What did we learn about stocks this earnings season?

The earnings season is almost over and stock markets are in a joyful mood. Even though corporate earnings are on track to decline for a second quarter, the drop was far less severe than what analysts expected, spreading cheer in the markets. In this piece, we dissect the outlook for earnings and examine whether valuations reflect economic reality.

Beating a low bar

As the earnings season winds down, the results have been quite encouraging. In the first quarter of this year, analysts had projected a decline of more than 5% in S&P 500 earnings compared to the same period last year. Yet, with the grand majority of companies having reported, the actual fall was closer to 0.7% so far.

That still means corporate earnings are shrinking, but the contraction was not as severe as feared. Investors often care most about any surprises relative to expectations, not the direction of travel itself, so this relative outperformance came as pleasant news for markets.

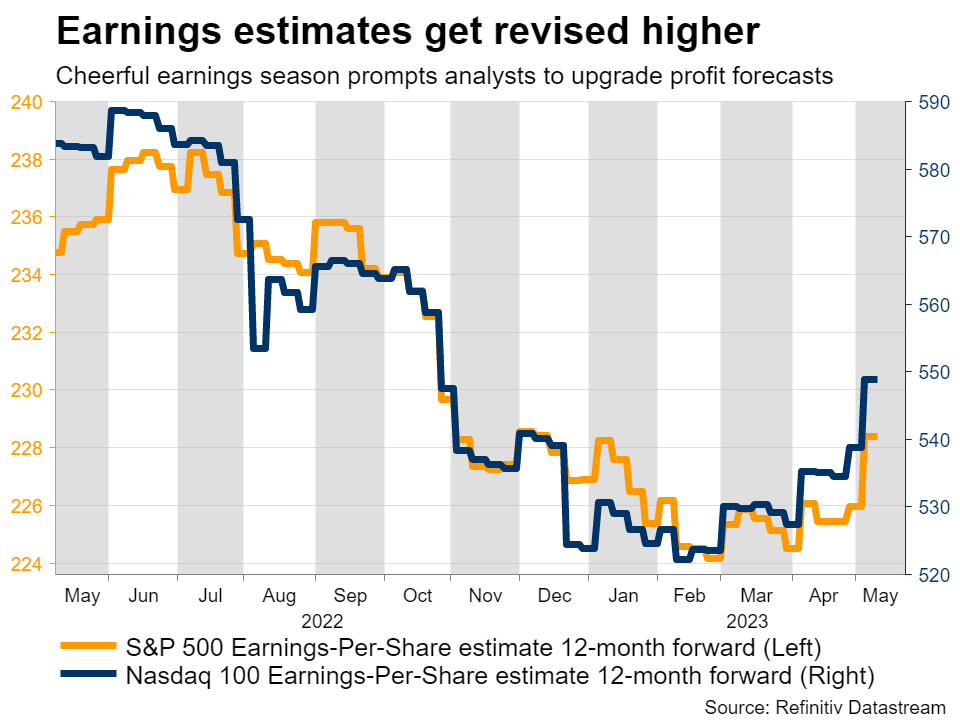

In a nutshell, analysts set the bar so low heading into the earnings season that businesses managed to jump over it without any issues. Of the 84% of S&P 500 companies that have already reported, around 77% of them have beaten expectations, which is much higher than usual.

Behind the scenes

Even though the decline was shallower than what analysts expected, this is now the second straight quarter of falling profits, marking the start of an earnings recession. Making matters worse is the fact that earnings are nominal numbers, meaning they are not adjusted for inflation.

If one accounts for an inflation rate running close to 5%, the real decline in earnings was even worse than mentioned above. And according to analysts, a third consecutive earnings drop is anticipated when the results for the current quarter are released.

Nonetheless, the S&P 500 has risen almost 18% from its lows reached back in October, shrugging off this shrinkage in profitability. One potential explanation for this rally is that investors are looking ahead towards the second half of the year and beyond, where earnings growth is expected to return to positive territory.

