What to expect from May’s Federal Reserve meeting

A 50bp interest rate hike from the Federal Reserve is widely expected given recent commentary from officials and the fact inflation is well above target and unemployment is just 3.6%. The negative 1Q GDP print will be shrugged off with quantitative tightening also announced. We continue to see the risks skewed toward swifter, more aggressive action.

50bp from the Fed as inflation worries outweigh temporary GDP dip

The Federal Reserve is widely expected to raise its policy rate by 50 basis points next Wednesday as 8%+ inflation and a tight labour market trump the surprise 1Q GDP contraction attributed to temporary trade and inventory challenges. Moreover, consumer spending remained firm and the contribution from investment was solid and we expect this to continue into the second quarter. Wages are rising rapidly amid a dearth of workers and this will contribute to keeping inflation elevated through this year. Indeed, we don’t expect inflation readings to drop meaningfully below 4% before year end.

That said, the weakness in GDP makes it less likely that we will hear the Fed explicitly making the case for a more aggressive 75bp hike at the June or July FOMC meetings. This has been raised as a potential course of action by St Louis Fed President James Bullard. We are open to the possibility, but that would probably require a decent set of consumer spending numbers over the coming months and some very solid jobs gains that contribute to further wage pressures.

For now, our base case remains that the Fed will follow up next week’s 50bp hike with 50bp increases in June and July before switching to 25bp as quantitative tightening gets up to speed. We see the Fed funds rate peaking at 3% in early 2023.

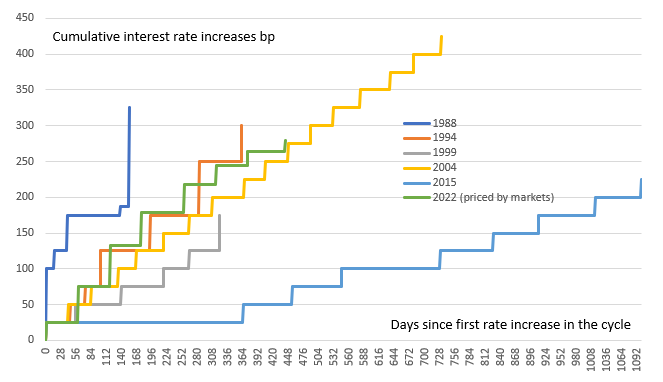

What's priced for Fed tightening and how it stacks up against previous cycles

Source: Macrobond, ING

Pulling the trigger on quantitative tightening

We will also be looking for the Fed to formally announce quantitative tightening on Wednesday. The minutes to the March FOMC meeting showed “all participants” felt the need to announce the “commencement of balance sheet runoff at a coming meeting”. Given the doubling of the size of the balance sheet since the last round of Quantitative Tightening in 2017-19, this would be done at a “faster pace” than back then. The minutes suggested “participants generally agreed that monthly caps of about $60 billion for Treasury securities and about $35 billion for agency MBS would likely be appropriate” versus the peak total $50bn run-off seen last time around.

This would be a “phased in” roll-off cap of maturing assets that could last 3+ months depending on market conditions. We expect it to start with $50bn being allowed to run off each month before getting up to $95bn by September.

Market circumstances the Fed will be cognizant of into the Q&A

Related to this, the Fed needs to be prepared for is a quizzing on repo market circumstances. Routinely some US$1.8tr continues to be shipped back to the Fed through its reverse repo window as the market has found it difficult to match the 30bp overnight rate offered by the Fed. In fact, Secured Overnight Financing Rate, which was at 30bp post the 25bp hike March hike, has slipped down to 28bp, in fact at one point touching 26bp. And beyond general collateral, many securities are on special. A lot of this has got to do with a shortage of collateral and an excess of liquidity, and part of this could be solved by a quicker balance sheet roll-off process. Any decision to move more quickly in that direction would be a nod of acknowledgement of these extreme circumstances.

Further out the curve, the Fed will be cognizant that US 10yr inflation expectations are threatening to break above 3% on a sustained basis, and will be keen to prevent this from happening, or at least to prevent any overshoot above 3% from being extreme or protracted. The Fed may not admit it, but a break above 3% would suggest they are losing the battle against rising inflation expectations. It's difficult to see how delivery of a heavily discounted 50bp hike will change this dynamic, so some additional verbal tightening may be required. From here, the 10yr inflation expectation movement will go hand in hand with the 10yr Treasury yield, with the real yield more stagnant, now that it is back at around zero (close to but below).

FX: As long as the Fed doesn't blink, the dollar stays bid

Trade weighted measures of the dollar are going into next week's Fed meeting on their cyclical highs. Driving this trend remains the conviction that the Fed has the most cause of any G10 central bank to rush monetary policy to normal. At the same time, the external environment of war in Europe and continued lockdowns in China are weighing on pro-cyclical currencies such as the Euro and the Renminbi. This is a particularly tough time for emerging markets, where US$50bn of portfolio capital has left bond and equity markets since late February.

Assuming that the Fed does not start to have second thoughts about the pace of its tightening cycle – and that seems unlikely – the re-iteration of an 'expeditious' normalisation of policy should keep the short end of the US yield curve supported and the dollar bid. A key driver of dollar strength since June last year has been the re-pricing of the Fed cycle and it still seems too early to make a call, with any confidence, that the top has been reached.

The prospects of tighter monetary policy in Europe might start to offer a little EUR/USD support. Yet our baseline scenario of a 1.05-1.10 range this summer is clearly at risk to an even more hawkish Fed and a further re-appraisal of European growth prospects. GBP/USD remains vulnerable should at some point the Bank of England disappoint the 150bp of rate hikes still priced in by year-end. As above, we see the next six to twelve months as particularly challenging for emerging market currencies, where the Brazilian Real and the South African Rand are probably the most vulnerable.

Read the original analysis: What to expect from May’s Federal Reserve meeting

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.