, and then the pace of gains slows down, making for a very muted Santa Claus rally. Santa just doesn‘t deliver so generously during Presidential election years.

For now, there are no major cracks in the bullish dam, but I‘m watching various sectoral ratios and industrials as well for advance clues of when the lean times come again. Fine candidate for that to happen would be with the upcoming debt ceiling early 2025. What remains to be seen, is the confidence (volume of Treasuries buying stated plainly) of foreign central banks in 2025, whether that forces the Fed‘s hand or not. For now, the job market isn‘t source of inflationary pressures, and there is also plenty of money parked in money market funds to make for a slow grind higher in the main indices and select sectors – have a good look at the below yields and USD charts.

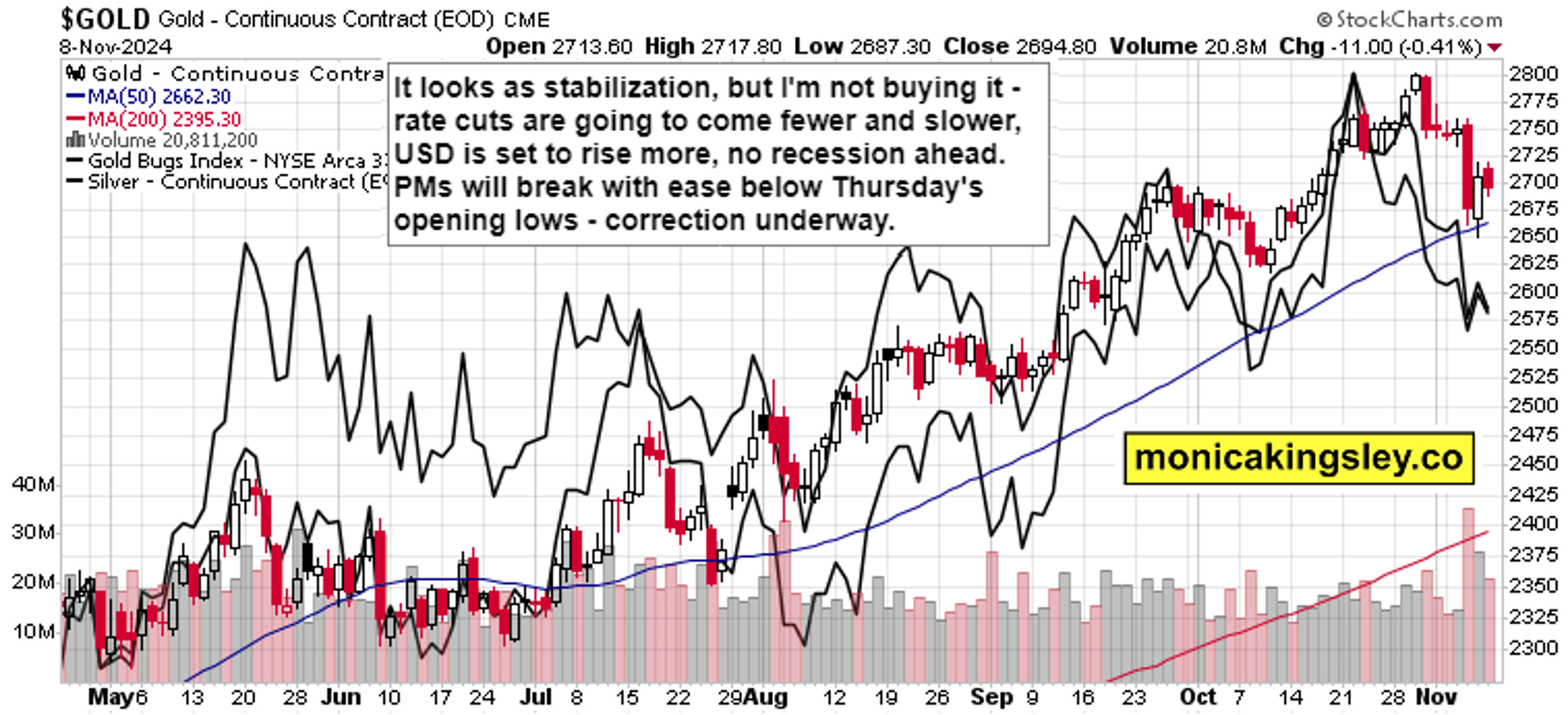

Gold, Silver and Miners

There are many great long-term reasons to be a precious metals bull, but I say the short-term path (lower) will offer more favorable entry points than the levels where prices are now, for gold, silver and miners alike.