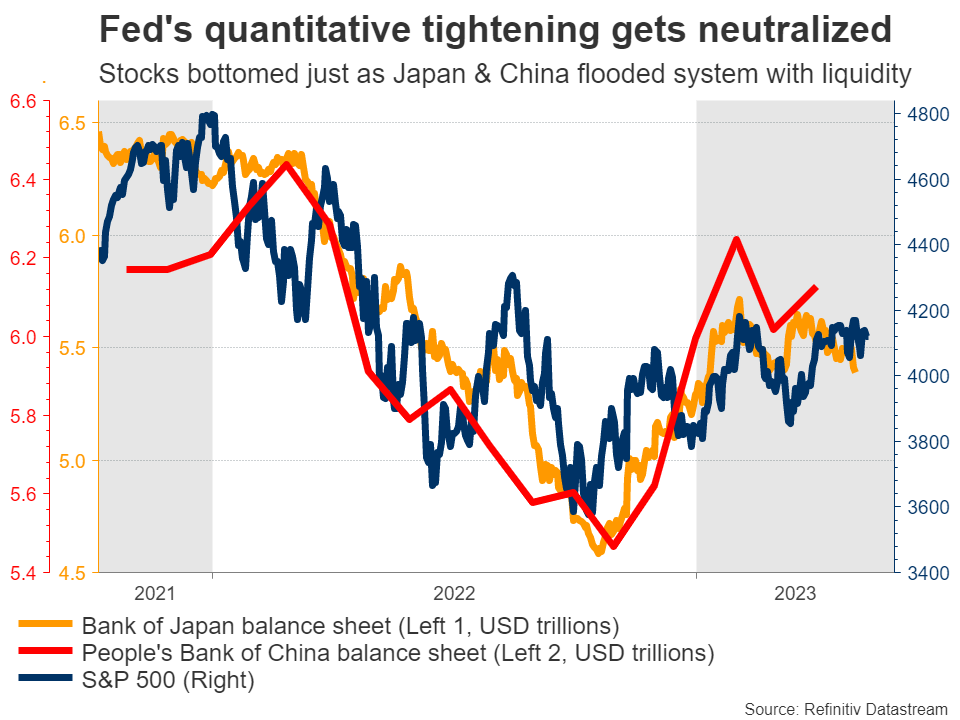

Another explanation lies with liquidity injections. Liquidity refers to how much money is sloshing around in the financial system, available to buy assets. Even though central banks in the United States and lately in Europe have been draining liquidity out of the system through their quantitative tightening programs, their efforts have been more than offset by enormous liquidity injections in Japan and China.

Liquidity is a global phenomenon, so when the Bank of Japan and the People’s Bank of China put money into their systems, it still finds its way into US markets. And they have been doing that, in tremendous force. Since October, the BoJ and the PBoC have collectively expanded their balance sheets by roughly $1.6 trillion, whereas the Fed has merely drained $200 billion.

It is probably not a coincidence that the S&P 500 bottomed in October, exactly when these liquidity injections started.

Valuations are pretty scary

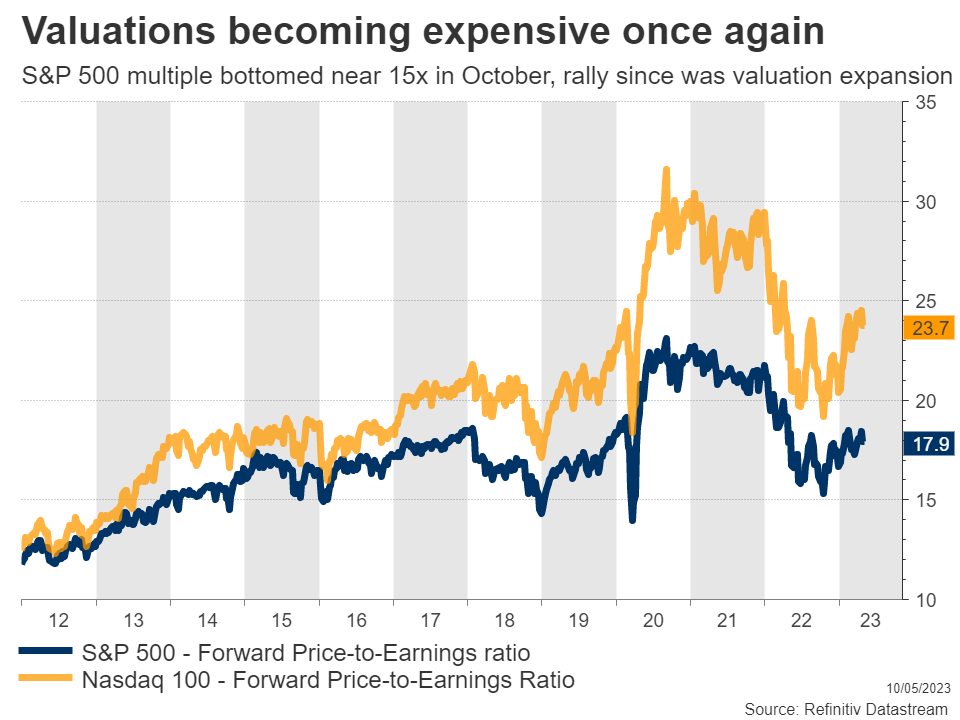

When you have a liquidity-driven rally in stock markets that is not backed up by an increase in earnings, the result is that valuations become more expensive. Indeed, the entire recovery since the October lows reflects an expansion in valuation multiples.

The S&P 500 currently trades for nearly 18 times what analysts expect earnings to be over the next 12 months, which is rather expensive. Such a valuation assumes everything will turn out perfectly - interest rates will fall as inflation cools, but economic growth will remain resilient. In other words, the stock market is pricing in a ‘soft landing’ for the economy.

Nobody truly knows how the economy will play out. The post-pandemic era has been one of the strangest economic cycles ever, leaving even seasoned economists scratching their heads. A soft landing is certainly possible, although history would suggest it is not very probable considering how rapidly interest rates have risen.

From an investment perspective, the fact that markets are almost priced for perfection leaves little room for error. Analysts predict earnings growth will reaccelerate from the third quarter onwards, but that’s precisely when the lagged impact of all the previous rate increases might hit the economy. Hence, it’s difficult to trust this forecast, despite the rosy guidance from corporate executives.

The bottom line is that the risk/reward profile for equity markets does not seem attractive at this stage. A tsunami of liquidity and speculation around Fed rate cuts have carried stocks higher, albeit in an environment of stagnant earnings and high valuations. This might be a classic case of excessive optimism that corrects over the remainder of the year, especially if the data pulse begins to weaken.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service