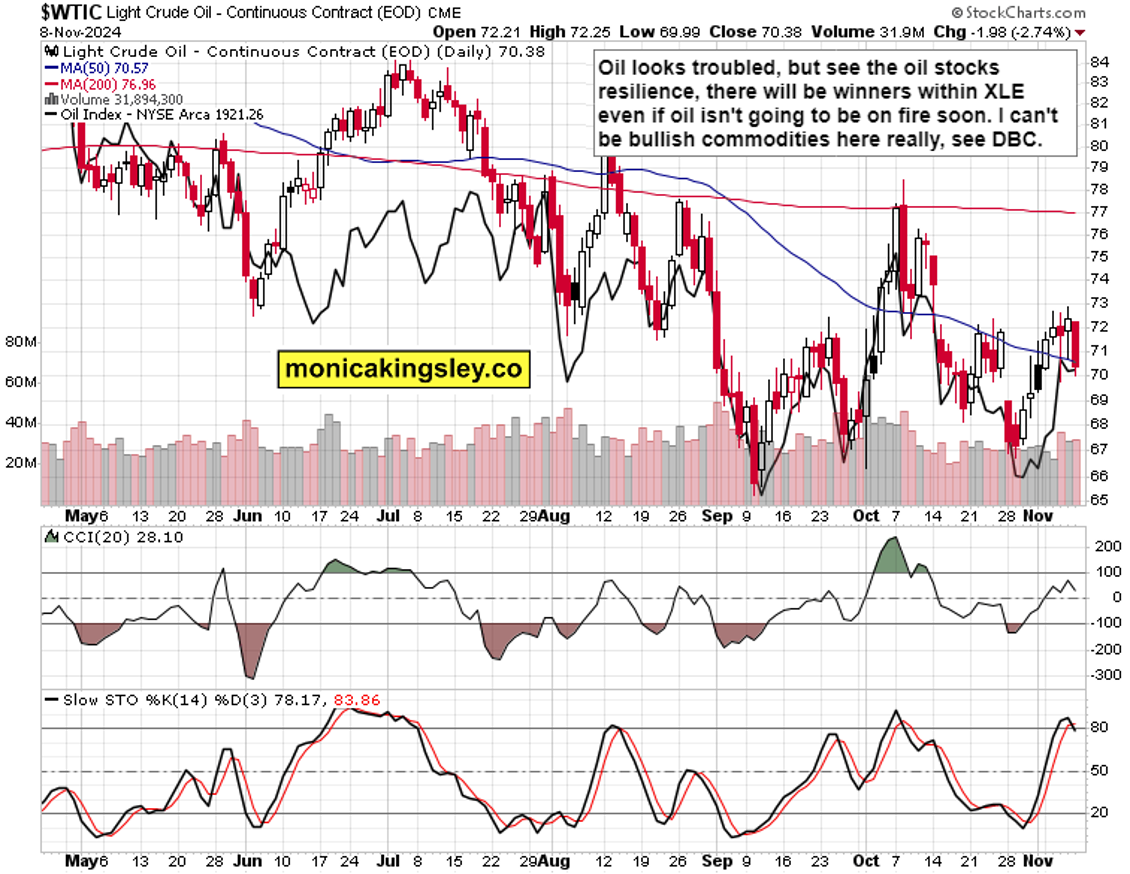

Crude Oil

Commodities are, and will be still, under pressure, relatively underperforming star picks such as crypto beyond Bitcoin. This is not yet time to be wildly bullish oil or copper – easier money is to be made elsewhere.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.